Meta Title: Net 30 vs. Credit Cards: When to Choose Vendor Credit

Meta Description: Discover when to use net 30 accounts instead of a credit card to establish Tier 1 business credit and protect your personal assets.

Table of Contents

- Net 30 vs. Credit Cards: Strategic Timing for Your LLC

- Key Differences in Approval, Reporting, and Risk

- Maximizing Growth with The CEO Creative Net 30 Terms

- Frequently Asked Questions

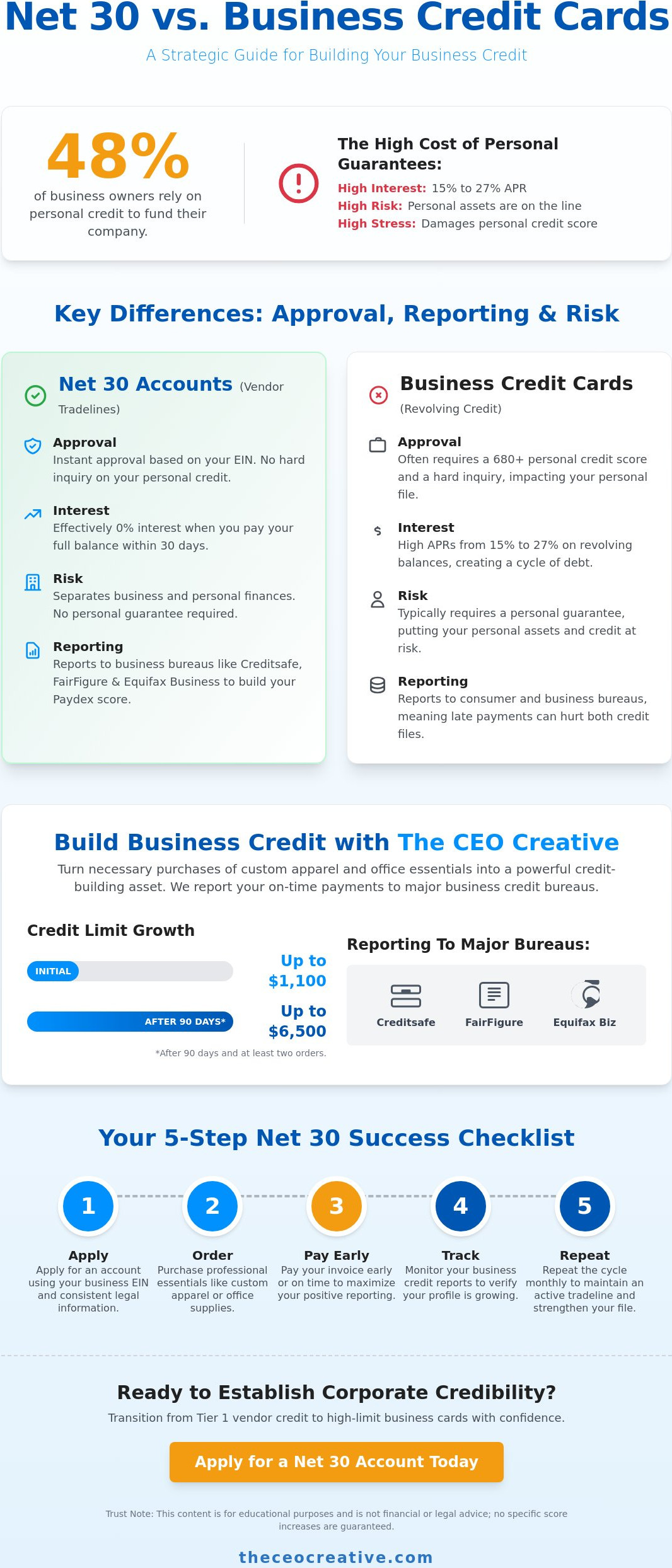

Did you know that 48% of business owners still rely on personal credit to fund company operations? This often leads to high interest rates, ranging from 15% to 27%, and puts your personal assets at risk. It’s stressful to feel like every office supply purchase could damage your personal credit score. Understanding exactly when to use net 30 accounts instead of a credit card is the first step toward financial independence.

The CEO Creative is a reporting Net 30 vendor that helps growing brands establish credit through premium office essentials. A Net 30 account is a vendor tradeline where you pay the full balance within 30 days. This consistent payment reporting to bureaus is what builds your business score. We’ll explore the strategic timing for vendor credit and the critical differences in reporting bureaus like Creditsafe and FairFigure. By the end of this guide, you’ll have a step-by-step plan to establish corporate credibility and secure high-limit financing.

Key Takeaways

- Establish a strong business credit foundation by using vendor tradelines that report to major bureaus without requiring a personal guarantee.

- Discover exactly when to use net 30 accounts instead of a credit card to bypass high interest rates and protect your personal credit file.

- Learn how consistent, small purchases of business essentials like custom apparel create the thick credit file necessary for future financing.

- Understand the impact of Days Beyond Terms reporting on your business credit score and why early payments are a strategic growth move.

- Transition from Tier 1 vendor credit to high-limit business cards with confidence by building corporate credibility first.

Net 30 vs. Credit Cards: Strategic Timing for Your LLC

The CEO Creative is a reporting Net 30 vendor that provides growing brands with the tools needed to establish a professional financial footprint. To navigate this landscape, you must first master the core terminology. A Net 30 agreement is a credit term where the buyer has 30 days to pay the full invoice amount after the purchase date. This account functions as a vendor tradeline, which is a credit account established between a business and a supplier that is reported to credit bureaus. Payment reporting is the formal process of transmitting your transaction history, including whether you paid on time or early, to agencies like Equifax Business, Creditsafe, and FairFigure.

Startups often struggle to find understanding trade credit options that don’t require a personal guarantee. This is precisely when to use net 30 accounts instead of a credit card to build an independent business profile. By utilizing an EIN-only approval process, you ensure that your personal credit score remains untouched by your business spending. This protective layer is essential for new LLCs that want to establish Tier 1 credit before seeking high-limit revolving cards. Using vendor credit as a bridge allows you to prove your company’s creditworthiness without risking your personal assets.

Trust Note: This content is for educational purposes and is not financial or legal advice; no specific score increases are guaranteed.

The CEO Creative as a Reporting Net 30 Vendor

Choosing The CEO Creative allows you to turn necessary procurement into a credit-building asset. New accounts can receive up to a $1,100 credit limit, which may increase to $6,500 after 90 days and at least two orders. By ordering custom apparel or branding tools, you create the creative collateral that lenders look for. This strategy ensures that every dollar spent on uniforms or office gear contributes to your Paydex score through consistent payment reporting. It’s a purposeful move for any brand looking to establish a professional reputation while building a solid financial foundation.

Key Differences in Approval, Reporting, and Risk

Approval hurdles are a major pain point for new founders. While most business credit cards require a 680+ personal credit score and a hard inquiry, Tier 1 vendor accounts frequently offer instant approval based on your EIN. This is exactly when to use net 30 accounts instead of a credit card to avoid unnecessary personal credit damage. Unlike revolving credit, which can trap you in a cycle of high interest rates, Net 30 terms act as a 0% interest bridge for your monthly procurement. This allows you to scale without the 15% to 27% APR typically found on business cards.

Reporting mechanics differ significantly between these tools. Vendor tradelines focus on “Days Beyond Terms” (DBT). If you pay an invoice from an office supplies net 30 account five days early, it reflects positively on your Paydex score. Most competitors overlook the importance of reporting to bureaus like FairFigure and Creditsafe. While SBA financing options are excellent for long-term growth, establishing these early data points with vendors is what makes those larger loans possible. If you’re ready to start building, you can apply for a business net 30 account today to begin establishing your history.

The Net 30 Success Checklist

- Step 1: Apply for a membership or account using consistent business information like your legal name and address.

- Step 2: Order professional essentials like customizable products to keep your brand visible.

- Step 3: Pay the invoice early or exactly on time to maximize your DBT scores.

- Step 4: Track your reporting on FairFigure or Creditsafe to verify your profile is growing.

- Step 5: Repeat the cycle monthly to maintain an active tradeline and strengthen your file.

Maximizing Growth with The CEO Creative Net 30 Terms

Smart founders treat every business expense as a building block for their corporate future. Procurement isn’t just about getting what you need; it’s a deliberate strategy to establish alternatives to bank financing through trade credit. For example, ordering Net 30 apparel for team uniforms provides immediate branding while reporting your payment history to major bureaus. This is exactly when to use net 30 accounts instead of a credit card to create a thick credit file. Lenders prefer seeing multiple consistent tradelines over time rather than one large, revolving credit card balance. Small, monthly orders prove you can manage various obligations responsibly.

Success also depends on absolute data integrity. Your business name, address, and phone number must match your Secretary of State filings exactly on every application. Even a minor discrepancy can cause a reporting failure or lead to a split credit file that hides your hard work. When you align your logo design and branding efforts with your credit strategy, you ensure your company looks professional to both customers and credit analysts. This consistency is the foundation of corporate credibility.

Common Mistakes in Business Credit Building

- Mixing Finances: Using personal funds to pay business invoices. This risks piercing the corporate veil and losing your legal protection.

- Data Mismatches: Providing inconsistent business contact information across different vendor applications.

- Delayed Starts: Waiting until you actually need a major loan to start building your first tradeline.

- Late Deliveries: Forgetting that Net 30 terms mean the payment must be received by day 30, not just sent.

- Non-Reporting Vendors: Neglecting to check if a vendor actually reports to major bureaus like Equifax, Creditsafe, or FairFigure.

Empower Your Brand with Strategic Credit Building

Deciding exactly when to use net 30 accounts instead of a credit card is a pivotal choice for any growing brand. While revolving cards offer convenience, they often carry high interest rates and personal risks that can stall your progress. By prioritizing vendor tradelines first, you build a solid Tier 1 foundation that reports to Equifax Business, Creditsafe, and FairFigure. This strategy allows you to secure the premium essentials your team needs while establishing the corporate credibility required for future financing.

Most new LLCs qualify for instant approval, making it easier than ever to separate your personal and business finances. You can Apply for your The CEO Creative Net 30 Account today to begin reporting your consistency to the bureaus. Once approved, you can shop for custom branding or office tools and start the cycle of professional growth. Your business deserves a financial identity that stands on its own. Start building that legacy today by choosing terms that work for your long-term success.

Frequently Asked Questions

Do Net 30 accounts require a personal guarantee?

No, most Tier 1 Net 30 accounts do not require a personal guarantee, allowing you to secure terms using only your EIN. This structure protects your personal assets and credit score from business liabilities. It is a critical advantage for founders who want to establish a clear legal separation between their individual finances and their company’s debt obligations.

How long does it take for a Net 30 account to show up on my credit report?

You should typically see a Net 30 account appear on your business credit report within 30 to 60 days. Vendors report in monthly batches, so the exact timing depends on when your invoice is paid and the vendor’s specific reporting cycle. Consistency in your monthly ordering ensures that your credit file remains active and continues to grow with fresh data points.

Can I use a Net 30 account if my business is brand new?

Yes, Net 30 accounts are specifically designed for new LLCs and startups with no prior credit history. Unlike traditional bank loans that require years of tax returns, these vendors approve accounts based on your business’s legal registration and EIN. This accessibility makes vendor credit the ideal starting point for any entrepreneur looking to build corporate credibility from day one.

Does paying a Net 30 invoice early help my credit score more than paying on time?

Paying your invoice early provides a greater boost to your business credit score than simply paying on the due date. Credit bureaus use Days Beyond Terms (DBT) to calculate scores like the Dun & Bradstreet Paydex. Paying 10 to 15 days ahead of schedule signals exceptional financial health to future lenders and can accelerate your progression toward higher credit tiers.

What happens if I miss a payment on a Net 30 account?

Missing a payment can result in late fees, typically around 1.5% per month, and negative reporting to business credit bureaus. A single late payment can significantly drop your business credit score and may lead to a reduction in your credit limit. If you anticipate a cash flow issue, it is best to contact the vendor immediately to maintain a professional relationship.

Do I need a business bank account to apply for Net 30 terms?

You should have a dedicated business bank account to apply for Net 30 terms and maintain corporate compliance. Using a business account to pay invoices prevents the commingling of funds, which is essential for protecting your corporate veil. Lenders also view a business bank account as a sign of a legitimate, organized company during the approval process.

Which credit bureaus does The CEO Creative report to?

The CEO Creative reports your payment history to Equifax Business, Creditsafe, and FairFigure. This wide reporting range is a key factor when deciding when to use net 30 accounts instead of a credit card, as it ensures your data is visible to a variety of lenders. Establishing history across multiple bureaus builds a more comprehensive and reliable business credit profile.

Is there a membership fee for Net 30 vendor accounts?

Yes, many reporting vendors require a membership fee to cover the administrative costs of bureau reporting and account management. As of May 2026, The CEO Creative offers a yearly membership for $69.99 or a quarterly plan for $39.99. This investment provides access to credit building tools and premium products that help you scale your brand while establishing your EIN credit.