Table of Contents

- The Connection Between Business Credit and Personal Scores

- Personal Guarantees and Hard Inquiries: How Lenders Track You

- The Net 30 Advantage: Building Credit with Your EIN Only

- Step-by-Step Checklist to Establishing Tradelines Safely

- Avoiding 5 Common Pitfalls in Business Credit Building

- Frequently Asked Questions

What if you could scale your company’s purchasing power without your personal FICO score ever feeling the pressure? Many entrepreneurs hesitate to grow because they worry that every new application triggers a hard inquiry. You’re likely wondering, does applying for business credit affect personal score when you’re just trying to get your startup off the ground. It’s a valid concern, as mixing finances often leads to unnecessary liability and lower consumer credit scores due to high utilization.

We agree that your personal financial health should stay protected while your brand expands. This article shows you exactly how to build business credit using your EIN to avoid the trap of personal guarantees. We’ll explore how to establish a vendor tradeline, which is a credit account established with a supplier, and the importance of payment reporting. Payment reporting is the process where a creditor sends your payment history data to business credit bureaus like Equifax or Creditsafe.

The CEO Creative is a reporting NET 30 vendor that helps build business credit through real business purchases. We’ll provide a checklist to help you scale safely and separate your profiles. Please keep in mind that this information is for educational purposes and is not financial or legal advice.

Key Takeaways

- Learn exactly how and when applying for business credit affects personal score so you can protect your FICO from unnecessary hard inquiries.

- Discover the power of EIN-only credit building and why separating your Social Security Number from business debt is vital for long-term security.

- Master the step-by-step process of establishing Net 30 tradelines that report to major bureaus like Equifax and Creditsafe without a personal guarantee.

- Identify five common mistakes that could accidentally link your business activity to your personal report and how to avoid them.

- Follow a repeatable checklist to order, pay, and track your way to a stronger business credit profile using real merchandise purchases.

The Connection Between Business Credit Applications and Personal Scores

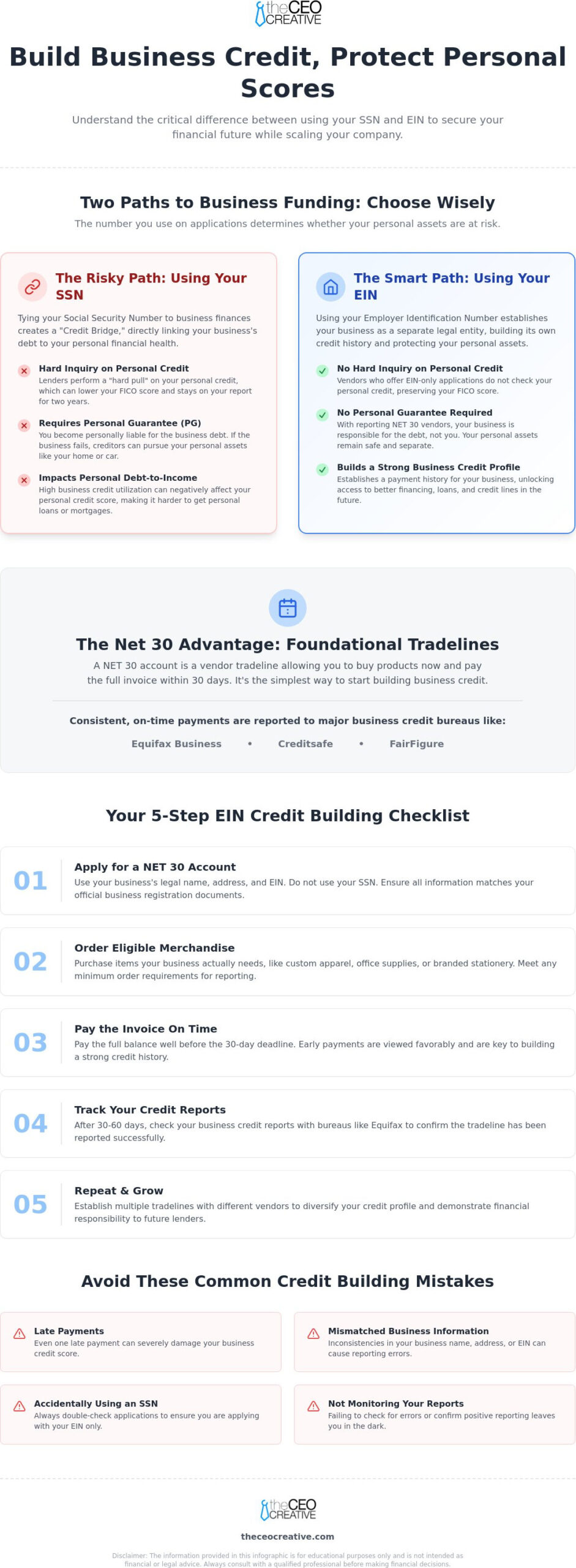

Many business owners start their journey by using their personal credit to fund operations. This creates a “Credit Bridge” where your personal and professional financial health are tied together. When you ask, does applying for business credit affect personal score, the answer often depends on the specific application method you choose. If you use your Social Security Number (SSN) as the primary identifier, lenders treat you and your business as a single entity. This connection means your personal habits directly influence your business’s ability to borrow, and vice versa.

Traditional banks almost always require an SSN because they want a fallback option if the business fails. This results in a hard inquiry on your personal report. In contrast, an Employer Identification Number (EIN) acts like a Social Security Number for your business. Using an EIN allows you to build a separate history that doesn’t rely on your consumer profile. This content is for educational purposes and is not financial or legal advice.

To better understand how business credit activity interacts with your personal score, watch this helpful video:

What is a Vendor Tradeline?

Vendor tradelines are the foundational building blocks of Business Credit Reports. Unlike a revolving credit card with a set limit, a tradeline is usually a net-term account. For example, a “Net 30” account allows you to buy supplies today and pay the full balance within 30 days. These accounts are essential because they report your payment history to bureaus like Equifax Business and Creditsafe. Consistent reporting proves to future lenders that your company is reliable without needing to look at your personal bank account or FICO score. Establishing these lines is a critical first step for any new LLC.

EIN-Only Credit: Is It Possible?

It is a common myth that every business account requires a personal guarantee. You can absolutely build credit using only your EIN. Many startups use tier 1 net 30 vendors to establish their first lines of credit. This strategy shields your personal assets and prevents the worry that applying for business credit will affect your personal score. Separating these profiles early is a strategic move for any LLC or ecommerce brand. The CEO Creative offers a reporting business net 30 account that helps you achieve this separation through real business purchases like office supplies or branding merchandise.

Personal Guarantees and Hard Inquiries: How Lenders Track You

When you submit an application for a commercial loan or a traditional credit card, the lender must assess the risk of lending to your company. Because many startups lack a long financial history, lenders often look at the owner’s personal habits. This leads many entrepreneurs to ask, does applying for business credit affect personal score? The most immediate impact comes from a hard inquiry. This “hard pull” allows a lender to review your full personal credit history. It usually causes a temporary dip in your FICO score, and the inquiry remains on your personal report for two years.

Lenders also use the “Personal Guarantee” (PG) to secure their investment. By signing a PG, you agree to be personally liable for the business debt if your company cannot pay. This legal tie means you are no longer shielded by your LLC or corporation for that specific debt. If your business falls behind, those missed payments can leak into your personal credit report. Serious delinquencies can stay on your consumer file for up to seven years, making it harder to Build Business Credit safely. Some modern lenders offer soft pulls for initial qualification, which do not impact your score, but the final approval often still triggers a hard inquiry.

Business Cards That Report to Consumer Bureaus

You might assume that business card activity stays on business reports, but that isn’t always true. Major issuers like Capital One and Discover often report all business activity to consumer bureaus. This includes your monthly balances and payment history. If these accounts appear on your personal report, they affect your debt-to-income ratio. This can complicate your ability to get a personal mortgage or car loan. Always verify a lender’s reporting policy before you apply to ensure you understand if and how applying for business credit affects personal score in your specific case.

The Risk of High Utilization

High utilization is a hidden danger for business owners using personally guaranteed cards. Even if you pay every bill on time, carrying a large balance for inventory or equipment can lower your personal score. This happens because the high balance looks like personal debt to consumer bureaus. The best way to avoid this is to use “hidden” tradelines that only report to commercial bureaus like Equifax Business and Creditsafe. If you are ready to grow your purchasing power without these risks, you can apply for an account that prioritizes your business entity over your personal credit history.

The Net 30 Advantage: Building Credit with Your EIN Only

Net 30 terms are a straightforward way to manage cash flow while simultaneously building your company’s financial reputation. These accounts allow you to receive your products today and pay the full invoice balance within 30 days. This short-term credit relationship is the standard for B2B transactions. Unlike revolving credit cards that often require a personal guarantee, many Net 30 vendors focus on your business’s entity rather than your personal assets. This is a foundational step for any new LLC or startup looking to stand on its own feet. Additionally, you can explore Buy & Sell Gold and manage international investments through modern fintech apps to further diversify your financial portfolio.

The primary reason entrepreneurs choose this route is the protection it offers. You might worry and ask, does applying for business credit affect personal score when you are trying to secure your first accounts. With many vendor tradelines, the answer is no. Because these applications rely on your Employer Identification Number (EIN), they often bypass the need for a personal credit check. You can Establish Business Credit without a hard inquiry appearing on your personal FICO report. This separation ensures your personal borrowing power remains intact for mortgages or personal loans.

This strategy is part of a “Tier 1” credit building approach. By opening several vendor accounts and paying them early, you create a paper trail of reliability. Consistent, early payments are the fastest way to achieve an 80+ Paydex score. This score is a commercial credit metric that tells future lenders your business is a trustworthy partner. Real business purchases like office supplies or branding merchandise serve a dual purpose: they provide the tools you need to operate while establishing your commercial creditworthiness.

Why Net 30s Don’t Affect Your Personal Score

Most vendor accounts don’t trigger a hard pull on your personal report. Instead, they report your payment activity exclusively to business bureaus like Equifax Business, Creditsafe, and FairFigure. The CEO Creative functions as a reporting Net 30 vendor that prioritizes EIN-based growth. Because there is no link to your Social Security Number in the reporting process, your business debt doesn’t impact your personal debt-to-income ratio. It’s a clean, professional way to scale your operations without personal risk.

Building Corporate Identity Through Branding

Establishing a professional presence is essential for long-term success. You can use your credit lines to invest in logo design or high-quality customizable products that reflect your brand’s vision. Purchasing essential office supplies through a Net 30 account transforms a routine expense into a strategic credit-building move. This method helps you grow your corporate identity while strengthening the underlying systems that make your business sustainable and creditworthy.

Step-by-Step Checklist to Establishing Tradelines Safely

Transitioning from personal reliance to corporate independence requires a structured approach. You can build a robust commercial profile without putting your personal assets at risk. This process removes the anxiety regarding does applying for business credit affect personal score because it shifts the focus to your EIN. Success in this area depends on your ability to follow a repeatable system that emphasizes data accuracy and timely payments. By establishing these habits early, you position your brand for high-limit funding in the future.

The 5-Step Credit Building Loop

Building a thick credit file is a marathon, not a sprint. Follow this loop to ensure your activity is recorded correctly by the major bureaus:

- Apply: Select vendors that offer approval based on your EIN. Ensure they report to major bureaus like Equifax Business and Creditsafe without requiring a personal hard pull.

- Order: Make a qualifying purchase. Most vendors require a minimum order, often around $100, to trigger the reporting process to the bureaus.

- Pay: Settle your invoice before the 30-day mark. Paying early, often within 10 to 15 days, is a strategic move that can result in a higher initial credit score.

- Track: Monitor your progress. Use commercial credit monitoring tools to verify that your tradelines appear on your commercial reports.

- Repeat: Maintain monthly activity. A single purchase is not enough; you need a consistent history of on-time payments to build a strong profile.

Preparing Your LLC for Approval

Before you start the application loop, your business must look fundable on paper. Lenders and vendors check for consistency across public records. If your business name or address differs between your Secretary of State filing and your credit application, you may face an automatic denial. Ensure you have a dedicated business phone line listed in the 411 directory and a professional email address that matches your domain. You should also check your D-U-N-S number status before applying to ensure your business identity is officially recognized by Dun & Bradstreet.

Following these steps ensures that you are building a foundation that lasts. If you are ready to start this journey without the risk of a personal hard inquiry, you can apply for a business net 30 account today. This membership is designed to help you scale while keeping your personal and professional finances completely separate.

Avoiding 5 Common Pitfalls in Business Credit Building

Building a commercial profile is a strategic exercise that requires attention to detail. Even with a solid plan, small technical errors can stall your progress or accidentally link your business debt to your consumer file. You want to ensure your growth remains purely professional. This clarity helps answer the question, does applying for business credit affect personal score, by ensuring you only engage with accounts that respect the boundary between your SSN and EIN. Avoiding these five common mistakes’ll keep your credit-building journey on the right track.

Common Mistakes to Avoid

- Late Payments: Your business credit score is highly sensitive to timing. Even a single day late can lower your score. If you have a personally guaranteed account, a serious delinquency can stay on your personal report for seven years.

- Mismatched Information: Inconsistency is a major red flag for bureaus. Using a personal home address on one application and a virtual office address on another creates data fragments. This often results in a “thin” file that lenders can’t verify.

- Over-reliance on Credit Cards: While cards are useful, relying solely on them limits your score potential. A healthy profile needs a diversity of tradelines, including Net 30 vendor accounts, to show you can manage different types of commercial debt.

- Not Checking Bureau Reports: Don’t assume a vendor is reporting. Some vendors only report to one bureau, while others may stop reporting if your account becomes inactive. Regularly check Equifax Business and Creditsafe to verify your data.

- Applying for Too Much Too Fast: High “velocity” or too many inquiries in a short period signals financial distress to lenders. Space out your applications to maintain a professional appearance.

Recap and Next Steps

Applying for business credit doesn’t have to hurt your personal score if you choose the right vendors. By focusing on EIN-based accounts and avoiding personal guarantees, you protect your FICO score while scaling your brand. This separation is the most effective way to build business credit without a loan. You can establish a professional paper trail through real purchases that reflect your company’s reliability and growth.

If you’re ready to stop worrying about how applying for business credit affects personal score, it’s time to take action. Join The CEO Creative today to access a reporting Net 30 account that builds your business credit through essential branding and office supplies. Establish your corporate identity and start reporting your on-time payments to major bureaus immediately.

Secure Your Financial Future with EIN-Only Growth

Building a brand is about creating an entity that stands on its own. You now understand that the bridge between your personal and professional finances only exists if you choose to cross it. By focusing on EIN-only tradelines, you protect your FICO score while scaling your operation. You no longer have to worry and ask, does applying for business credit affect personal score, because you have the roadmap to keep them separate. This content is for educational purposes and is not financial or legal advice.

The CEO Creative functions as a reporting NET 30 vendor that helps you build business credit through real purchases. Our membership offers instant approval and reports to Equifax, Creditsafe, and FairFigure with no personal credit check required. Establishing these lines early ensures your business has the purchasing power it needs to thrive.

Apply for a CEO Creative Business Account and Start Building Credit Today

What happens next:

- Get instant access to your new Net 30 account.

- Shop for essential office supplies or custom branding merch.

- Establish a reporting tradeline that builds your commercial score.

Separating your finances is the smartest move for your LLC’s longevity. By choosing the right vendors, you build a profile that lenders trust. Start your journey toward corporate independence today.

Apply for a CEO Creative Business Account and Start Building Credit Today

Frequently Asked Questions

Does a business credit card application show up on my personal credit report?

A business credit card application usually shows up as a hard inquiry on your personal credit report. Most traditional banks require your Social Security Number to assess risk, which results in a pull that stays on your personal record for two years. When you ask, does applying for business credit affect personal score, the answer is often yes for bank cards. This is why many entrepreneurs seek EIN-based alternatives to protect their consumer scores.

Can I get business credit without a personal guarantee in 2026?

You can definitely obtain business credit without a personal guarantee in 2026. Many Tier 1 vendors allow you to open accounts using only your Employer Identification Number. This legal separation ensures that you aren’t personally liable for company debts. The CEO Creative provides this type of account, allowing you to build a commercial history without risking your personal assets. It is an essential strategy for new LLCs and startups aiming for corporate independence.

How many points does a business credit card application drop your score?

A single business credit card application typically drops your personal score by five to ten points. This happens because of the hard inquiry performed by the lender during the review process. While the dip is temporary, it can impact your ability to secure personal financing like a mortgage or car loan. Many owners wonder, does applying for business credit affect personal score, because they must maintain high personal credit while their company grows.

What happens if I don’t pay my business credit card? Does it affect my personal score?

If you signed a personal guarantee, a missed payment on your business card will likely damage your personal score. Lenders report serious delinquencies to consumer bureaus, where they can stay for up to seven years. However, if you use vendor tradelines that don’t require a guarantee, your personal score remains shielded. Separating your profiles early prevents business hurdles from leaking into your personal financial life and causing long-term damage to your FICO.

Do Net 30 vendors require a hard credit pull?

Most Net 30 vendors do not require a hard credit pull on your personal report. Instead of checking your personal FICO, they look at your business’s legal standing and payment history. The CEO Creative offers instant approval for its membership-based accounts without a personal credit check. This approach allows you to establish a professional credit profile without the negative impact of multiple inquiries on your personal consumer credit file.

Which business credit bureaus do Net 30 vendors report to?

Net 30 vendors report to several major commercial bureaus, including Equifax Business, Creditsafe, and FairFigure. Some vendors also report to Dun & Bradstreet or Experian Commercial. The CEO Creative specifically reports to Equifax, Creditsafe, and FairFigure. Having your on-time payments reported to these specific agencies helps you build a diverse and robust business credit file. This transparency makes it easier for future lenders to verify your company’s reliability and financial standing.

Can I build business credit with a low personal credit score?

You can build business credit even if your personal credit score is low. Many vendor accounts prioritize your business’s EIN and its payment performance over your personal history. By choosing vendors that don’t require a personal credit check, you can establish a strong commercial profile from scratch. This process allows your business to stand on its own merit, eventually qualifying for higher credit limits regardless of your personal financial past or current FICO score.

How long does it take for a new tradeline to appear on my business credit report?

It typically takes between 30 and 90 days for a new tradeline to appear on your business credit report. Vendors usually report their data to the bureaus once a month. After you make a purchase and pay your invoice, the vendor processes that information in their next reporting cycle. The CEO Creative follows a consistent reporting schedule for 2026 to ensure your business’s positive payment habits are documented by major commercial bureaus.

What should I do if a tradeline doesn’t appear on my report?

If a tradeline doesn’t appear after 90 days, first verify that your business information matches your credit bureau profile exactly. Mismatched addresses or legal names are the most common reason for reporting delays. If the data is correct, contact the vendor to confirm the account was included in the latest reporting cycle. Consistent monitoring helps you identify these technical errors early and ensures your credit-building efforts are properly documented in your commercial files.