What if your business’s ability to scale had nothing to do with your personal bank account and everything to do with the office supplies you bought last month? Most entrepreneurs feel the weight of personal guarantees or the frustration of a “thin” credit file that keeps them from the best financing terms. You can master how to maintain a good business credit history by shifting your focus to strategic vendor tradelines and disciplined reporting habits. It’s about building a foundation that works for you, not against you.

We understand that the world of business credit can feel like a maze, especially when you aren’t sure which bureaus matter or how to avoid putting your personal assets at risk. This guide provides a clear roadmap to help you navigate reporting cycles and access better interest rates. We’ll cover the step-by-step process of using NET 30 accounts to keep your profile active and healthy. Please note that this content is for educational purposes and is not financial or legal advice. We don’t provide guarantees regarding specific credit score increases.

Key Takeaways

- Establish a strong foundation by opening Net 30 accounts with vendors that report directly to major bureaus like Equifax Business, Creditsafe, and FairFigure.

- Learn how to maintain a good business credit history by following a consistent cycle of purchasing essential office supplies and paying invoices before the due date.

- Ensure your business information, including your legal name and address, remains consistent across all registrations to avoid fragmented or inaccurate credit files.

- Leverage practical business purchases, such as onboarding kits and custom uniforms, to build tradelines while simultaneously supporting your daily operations.

- Protect your credit health by strictly separating personal and business finances to prevent the common mistake of commingling funds.

Understanding the Foundations: What is Business Credit History?

Building a robust credit profile is the gateway to unlocking corporate funding without risking your personal assets. When you master how to maintain a good business credit history, you transition from a “thin file” to a creditworthy entity that lenders and suppliers respect. This guide provides the exact steps to manage your financial reputation through strategic purchasing and disciplined reporting habits.

The CEO Creative acts as a foundational partner in this process. As a reporting Net 30 vendor, we offer high-quality products that help startups and established LLCs establish their credit footprint. By reporting your payment activity to major bureaus, we help turn your routine operational costs into a verifiable record of financial reliability.

Trust Note: This content is for educational purposes and doesn’t constitute financial or legal advice. We make no guarantees regarding specific credit score increases.

To better understand how this process changes your business trajectory, watch this helpful video:

The Role of Net 30 Vendors

Net 30 accounts are widely considered the “Tier 1” of business credit building. These accounts provide credit terms that allow you to pay for your purchases within 30 days of the invoice date. When a vendor reports this activity, it creates what’s known as a vendor tradeline on your business credit reports. Unlike many traditional loans, a business Net 30 account often allows for EIN-only approval. This structure helps you build a credit history for your business without requiring a personal guarantee, keeping your personal and professional finances completely separate.

Why Maintenance Matters for New LLCs

For a new LLC, consistency is your greatest asset. Learning how to maintain a good business credit history requires a commitment to small, repetitive actions that prove your reliability. This history isn’t just about a number; it impacts your insurance premiums and gives you leverage during supplier negotiations. Successful reporting depends heavily on business info consistency. Your legal name, address, and phone number must match exactly across all accounts to avoid fragmented files. By purchasing essential office supplies and paying invoices early, you demonstrate the stability needed to move from “no file” to “creditworthy.”

The Mechanics of Business Credit Reporting

Understanding the backend of credit reporting is essential if you want to know how to maintain a good business credit history. Unlike personal credit, where almost every bank reports to the same three bureaus, business reporting is more fragmented. Data flows from a reporting vendor to the bureaus based on a specific schedule, often every 30 to 45 days. This delay means your actions today might not reflect on your profile for several weeks. Consistency is the only way to ensure your file stays current.

The process starts when you place an order. Once the invoice is generated and paid, that payment data is batched and sent to agencies. This cycle makes Net 30 terms a powerful strategy for any growing brand. You get to keep your cash in the business for an extra month while simultaneously building a record of reliability. If you’re ready to start this cycle, you can apply for a business Net 30 account to begin your reporting journey.

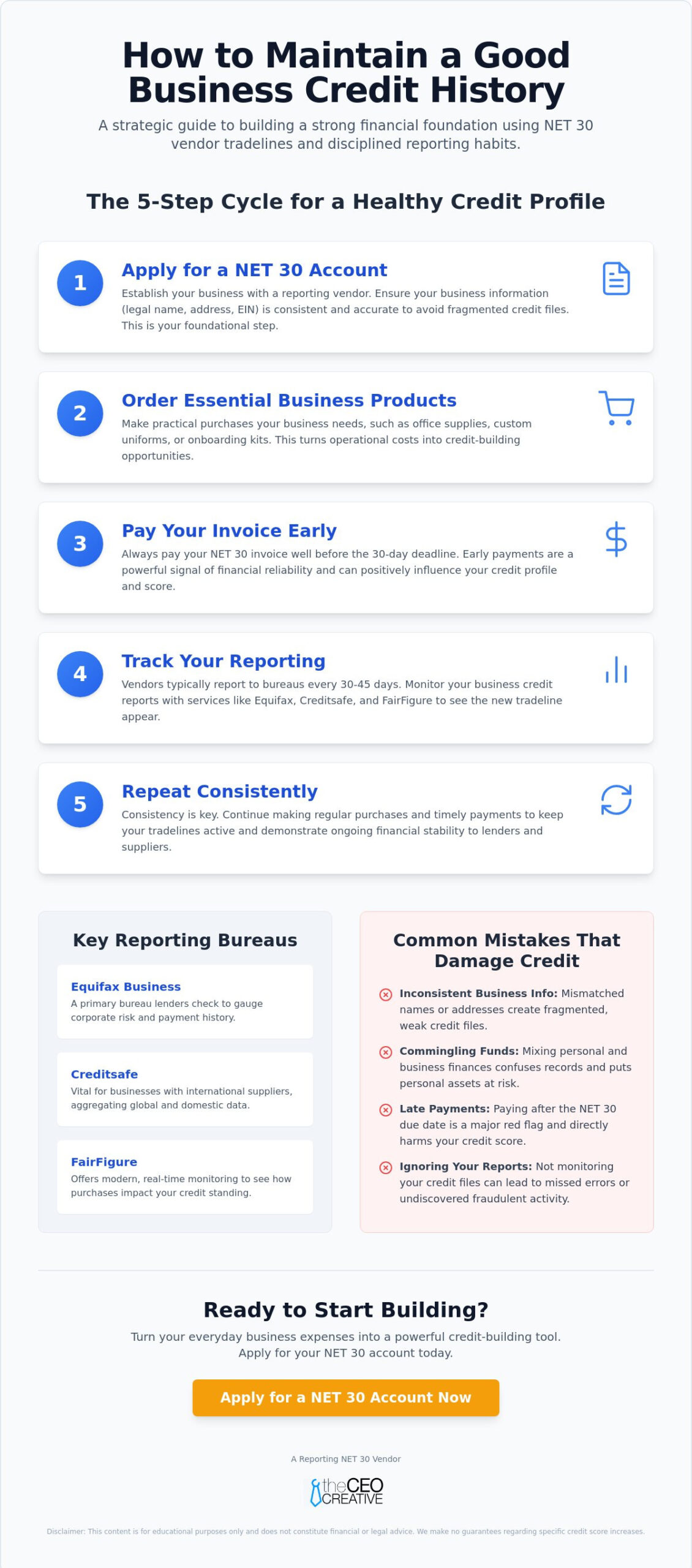

The Bureau Ecosystem: Equifax, Creditsafe, and FairFigure

Equifax Business remains a heavyweight in the industry. Lenders often look here first to gauge your corporate risk level. Creditsafe is equally vital, especially if you deal with international suppliers, as they aggregate domestic and global data to provide a comprehensive rating. For modern entrepreneurs, FairFigure offers a way to monitor these scores in real-time, helping you see exactly how your purchases impact your standing. For more on the basics of this system, consult the SBA guide to establishing business credit.

Tradeline Visibility and Impact

You typically need between 3 to 5 reporting tradelines before a bureau will even generate a score for your business. This is why choosing the right partners is critical. Many big-box retailers are non-reporting vendors. They’ll sell you products, but they won’t help you build your file. Working with a reporting vendor ensures that every dollar spent on operations also acts as an investment in your credit score.

Consistency beats intensity every time. It’s better to make small, monthly purchases than one massive order every year. Frequent activity ensures your data remains fresh and your profile stays active. This steady stream of “paid as agreed” marks is the most effective way to show underwriters that your company is a safe bet for larger financing down the road. It keeps your file from becoming stagnant or “thin” in the eyes of automated scoring models.

The 5-Step Checklist for Maintaining Good Credit

Success in business credit isn’t about one large transaction. It’s about a series of small, disciplined actions. If you want to master how to maintain a good business credit history, you need a repeatable system. This checklist provides a clear roadmap to move from a basic EIN registration to a robust, fundable credit profile.

- Apply: Start by opening a business net 30 account with a vendor known for reporting to major bureaus. This establishes your first foundational tradeline.

- Order: Purchase essential office supplies or branded materials. Use these items for daily operations to keep your spending professional and practical.

- Pay: Settle your invoices early. While Net 30 gives you a month, paying sooner signals high liquidity and management discipline to underwriters.

- Track: Monitor your reports regularly. Resources like Experian’s guide to business credit help you understand the specific data points lenders evaluate.

- Repeat: Continue this cycle every 90 days. A stagnant profile can lead to score drops or “inactive” status at some bureaus, so keep the data flowing.

Optimizing the Payment Cycle

The “Early Payment” advantage is a secret weapon for savvy entrepreneurs. Many scoring models reward you more for paying 15 days early than for simply paying on the due date. Set up digital reminders or automated alerts to ensure you never miss a window. Diversifying your tradelines also helps. You can look into the best Net 30 apparel vendors to build business credit in 2026 to add variety to your profile while outfitting your team with professional gear.

Monitoring for Consistency

Data integrity is the backbone of credit maintenance. When learning how to maintain a good business credit history, you must verify that your business name, address, and phone number match exactly on every invoice and registration. A missing “LLC” or a mistyped suite number can cause reporting errors that are difficult to fix later. If you spot an inaccuracy, dispute it immediately with the bureau. Using membership tools can streamline this tracking, providing a central dashboard to view your progress and catch errors before they impact your funding chances. It’s about being proactive rather than reactive with your company’s financial reputation.

Common Mistakes That Damage Business Credit

Maintaining your professional reputation is a full-time commitment. Many founders stumble because they treat their business finances like a personal hobby. If you want to master how to maintain a good business credit history, you must avoid the pitfalls that lead to automatic denials and stagnant scores. Even a single reporting error or a missed window can set your progress back by months.

Avoid these common mistakes to keep your profile healthy:

- Commingling funds: Using personal bank accounts for business purchases makes it impossible to build a distinct corporate identity.

- Non-reporting vendors: Spending thousands with suppliers that don’t share data with bureaus is a wasted opportunity for growth.

- Inconsistent NAP data: Discrepancies in your Name, Address, or Phone number across different accounts can lead to fragmented credit files.

- Reactive building: Waiting until you actually need a loan to start establishing credit is a recipe for rejection.

- Poor bookkeeping: Missing a payment window because of disorganized records is the fastest way to tank a Tier 1 score.

- Skipping tiers: Applying for high-level corporate cards before you have established baseline tradelines often results in hard inquiries with no approvals.

The Trap of the Personal Guarantee

Relying on personal credit cards for business expenses is a common trap that hinders corporate growth. It keeps the financial liability on you and prevents your business from standing on its own. The goal is to transition toward EIN-only accounts that don’t require your Social Security number. You also need to watch out for “credit ghosting.” This happens when a business has no reported activity for six months or more. Bureaus may stop generating a score entirely if your file goes dormant, so keep your tradelines active with regular, small purchases. You can take the first step toward true corporate independence when you apply for a business Net 30 account.

Operational Errors to Avoid

Small administrative oversights often have large financial consequences. If you move offices, you must update your business address with the Secretary of State immediately. If your credit file address doesn’t match your legal registration, reporting will fail. You should also monitor your file for identity theft, as business profiles are frequent targets for fraudulent accounts. Finally, don’t overextend your credit limits too quickly. Rapidly hitting your maximum limit on new accounts can signal financial distress to underwriters, even if you pay on time. Slow, steady utilization is the most effective way to show you know how to maintain a good business credit history over the long term.

Strategic Scaling: Using Products to Build Credit

Instead of viewing overhead as a drain on resources, use it as a tool for growth. Purchasing customizable products like onboarding kits or promotional items creates a verifiable record of financial reliability. Similarly, investing in Net 30 apparel ensures your staff looks professional while you establish the tradelines necessary for future funding. By choosing products that serve a practical business purpose, you keep your spending disciplined and your credit file active.

Branding for Credibility

Professional branding does more than attract customers; it increases your perceived creditworthiness in the eyes of lenders and underwriters. A cohesive brand identity, including high-quality logos and custom stationery, signals that your company is established and stable. This visual consistency mirrors the data consistency required for successful credit reporting. You can even explore Logo Design for Business Credit to build your brand and your tradelines at the same time. Maintaining a professional image across all touchpoints ensures that when a lender reviews your file, they see a serious, fundable organization.

The CEO Creative Membership Advantage

The CEO Creative Membership is designed for the modern entrepreneur who values efficiency and growth. It provides access to exclusive tools that simplify the logistics of management and credit building. This structured approach helps you automate the “Repeat” step of the credit maintenance checklist, ensuring you never go through a period of “credit ghosting.” By integrating your procurement needs with a reporting vendor, you create a seamless cycle of activity that bureaus reward.

Take Control of Your Corporate Financial Future

Maintaining a healthy credit profile isn’t a one-time event; it’s a disciplined cycle of procurement and reporting. By prioritizing reporting vendors and ensuring your business data remains consistent across every account, you protect your company from the common pitfalls that stall growth. Mastering how to maintain a good business credit history allows you to secure better financing terms and build a brand that stands on its own EIN without personal liability.

You don’t have to navigate this logistical maze alone. Start your journey with a partner that reports your payment activity to major bureaus like Equifax, Creditsafe, and FairFigure. With instant approval for qualified businesses and no personal guarantee required for EIN accounts, building your professional foundation has never been more accessible or efficient.

Apply for a CEO Creative Net 30 Account and Start Building Credit Today

What happens next: Submit your application using your EIN for instant approval consideration. Browse our catalog of office supplies and customizable products to place your first order. Pay your invoice early to trigger your first positive report to major bureaus.

Maintaining business credit is about consistency, professional branding, and reporting accuracy. Start by outfitting your team with professional apparel or ordering essential supplies to keep your tradelines active. Your sustainable success starts with the disciplined systems you put in place today.

Frequently Asked Questions

Do Net 30 vendors require a personal guarantee?

Many Tier 1 vendors don’t require a personal guarantee for account approval. This is a primary benefit for founders learning how to maintain a good business credit history without risking their personal assets. By using your EIN for the application, the financial liability stays with the business entity. This separation is crucial for protecting your personal credit score while building a fundable corporate reputation.

How long does it take for a Net 30 account to report to the bureaus?

Reporting timelines typically range from 30 to 60 days depending on the vendor’s specific schedule. Most reporting vendors batch their data and send it to bureaus once a month. If you pay an invoice right after a reporting cycle, it might take an extra month to see that activity on your report. Consistency in your purchasing habits ensures your profile stays updated as these data cycles refresh.

Will paying my invoice early help my business credit score?

Paying early is one of the most effective ways to boost your business credit score. Many business credit models reward you more for paying 15 days before the due date than for paying on the day it’s due. This signals to underwriters that your company has excellent cash flow and management habits. It’s a proactive move that builds trust quickly with future lenders and suppliers.

Which credit bureaus does The CEO Creative report to?

The CEO Creative currently reports payment activity to Equifax Business, Creditsafe, and FairFigure. Reporting to multiple agencies is vital because different lenders use different bureaus to assess risk. This broad visibility ensures that your positive payment history is recognized across the industry. It helps you build a more comprehensive and reliable financial profile for your brand without relying on a single data source.

Can I build business credit without an LLC or Corporation?

You should register as an LLC or Corporation to build business credit effectively. While sole proprietors can sometimes open accounts, those accounts are often tied directly to a personal Social Security number. Forming a legal entity provides the EIN necessary to create a separate credit file. This distinction allows your business to stand on its own financial merits and protects your personal assets from business liabilities.

What happens if I miss a payment on a Net 30 account?

A missed payment can cause your business credit score to drop significantly and stays on your report for years. Late payments are reported to the bureaus and signal high risk to other suppliers and financial institutions. If you realize you can’t meet a deadline, contact the vendor immediately to discuss your options. Being proactive may help you avoid a negative report and preserve the professional relationships you’ve worked hard to build.

How many tradelines do I need to get a business credit score?

Most bureaus require at least three reporting tradelines before they generate a score for your EIN. Some lenders look for five or more active accounts to verify your company’s long-term stability. Learning how to maintain a good business credit history involves keeping these accounts active with regular, small purchases. This steady stream of data prevents your file from becoming stagnant or being labeled as a “thin” file.

Does my personal credit score affect my business credit history?

Your personal credit score shouldn’t affect your business history if you strictly use EIN-only accounts. However, many traditional banks still check personal credit if your business file is new or has very few reporting tradelines. As you build a robust corporate history, you reduce the need for lenders to look at your personal finances. Eventually, your business will qualify for high-tier funding based solely on its own credit merits.