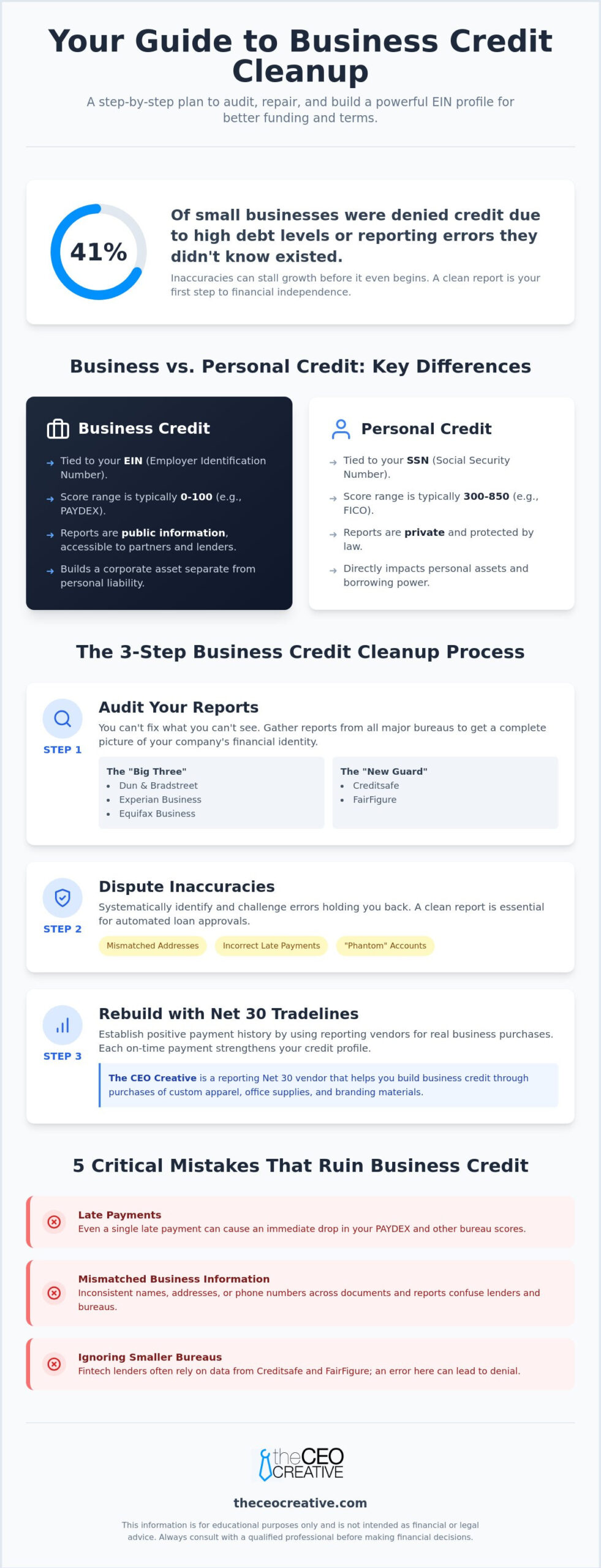

Did you know that 41% of small businesses denied credit in early 2026 were turned away because of high debt levels or reporting errors they didn’t even know existed? It’s a sobering reality that proves your hard work isn’t always reflected in your official files. If you’ve struggled with high interest rates or confusion between your personal and business scores, cleaning up your business credit report is the first step toward true financial independence.

We understand how discouraging it feels to have your growth stalled by a number on a screen. This guide promises to demystify the process by showing you how to identify inaccuracies, file effective disputes, and leverage Net 30 tradelines to build a stronger foundation. We’ll explore the mechanics of bureau reporting and provide a step by step plan to ensure your EIN stands on its own. You’ll learn how to replace outdated data with a professional profile that unlocks higher limits and better supplier terms.

Key Takeaways

- Audit your files across major bureaus like Equifax, Creditsafe, and FairFigure to catch the hidden errors that lead to loan denials.

- Follow a structured checklist for cleaning up your business credit report to systematically remove inaccuracies and strengthen your corporate identity.

- Avoid critical mistakes like mismatched business names or late payments that can cause immediate drops in your PAYDEX and bureau scores.

- Leverage reporting Net 30 accounts to build a positive payment history through real purchases of branding materials and office supplies.

- Transform your credit profile into a professional asset that secures higher limits and better terms using just your business EIN.

The Fundamentals: Understanding Business Credit Cleanup in 2026

Accuracy is everything. A single error on your business credit report can cost you thousands in interest or trigger an immediate loan denial. Cleaning up your business credit report isn’t just about fixing the past; it’s about positioning your company for future growth. This guide outlines how to purge inaccuracies and strengthen your EIN profile with precision. Most entrepreneurs don’t realize that a mismatched address or an incorrectly reported late payment can haunt their files for years, stalling expansion before it begins.

To succeed, you must understand two core concepts: the vendor tradeline and payment reporting. A vendor tradeline is a credit account between your business and a supplier, such as The CEO Creative, that reports your payment history to credit bureaus. Payment reporting is the actual mechanism where these vendors send your transaction data to bureaus like Equifax and Creditsafe. When you partner with a reporting Net 30 vendor, every on-time payment helps build a track record of fiscal responsibility that lenders can verify instantly.

To better understand this concept, watch this helpful video:

Why Business Credit Reports Differ from Personal Credit

Unlike your personal financial history, business credit reports are public information. Anyone can view your company’s creditworthiness for a small fee, from potential partners to competitors. While personal FICO scores range from 300 to 850, business scores typically operate on a 0 to 100 scale. This logic prioritizes payment speed and trade depth over simple credit utilization. Crucially, these reports are tied to your Employer Identification Number (EIN) rather than your Social Security Number (SSN). This allows you to separate your personal life from your professional liabilities and build an asset that exists independently of your personal credit score.

The Impact of a Clean Report on EIN-Only Funding

A clean report is the key to unlocking “no personal guarantee” (No-PG) financing. Lenders feel confident extending credit to your EIN alone when your file shows zero delinquencies and strong trade lines. This clarity is essential for moving into Tier 2 and Tier 3 credit lines, where limits are higher and terms are more favorable. By removing negative marks, you essentially clear the path for larger equipment leases and higher-limit business credit cards that don’t require you to put your personal assets at risk. Scaling businesses also benefit from reducing overhead through efficient merchant services like LyrxPay, which provides lower-fee payment processing to keep more capital in your company. Please remember that this content is for educational purposes and is not financial or legal advice.

Step 1: Auditing Your Reports Across All Major Bureaus

You cannot fix what you cannot see. Most entrepreneurs only look at one report, but lenders in 2026 pull data from multiple sources to assess risk. The first phase of cleaning up your business credit report involves gathering files from the “Big Three”: Dun & Bradstreet, Experian Business, and Equifax Business. However, a complete audit now requires looking at the “New Guard.” Monitoring Creditsafe and FairFigure is mandatory because alternative lenders and fintech companies increasingly rely on these bureaus to make instant funding decisions. If an error exists on a smaller bureau report, it can still trigger an automated denial even if your D&B score is perfect.

Accessing your data is straightforward. D&B, Experian, and Equifax all provide portals where you can request your files. It is vital to monitor your business credit regularly to catch “phantom” accounts. These are debts or credit lines that don’t belong to your LLC but were attached to your EIN due to clerical errors. If you are just starting this process, ensure you know how to get a D-U-N-S number quickly, as this unique identifier is the backbone of your Dun & Bradstreet profile. For those who want a more integrated approach, The CEO Creative Membership offers specialized tools for credit building and tracking that simplify the oversight of your corporate identity.

Common Red Flags to Look For

During your audit, search for mismatched business information. Inconsistent spellings of your business name, varied suite numbers, or old phone numbers can create duplicate profiles. These duplicates split your credit history, making your business appear younger or less stable than it actually is. You should also look for outdated UCC filings. These are legal notices of a lender’s interest in your assets; if a loan is paid off but the filing remains, it looks like you have more debt than you do.

Finally, verify your industry classification. Incorrect SIC or NAICS codes often categorize a business as “high risk” without cause. If you are a consultant but your code suggests you are in high-risk real estate, you may face higher interest rates or lower credit limits. Once you have identified these gaps, you can begin the work of repairing them. A proactive way to start fresh is to apply for a net 30 account that reports positive data to the bureaus, helping to outweigh any past inaccuracies with new, reliable payment history.

Step 2: The Step-by-Step Business Credit Cleanup Checklist

Turning a thin or damaged file into a robust corporate profile requires more than just removing negatives. You must overwhelm old, stagnant data with a fresh stream of positive activity. Cleaning up your business credit report is a recurring cycle, not a one-time event. As you refine your file, maintaining a professional brand identity is critical. Lenders often look at your digital and physical presence to verify your legitimacy. Using strategic purchases to build your brand while simultaneously building credit is a move that separates visionary CEOs from basic operators.

For a comprehensive list of partners who report to major bureaus, consult our Net 30 Vendors 2026 Guide. This resource helps you select vendors that align with your specific industry needs. By choosing the right partners, you ensure that every transaction works in your favor.

The 5-Step Execution Plan

Follow this structured roadmap to ensure every dollar you spend contributes to your credit health. This “Apply, Order, Pay” framework is the most efficient way to build a file from scratch. It creates a predictable pattern that credit algorithms reward with higher scores.

- 1. Apply: Open accounts with reporting vendors like The CEO Creative. These accounts typically offer instant approval with an EIN, making them perfect for new LLCs or those rebuilding.

- 2. Order: Purchase essential business products. Invest in items that grow your brand, such as custom apparel or office supplies.

- 3. Pay: Settle your invoices early. In the world of business credit, paying 10 days before the due date often results in a higher score than paying on the day it’s due.

- 4. Track: Monitor your reports to ensure the tradeline appears on Equifax, Creditsafe, or FairFigure. This verification step confirms your efforts are being recorded accurately.

- 5. Repeat: Consistency is the secret. Maintain a monthly “buy and pay” cycle to show lenders you can handle ongoing credit obligations over the long term.

Disputing Inaccuracies Effectively

While you build new history, you must also address the errors discovered during your audit. You’ll need to file a formal dispute with each bureau separately because they don’t share data with one another. When disputing errors on your credit report, your evidence must be undeniable. Gather your invoices, canceled checks, and Secretary of State filings to prove your case. Once you submit your claim, expect a 30 to 45 day window for the investigation phase. Stay organized and follow up if you don’t see a resolution within that timeframe. A clean file is worth the patience and the administrative effort.

8 Common Mistakes That Ruin Business Credit Reports

Identifying errors is only the beginning. To maintain a clean profile, you must recognize the behaviors that trigger automatic red flags in bureau algorithms. Cleaning up your business credit report requires a proactive stance against these common pitfalls. Many entrepreneurs unknowingly sabotage their growth by overlooking technical details that lenders use to verify legitimacy. Avoid these errors to ensure your efforts in credit building aren’t wasted on a flawed foundation.

- Late Payments: Business credit is unforgiving. Even a payment made one day past the deadline can cause a significant drop in your PAYDEX score, which relies heavily on payment promptness.

- Mismatched Information: Inconsistency is a major red flag. If you use “LLC” on one application but leave it off another, bureaus may create separate, weaker files for your business.

- Neglecting “Thin” Files: Having only one tradeline is nearly as risky as having none. Lenders want to see a diverse range of credit experiences before approving high-limit loans.

- Personal Guarantee Reliance: Relying on your SSN keeps your business tied to your personal life. You must move credit to the EIN level to protect your personal assets and build corporate autonomy.

- High Credit Utilization: Maxing out vendor lines suggests cash flow struggles. Use your limits strategically rather than exhausting them every month to show you don’t live on credit.

- Ignoring Small Bureaus: Lenders often check Creditsafe and FairFigure even if you only monitor Dun & Bradstreet. An error on a minor report can still cause an automated denial.

- Closing Old Accounts: The age of your credit history matters. Closing your oldest vendor accounts shortens your track record and can lower your overall score.

- Failing to Monitor: Discovering identity theft or clerical errors only when you apply for a loan is a recipe for disaster. Regular oversight is mandatory for long-term success.

The Data Mismatch Trap

Your business address must match exactly across every utility bill, credit application, and government filing. Even slight variations, like “Suite 100” versus “#100,” can confuse automated systems and lead to duplicate profiles. While it feels like a relic of the past, 411 directory listings still influence some older scoring models used by traditional banks. To appear established, always use a professional business email and a dedicated phone line rather than a personal cell number or a generic Gmail address.

The Danger of Co-mingling Funds

Paying business debts with personal credit cards muddies your report and weakens the “corporate veil.” Lenders need to see a dedicated business checking account for tradeline verification. This separation proves your company is a distinct financial entity capable of managing its own obligations. If you are ready to build a professional, EIN-only history, apply for a net 30 account today to start reporting positive data correctly.

Rebuilding Your Profile with The CEO Creative Net 30 Tradelines

Cleaning up your business credit report is only half the battle. Once the inaccuracies are gone, your file might look thin or empty. This is where The CEO Creative acts as your strategic partner. We are a reporting Net 30 vendor that helps build business credit through real business purchases. By ordering items you already need, such as custom apparel or engraved merchandise, you create a paper trail of reliability that bureaus can’t ignore. Shop Net 30 Office Supplies to start your first tradeline and demonstrate your company’s ability to handle credit responsibly.

We report your payment history to Equifax, Creditsafe, and FairFigure simultaneously. This multi-bureau reporting ensures that your hard work is visible to a wide range of lenders and suppliers. While you focus on growing your brand, our reporting system works in the background to strengthen your EIN profile. This approach turns routine operational spending into a strategic move for your company’s financial future.

What Happens After You Apply?

The transition from a damaged report to a professional profile is a structured process. Once you are approved, you gain immediate access to the member portal and our full suite of custom branding tools. Your first order triggers the reporting cycle. As soon as you settle your invoice, we prepare the data for the next reporting period. Most members begin to see these positive tradelines appear on their business reports within a 30 to 90 day window. This timeline allows the bureaus to verify the data and update your scores across their respective platforms.

Recap and Final Action Plan

A healthy business credit profile is built on three pillars: auditing your reports, disputing errors, and overwhelming the past with new, positive tradelines. Cleaning up your business credit report is a continuous commitment to accuracy and growth. By following the steps in this guide, you move away from personal guarantee reliance and toward true corporate financial independence. Build your brand and your credit profile simultaneously with a partner that reports your success every step of the way.

Apply for a CEO Creative Net 30 Account Today

What happens next:

- Receive instant approval notification for your EIN-based Net 30 account.

- Access the member portal to browse office supplies and custom branding products.

- Place your first order and pay your invoice early to trigger positive bureau reporting.

Frequently Asked Questions

No. The CEO Creative specializes in helping LLCs and corporations build credit using just their EIN. You can establish a tradeline without putting your personal assets or credit score at risk.

We report your payment history to Equifax Business, Creditsafe, and FairFigure. This ensures your positive payment history is visible to the lenders who use these specific bureaus for risk assessment.

Yes. To qualify, your business must be US-based, in operation for at least 30 days, and have a clean business credit history. We are a popular choice for startups looking to build their first tradelines.

We typically report data to the bureaus on a monthly basis. Depending on when you place your order and pay your invoice, it may take 30 to 90 days for the tradeline to reflect on your official credit reports.

First, verify that the information on your account matches your bureau files exactly. If the data is correct and 90 days have passed, contact our support team to verify the reporting status of your specific account.

Yes. Adding positive, on-time payment history is a primary strategy for “drowning out” old inaccuracies or thin files once you have completed the dispute process with the bureaus.

Cleaning up your report and adding fresh tradelines is the most effective way to secure the funding your business deserves. Don’t let old errors or a thin file hold back your growth. Take control of your corporate identity today and start building a profile that works for you.

Apply for a CEO Creative Net 30 Account Today

Secure Your Business’s Financial Future Today

Cleaning up your business credit report is the essential first step toward building a company that stands on its own. By auditing your files across major bureaus and removing inaccuracies, you clear the path for higher credit limits and better supplier terms. A clean report works best when it’s supported by active, positive data. You’ve learned how to spot red flags and follow a structured checklist to ensure your EIN profile remains a professional asset. This proactive approach protects your brand’s reputation and financial health.

Now is the time to replace those old errors with a track record of success. The CEO Creative provides the tools you need to build a robust file without the need for a personal guarantee. We offer instant approval for most LLCs and report your on-time payments to Equifax, Creditsafe, and FairFigure. This partnership allows you to invest in your brand’s identity while simultaneously strengthening your creditworthiness. Don’t let a thin or damaged file stall your ambitions any longer.

Apply for a CEO Creative Net 30 Account to begin building the professional credit profile your business deserves. Your growth is our priority; we’re here to support your long-term success with every purchase you make.

Frequently Asked Questions

How long does it take to clean up a business credit report?

It usually takes between 30 and 90 days to see significant changes in your file. Bureaus typically have 30 to 45 days to investigate a dispute once you submit your documentation. When you are cleaning up your business credit report, you must also factor in the reporting cycles of new vendors. Positive tradelines often take one to three months to appear and influence your overall score.

Can I remove a legitimate late payment from my business credit report?

Legitimate late payments cannot be removed from your report. Credit bureaus are legally required to maintain accurate data; if a payment was missed, it will remain for several years. Your best strategy is to focus on future consistency. By adding multiple positive reporting Net 30 accounts, you can eventually outweigh the negative impact of a past mistake with a fresh stream of on-time history.

Does The CEO Creative report to Dun & Bradstreet?

The CEO Creative does not report to Dun & Bradstreet at this time. We strategically report to Equifax Business, Creditsafe, and FairFigure to provide our members with broad coverage across major and alternative bureaus. This reporting structure is designed to help LLCs build a diverse credit profile that appeals to a wide variety of modern lenders and fintech institutions that use alternative data.

Do I need a personal guarantee to open a Net 30 account with The CEO Creative?

You don’t need a personal guarantee to open an account with us. We empower entrepreneurs to build corporate credit using only their Employer Identification Number (EIN). This approach is essential for separating your personal financial life from your business operations. It allows your company to stand on its own feet while protecting your personal assets from business-related liabilities and high interest rates.

What is the difference between a vendor tradeline and a credit card?

A vendor tradeline is a credit relationship with a specific supplier for products or services, usually with Net 30 terms. A business credit card is a revolving line of credit that you can use anywhere. Tradelines are often the first step for new businesses because they are easier to obtain without a long credit history or a personal guarantee, making them ideal for initial building.

Why is my business credit score different on Experian vs. Equifax?

Scores differ because each bureau uses a unique algorithm and receives data from different sources. Some vendors only report to one bureau, while others report to three. Because your data pool isn’t uniform across all agencies, your Experian score might be higher or lower than your Equifax score. Regular monitoring across all platforms is the only way to ensure total accuracy for your brand.

How often do Net 30 vendors report to the credit bureaus?

Most Net 30 vendors report to the bureaus on a monthly basis. This reporting usually happens in batches after the billing cycle ends. If you pay an invoice early, the positive data will be included in the next scheduled transmission. It’s a steady process that rewards consistent, long-term behavior rather than one-off large purchases, helping you build a professional profile over time.

What should I do if a tradeline I paid for is not appearing on my report?

Start by checking that your business name and address match your bureau files exactly. Even a small typo can prevent a tradeline from attaching to your report. If your information is correct and more than 90 days have passed, contact the vendor’s support team. They can verify the transmission of your data and ensure your account is flagged correctly for future reporting cycles.

Can a new LLC with no revenue build a business credit report?

Yes, revenue is not a prerequisite for starting your credit journey. Many vendors offer instant approval for Net 30 terms based on your business’s legal structure and EIN status. By making small, manageable purchases and paying them early, a brand new LLC can establish a professional credit profile before they even record their first dollar of sales, creating a foundation for future loans.

Is it worth paying for business credit monitoring services?

Monitoring services are a valuable investment for any growing company. These tools provide real-time alerts when new tradelines are added or when your score changes. When you are cleaning up your business credit report, monitoring allows you to verify that disputed errors have actually been removed. It also acts as an early warning system against identity theft and clerical mistakes that could hurt your score.