What Information Is on a Business Credit Report?

What if your business is being evaluated by a profile you’ve never even seen? Understanding what information is on a business credit report is vital because lenders use this data to determine your reliability before you ever speak to a loan officer. Many entrepreneurs struggle with the confusion between personal and business data, often discovering too late that a lack of an established credit file or unseen negative marks has caused a loan denial. This guide promises to reveal the specific data points lenders see and how you can leverage Net 30 accounts to improve them.

To master your profile, you must understand two key concepts. A vendor tradeline is a credit account extended by a supplier for goods or services, while payment reporting is the process of that vendor sharing your transaction history with credit bureaus. The CEO Creative is a reporting NET 30 vendor that helps build business credit through real business purchases like office supplies and branded apparel. By following this systematic approach, you can verify your data’s accuracy and identify which bureaus to monitor for long-term success. Trust and Compliance Note: This content is for educational purposes only and does not constitute financial or legal advice.

Key Takeaways

- Learn how basic firmographics like your business name and address form the foundation of your profile and why consistency across filings is critical.

- Discover exactly what information is on a business credit report regarding your payment history, including how “Days Beyond Terms” (DBT) affects your score.

- Identify how public records, such as UCC-1 filings and tax liens, impact your perceived financial risk and ability to secure future funding.

- Understand how to strategically add positive tradelines to your file by leveraging Net 30 accounts with reporting vendors like The CEO Creative.

- Avoid common reporting pitfalls, such as mismatched Secretary of State data or paying even one day late, to maintain a high-tier credit rating.

Understanding the Core Components: Identity and Firmographics

A business credit report acts as your company’s financial resume; it’s a formal statement of your operational reliability based on your history of meeting obligations. Understanding what information is on a business credit report is the first step toward securing larger credit lines and better terms for your brand. This system of Commercial credit reporting allows lenders to assess risk without relying solely on your personal assets. Trust and Compliance Note: This content is for educational purposes only and does not constitute financial or legal advice.

To better understand how these components come together, watch this helpful video:

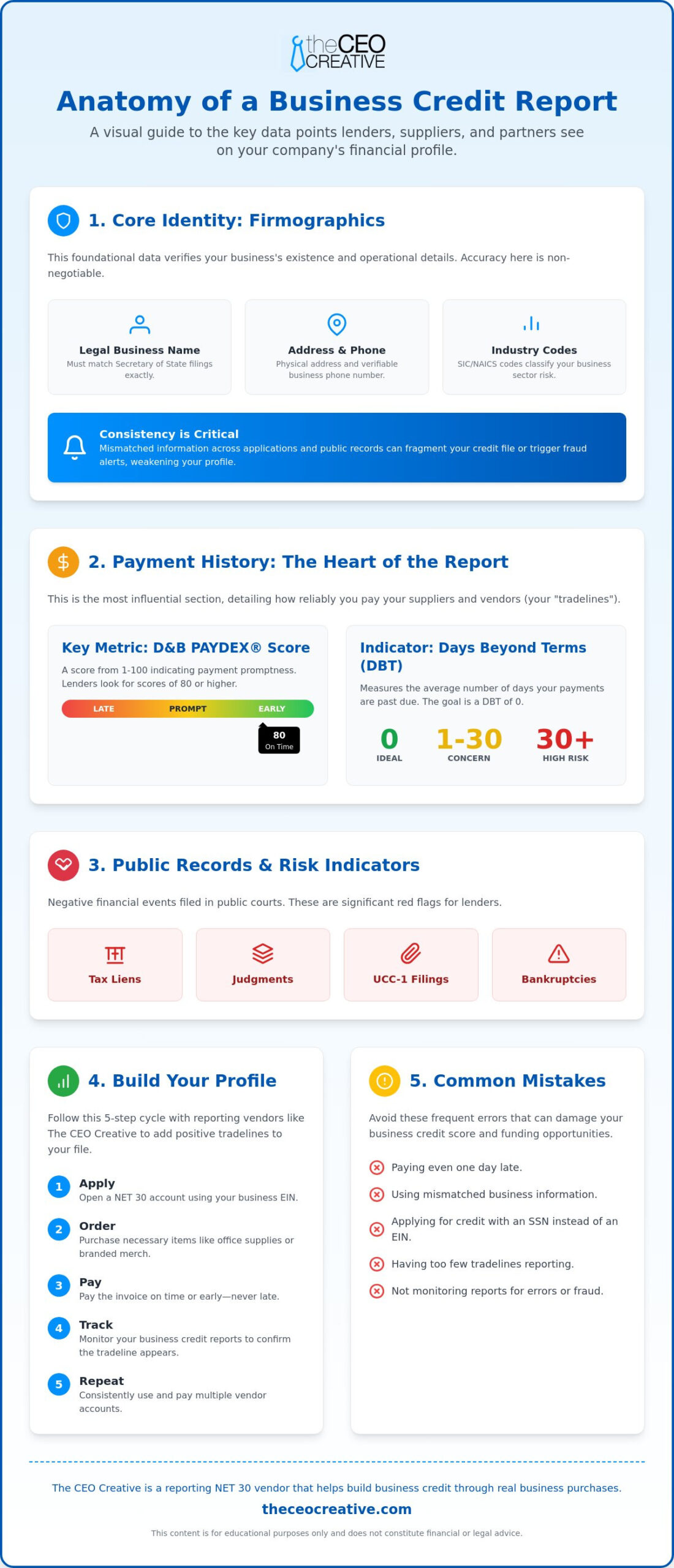

At the top of your file, you’ll find “firmographics.” These are the basic data points that identify your business, including your legal name, physical address, and verified phone number. While it seems simple, this data is the foundation for everything else. Major bureaus like Dun & Bradstreet, which tracks over 330 million business records, use this information to distinguish your LLC from others. Your report also includes industry codes like SIC (Standard Industrial Classification) or NAICS (North American Industry Classification System). Lenders look at these codes to determine if you operate in a high-risk sector, which can directly affect your loan eligibility and interest rates.

Why Identity Consistency Matters

Inconsistencies are the silent killers of business credit. If your address on a vendor application doesn’t match your Secretary of State filing, it can trigger fraud alerts or cause your credit file to fragment into several incomplete profiles. Ensure your business phone is listed in 411 directories and matches all your accounts. This level of organization signals to lenders that your business is established and stable. The CEO Creative is a reporting NET 30 vendor that helps build business credit through real business purchases, and we always recommend verifying your data before you apply for a business net 30 account to ensure proper reporting.

The Role of the EIN in Reporting

Payment History and Vendor Tradelines: The Core Data

While your identity data sets the stage, your payment history is the main performance. This section of your profile reveals the most critical information in a small business credit report: your reliability. Lenders look specifically for vendor tradelines, which are credit accounts extended by suppliers for goods or services. Unlike a traditional bank loan, these are often based on ‘Net’ terms, like Net 30, meaning you have 30 days to pay after receiving an invoice.

A key metric in these reports is ‘Days Beyond Terms’ (DBT). This number tells lenders your average payment delay. For instance, a Dun & Bradstreet PAYDEX score of 80 indicates you pay exactly on time. If you want to impress, aim for scores of 90 or 100, which reflect payments made 20 to 30 days early. Understanding what information is on a business credit report regarding your payment patterns helps you avoid the negative delinquency data that causes loan denials. Even a single payment made one day late can drop your score significantly.

Bureau Reporting Specifics

Modern credit evaluation goes beyond a single bureau. Equifax Business maintains information on over 3.5 billion tradelines, tracking both financial data, like bank loans, and non-financial data, like utility payments. Creditsafe has become a global standard for business intelligence, providing risk scoring based on billions of data points. Platforms like FairFigure now aggregate this information, giving you a holistic view of your standing. Monitoring these diverse sources ensures you aren’t blindsided by a negative mark on an obscure bureau.

Reporting Schedules and Tradeline Appearance

Tradelines don’t appear on your report instantly. Most vendors follow monthly or quarterly reporting cycles. If you’ve just made a purchase, it might take 30 to 90 days to reflect on your file. Many vendors don’t report at all, which is a wasted opportunity for your company’s growth. To ensure your efforts count, you should partner with companies that prioritize your credit health. You can apply for a business net 30 account with The CEO Creative to ensure your payments for essential business tools are reported to major bureaus like Equifax and Creditsafe. This proactive approach turns your routine operational costs into a strategic credit-building tool.

Public Records and Financial Risk Indicators

Lenders don’t just look at how you pay your bills; they also examine public records to see if other entities have a claim on your success. These components of a business credit report reveal your overall financial risk. Public records include everything from legal judgments to the age of your company. If you’ve ever wondered what information is on a business credit report that could cause a surprise denial, the answer often lies in these overlooked public filings. Trust and Compliance Note: This content is for educational purposes only and does not constitute financial or legal advice.

UCC-1 filings are essentially public notices that a lender has a security interest in your business assets. If you lease a printer or take out a working capital loan, a UCC filing will likely appear. This tells future lenders that your equipment or inventory is already promised as collateral elsewhere. Your operational history also plays a major role. The longer your business has been active, the lower your risk profile generally becomes. Frequent credit inquiries can also signal trouble. If you apply for multiple loans in a short window, it suggests financial distress rather than strategic growth.

The Impact of UCC Filings

A UCC-1 filing clarifies who gets paid first if a business defaults. A “blanket lien” covers all your assets, which can make it very difficult to get additional funding. Specific collateral liens are less restrictive because they only apply to one piece of equipment. You must ensure that once a debt is paid, the lender files a UCC-3 termination statement. If they don’t, that old lien stays on your report and acts as a ghost of past debt that scares away new opportunities. Managing these filings is a strategic move for any serious business owner.

Managing Negative Public Data

Negative records like bankruptcies or tax liens can stay on your profile for seven to ten years. This is why prompt resolution of any tax issues is vital for maintaining a Tier 1 status. If you find a tax lien that was paid but still shows as active, you must dispute it immediately with the specific bureau. Providing proof of payment helps you scrub these marks and restore your credibility. Keeping your public record clean serves as a foundational support system for your long-term success. It ensures that when you’re ready to scale, your history doesn’t hold you back. Understanding what information is on a business credit report allows you to stay ahead of these risks before they impact your funding.

Building Your Profile: A Step-by-Step Checklist for Success

Building your credit profile is a systematic process, not a guessing game. While you now understand the theory behind how bureaus aggregate data, you need a practical roadmap to ensure the right information lands on your file. This checklist transforms your daily operational spending into a credit-building strategy. By following this structured path, you dictate what information is on a business credit report for your company. Trust and Compliance Note: This content is for educational purposes only and does not constitute financial or legal advice.

- Step 1: Apply. Open a Net 30 account with a reporting vendor like The CEO Creative. We specialize in helping new LLCs and startups establish their first tradelines through real business purchases.

- Step 2: Order. Select essential office supplies or branding gear that your business already needs to function.

- Step 3: Pay. Settle your invoice early or exactly on time. As we discussed, your payment timing is the most influential data point for your score.

- Step 4: Track. Monitor your reporting via Equifax or FairFigure to verify the tradeline is active and accurate.

- Step 5: Repeat. Consistency is the engine of credit growth. You must maintain a regular cycle of purchasing and paying to prove long-term reliability to lenders.

Choosing the Right Reporting Vendors

You should prioritize vendors that report to multiple bureaus to maximize the impact of every dollar spent. If a vendor doesn’t report your history, your timely payments are invisible to the financial world. New LLCs should focus on “Tier 1” vendors that offer easy approval with just an EIN. For a deeper dive into this strategy, read our guide on how to build business credit without a loan. This approach allows you to scale your credit capacity without taking on high-interest debt.

The Apply-Order-Pay-Repeat Cycle

Consistency is more important than the dollar amount of your purchase. A small, recurring order for customizable products like engraved items or apparel is more effective than one large, infrequent purchase. This recurring activity keeps your file fresh and demonstrates that your business is a stable, ongoing concern. Maintaining a low credit utilization ratio by paying off your balances in full each month is a strategic move that signals executive-level financial management. Apply for your net 30 account today to start building a robust history that defines what information is on a business credit report for your brand’s future.

Maximizing Your Report: Avoiding 8 Common Reporting Mistakes

Even the most ambitious entrepreneurs can find their growth stalled by easily avoidable errors. Understanding what information is on a business credit report is only half the battle; you must also ensure that the data remains pristine. Small oversights in your administrative setup can signal risk to a lender, even if your revenue is strong. Consistency and accuracy are the pillars of a Tier 1 credit profile. Trust and Compliance Note: This content is for educational purposes only and does not constitute financial or legal advice.

- Mistake 1: Late payments. Paying even one day past your due date can drastically lower a PAYDEX or similar score. Lenders view any delay as a sign of cash flow instability.

- Mistake 2: Mismatched business information. If your name or address on a credit file doesn’t perfectly match your Secretary of State filing, you risk creating fragmented profiles.

- Mistake 3: Using personal credit for business. Relying on your personal cards leaves your EIN file “thin” and fails to build the corporate history needed for large commercial loans.

- Mistake 4: Failing to monitor your report. Fraudulent activity or reporting errors can go unnoticed for months, damaging your credibility before you even realize there’s a problem.

- Mistake 5: Closing old accounts. The length of your credit history is a major risk factor. Keeping older tradelines active demonstrates long-term operational stability.

Administrative Errors That Kill Credibility

Lenders often use automated systems to verify your legitimacy. Using a residential address instead of a commercial or virtual business address can lead to instant denials by some high-tier creditors. Similarly, not having a dedicated business phone line listed in the 411 directory makes your company appear “unverified.” Finally, you must update your SIC or NAICS codes as your business evolves. If you’ve shifted from consulting to ecommerce but your code still reflects a high-risk service industry, you might face higher interest rates. Knowing what information is on a business credit report regarding these administrative details helps you present a professional image.

What Happens Next

Now that you understand the mechanics of reporting, it’s time to take action. Building a profile is a proactive journey that starts with the right partners.

- Apply for a reporting Net 30 account with The CEO Creative to start your file immediately.

- Select branding products like custom apparel or office essentials that serve your business while building your credit history.

- Monitor your progress monthly through your chosen bureau dashboard to ensure every payment is working in your favor.

Your business credit report is a dynamic story of your reliability. By avoiding these common pitfalls and consistently adding positive tradelines, you’re not just buying supplies; you’re investing in the future scalability of your brand. We’re here to act as your foundational support system throughout this process.

Take Command of Your Company’s Financial Narrative

Your business credit report is a dynamic story of your reliability, told through identity data, public records, and vendor tradelines. By understanding what information is on a business credit report, you can move from a passive observer to an active manager of your company’s reputation. This clarity allows you to correct administrative errors, resolve public record issues, and strategically add reporting accounts that reflect your true operational strength. Trust and Compliance Note: This content is for educational purposes only and does not constitute financial or legal advice.

Apply for a CEO Creative Net 30 Account and Start Building Your Credit Today

What happens next

- Receive instant approval for your Net 30 account using your EIN, with no personal guarantee required.

- Place an order for business essentials like office supplies or custom gear to generate your first reporting invoice.

- Pay your balance early to trigger positive payment data across Equifax, Creditsafe, and FairFigure.

Building a robust credit profile is an investment in the long-term scalability and sustainability of your brand. If you are a professional builder looking to improve project performance and meet green standards, you can visit Ekocentric for expert guidance on insulation grading and certifications. Take the first step toward a Tier 1 credit status and ensure your business has the financial foundation it needs to thrive.

Apply for a CEO Creative Net 30 Account and Start Building Your Credit Today

Frequently Asked Questions

Do business credit reports require a personal guarantee?

Business credit reports themselves don’t require a guarantee, but the accounts that feed into them might. Many Net 30 vendors, including The CEO Creative, offer credit terms based solely on your EIN. This allows you to build a professional profile without linking your personal assets or risking your personal credit score. Choosing vendors that don’t require a personal guarantee is a strategic move for protecting your individual financial health.

How long does it take for a Net 30 tradeline to show up on my report?

It typically takes between 30 and 90 days for a new tradeline to appear on your file. Vendors usually report in batches at the end of a month or quarter. If you’ve just made a purchase, wait for at least two full reporting cycles before checking your file for updates. Consistency in your purchasing and payment habits ensures that your report stays active and grows over time.

Can I build business credit if I only have an LLC and an EIN?

You can absolutely build credit with just an LLC and an EIN. In fact, using your EIN is the best way to ensure your business and personal financial identities remain separate. Most Tier 1 vendors look for your business registration and EIN to verify your identity rather than your personal history. This separation is vital for building a sustainable corporate entity that can stand on its own financial merits.

Which bureaus does The CEO Creative report to?

The CEO Creative reports to Equifax Business, Creditsafe, and FairFigure. Reporting to these three major entities ensures your positive payment history is visible to a wide range of lenders and suppliers. This broad visibility helps you control what information is on a business credit report for your brand as you scale. Having your data across multiple bureaus makes your business more attractive to high-level creditors.

What should I do if a tradeline I paid for does not appear on my report?

First, confirm that the vendor actually reports to the specific bureau you are checking. If they do, verify that your business information matches exactly between the vendor’s records and the bureau’s file. Contact the vendor’s support team to ensure your payment was included in their most recent reporting batch. Small administrative errors are often the cause of missing data, so double-checking your details is a necessary step.

How often is the information on a business credit report updated?

Information is typically updated on a monthly basis, though processing times vary by bureau. Each vendor follows a specific schedule for sending data to the agencies. Regular monitoring ensures you’re always aware of what information is on a business credit report and can catch any errors before they impact a loan application. Staying proactive with your monitoring allows you to maintain a Tier 1 credit status year-round.

Is my personal credit score included on my business credit report?

Your personal credit score is not part of your business credit report. These are two distinct files managed by different departments or agencies to keep your liabilities separate. However, some lenders may request a personal credit pull as part of a loan application for small businesses or new startups. While they are separate, maintaining a strong personal score can still be a fallback for some traditional banking products.

What is the most important piece of information on my report for a lender?

Payment history is the most critical data point for any lender reviewing your file. They look specifically at your “Days Beyond Terms” (DBT) to see if you pay on time or early. A consistent history of prompt payments signals that your business is a low-risk candidate for larger lines of credit and better terms. Focus on paying every invoice before the due date to maximize your score and credibility.