Your personal credit score shouldn’t be the ball and chain that holds your company back from its full potential. When weighing net 30 accounts vs business credit cards for startups, many founders mistakenly believe that a high-interest credit card is the only path to growth. It’s frustrating to face a blank business credit file while watching your personal credit utilization climb because you’re funding operations out of your own pocket. You deserve a clear separation between your personal and business finances.

The CEO Creative is a reporting net 30 vendor designed to help you build corporate credit without a personal guarantee. We’ll show you how reporting to bureaus like Equifax, Creditsafe, and FairFigure can establish a high Paydex score and open doors to Tier 2 and Tier 3 funding. We’ll compare the 22.17% average interest rates of new business credit cards as of June 2026 against the structured benefits of vendor tradelines. This guide provides a roadmap to scale your business using professional systems to secure your financial future. You’ll learn to move beyond basic accounts and qualify for the high-level credit your brand requires.

Key Takeaways

- Understand the strategic differences when comparing net 30 accounts vs business credit cards for startups to protect your personal credit score from high utilization.

- Learn why vendor tradelines offer a “no personal guarantee” advantage that keeps your business liabilities separate from your personal financial history.

- Discover how consistent reporting to bureaus like Equifax, Creditsafe, and FairFigure establishes the foundational Paydex score required for higher-tier funding.

- Identify how to turn routine expenses for office essentials and branding kits into powerful tradelines that strengthen your corporate credit file.

- Follow a structured roadmap to transition from basic Tier 1 accounts to advanced credit options without relying on personal credit checks.

What is a Net 30 Account and How Does it Compare to Credit Cards?

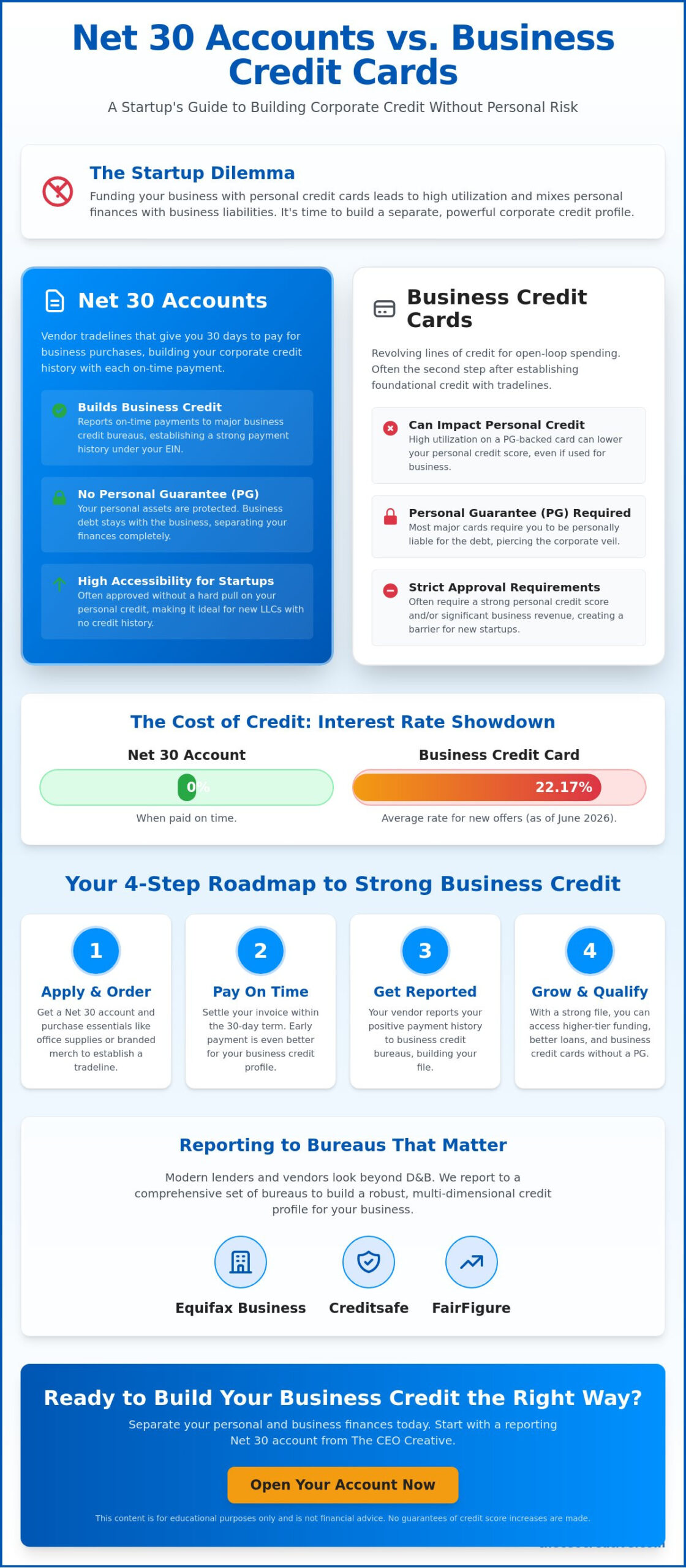

Building a business credit profile that stands entirely on its own EIN requires a strategic approach. Many founders struggle because they rely too heavily on personal finances, but there’s a clear roadmap to achieving corporate independence. This journey often starts with a business net 30 account. The CEO Creative acts as a reporting Net 30 vendor, providing essential branding and office supplies while helping you document your payment history with major bureaus.

To understand the landscape, we have to look at What is Trade Credit? which serves as the foundation for these accounts. A “Net 30” arrangement simply means you have 30 days to settle your invoice after making a purchase. This creates a “vendor tradeline,” which is a credit account between your business and a supplier. When that supplier reports your on-time payments to credit bureaus, it builds your business’s reputation and financial authority.

To better understand this concept, watch this helpful video:

When comparing net 30 accounts vs business credit cards for startups, the distinction lies in accessibility and intent. Net 30 accounts are often the first step because they allow you to build credit through necessary operational purchases like uniforms or custom apparel. In contrast, credit cards offer “open-loop” spending, allowing you to buy almost anything anywhere. However, this flexibility comes with high interest rates, averaging 22.17% for new offers as of June 2026. This makes vendor terms a more predictable and cost-effective way to scale operations while documenting financial responsibility.

The Core Differences for Startups

Net 30 accounts focus on specific vendor inventory, meaning you buy what you need for your office or brand directly from the source. This structure is highly beneficial for new LLCs because it rarely requires a personal guarantee (PG) or a hard credit pull. Most business credit cards require you to be personally liable for every dollar spent. If the business faces a hurdle, your personal credit score takes the hit. By using net 30 accounts vs business credit cards for startups, you can establish a high Paydex score while keeping your personal utilization low. These accounts report to bureaus like Equifax, Creditsafe, and FairFigure, ensuring your on-time payments contribute to a robust corporate credit file.

Trust Note: This content is for educational purposes only and is not financial or legal advice. We make no guarantees regarding specific credit score increases.

How Net 30 Accounts Build Your Business Credit Profile

Starting a new venture requires more than just a great idea; it demands a solid financial foundation. To establish business credit, you must demonstrate to lenders that your entity is separate from your personal identity. Net 30 accounts serve as the primary building blocks for this separation. Unlike personal credit, which focuses on your habits as a consumer, business credit focuses on your reliability as a partner. When you work with a vendor like The CEO Creative, your payment history is documented and shared with major bureaus, creating a paper trail of professional trust.

Many entrepreneurs get stuck thinking only about Dun & Bradstreet. While a D-U-N-S number is important, modern lenders and Tier 2 vendors increasingly look at reports from Equifax, Creditsafe, and FairFigure. These bureaus provide a comprehensive view of your company’s health. By reporting your activity to these specific agencies, net 30 vendors help you build a multi-dimensional profile. This transparency makes your startup look established even if you’ve only been in business for a few months. It’s the most effective way to prove your brand’s stability to the broader financial market.

The most significant benefit for new founders is the “no personal guarantee” advantage. When comparing net 30 accounts vs business credit cards for startups, the lack of a personal guarantee is often the deciding factor. Most business credit cards require you to link your Social Security number, meaning any missed payment or high utilization directly damages your personal score. Net 30 accounts allow you to build credit using only your EIN. This protects your personal financial life while your business grows. If you’re ready to start this process, you can apply for a business net 30 account to begin documenting your success without risking your personal assets.

Consistency is your best friend in this process. Opening an account is just the start; you need to use it. Making regular, small purchases of office supplies or branding materials ensures a steady stream of positive data reaches the bureaus. This consistent activity shows that your business has ongoing operational needs and the cash flow to meet them. It transforms a thin credit file into a robust history that Tier 2 and Tier 3 lenders will respect. Think of each invoice as a vote of confidence in your company’s future.

Reporting Mechanics and Timelines

Understanding the timing of reporting is vital for managing your growth. Most vendors report in cycles, typically every 30 to 45 days. This means your purchase today might not appear on your credit report until next month. To maximize your score, aim for early payments. In the business world, paying 10 days before the due date can actually result in a higher score than paying on the exact due date. Accuracy also matters. Ensure your business name, address, and phone number are identical across all accounts. Even a small discrepancy in your address can cause bureaus to create a “split file,” which hides your hard-earned progress from potential creditors.

Business Credit Cards: The Pros, Cons, and PG Barrier

Revolving credit offers a different kind of freedom than term-based accounts. While net 30 vendors provide specific items for your operations, a business credit card allows you to handle miscellaneous expenses like travel, fuel, or emergency repairs. This “open-loop” flexibility is tempting for many founders. However, when evaluating net 30 accounts vs business credit cards for startups, you must look closely at how the debt is structured. Unlike a vendor invoice that you settle in full, a credit card allows you to carry a balance. This revolving nature can lead to a cycle of high interest if your cash flow isn’t managed with precision.

The most significant hurdle for a new LLC is the personal guarantee (PG). Most traditional banks require you to sign away your personal liability to secure a card. This means your personal credit score is directly tied to your business spending. If your company’s credit utilization climbs too high, your personal score will likely drop. This “trap” makes it difficult to maintain a healthy financial life outside of your work. While the SBA provides a wealth of information on SBA business funding options, many of those traditional paths still rely heavily on your personal creditworthiness during the startup phase.

Cost is another factor that often catches entrepreneurs off guard. As of June 2026, the average interest rate for new business credit card offers has reached 22.17%. Carrying a balance at these rates can quickly drain your profit margins. Even existing accounts face high costs, with average rates sitting at 21.52%. Some variable APRs can even spike as high as 28.49% depending on the market. These figures highlight why using net 30 accounts vs business credit cards for startups is often the more sustainable choice for early-stage growth. You avoid the high interest and the risk of personal financial damage while still building the history you need.

When to Graduate to Business Credit Cards

You shouldn’t rush into a business credit card application until your foundation is secure. The smartest strategy is to use net 30 tradelines to build a solid corporate credit file first. By establishing a high Paydex score through consistent vendor payments, you’ll eventually qualify for “No PG” corporate cards. These advanced financial tools are reserved for businesses that have proven their reliability through documented history. If you want to scale without the stress of personal liability, you can learn how to build business credit without a loan. This approach ensures your company stands on its own EIN before you ever risk your personal assets for a revolving line of credit.

Strategy Guide: Which Option Should Your Startup Choose?

Deciding between net 30 accounts vs business credit cards for startups depends on your current credit maturity. If you’re operating a new LLC with a thin credit file, you need a foundation that doesn’t jeopardize your personal assets. Starting with a business net 30 account is the safest path for early-stage growth. It allows you to build a reputation with bureaus while avoiding the high interest rates and personal liability associated with revolving cards. Use the table below to compare your options at a glance.

| Feature | Net 30 Accounts | Business Credit Cards |

|---|---|---|

| Approval Basis | EIN and Business Verification | Personal Credit and PG |

| Reporting Bureaus | Equifax, Creditsafe, FairFigure | Personal and Business Bureaus |

| Personal Risk | None (No Personal Guarantee) | High (Personal Liability) |

| Best Use Case | Branding and Office Essentials | Travel and Daily Flexibility |

For most founders, the goal is to reach a point where the business can secure its own funding. By prioritizing vendor tradelines first, you create a documented history of reliability. This history eventually makes you a prime candidate for high-limit corporate cards that don’t require a personal guarantee. It’s a structured ascent rather than a risky leap. You can begin this journey today by choosing to apply for a business net 30 account to secure your first Tier 1 tradeline.

The Step-by-Step Credit Building Checklist

Success in business credit isn’t about luck; it’s about following a repeatable system. Follow this checklist to ensure your payments actually move the needle on your score:

- Apply: Ensure your LLC or Corporation is properly registered with the Secretary of State and has a valid EIN.

- Order: Purchase necessary operational items, such as customizable products for team uniforms or client onboarding kits.

- Pay: Settle your invoices 1 to 10 days before the due date. Early payments are a major factor in achieving a high Paydex score.

- Track: Regularly monitor your reports on Creditsafe and FairFigure to ensure your tradelines are appearing correctly.

- Repeat: Maintain consistent monthly activity to keep your credit file active and healthy.

Common Mistakes to Avoid

Even seasoned entrepreneurs can stumble when building credit. Avoid these pitfalls to keep your progress on track:

- Using inconsistent business information (name, address, or phone) across different accounts.

- Paying exactly on the due date rather than early, which misses out on scoring bonuses.

- Ordering from vendors that don’t report to major business credit bureaus.

- Over-leveraging high-interest credit cards before the business has stable cash flow.

- Treating business credit accounts as personal spending tools.

- Failing to update your business address with the Secretary of State after a move.

- Ignoring your business credit reports for more than 90 days.

Leveraging The CEO Creative for Strategic Credit Growth

Lenders and creditors value professionalism. When a company presents itself with a cohesive identity, it signals stability and long-term vision. Utilizing Net 30 apparel for your team does more than just boost morale. It creates a professional image that matters during manual underwriting reviews for Tier 2 or Tier 3 credit. A professional logo on high-quality merchandise proves that your business is an active, operational entity. This aesthetic credibility, combined with a strong Paydex score, makes your startup a much more attractive candidate for future funding.

Maximizing Your Membership

The CEO Creative Membership is designed specifically to help founders navigate the early stages of business credit. It serves as a foundational Tier 1 tradeline that reports monthly, providing the consistent data bureaus need to calculate your score. You can select from a wide range of functional items that serve your daily operations. Consider these options to keep your spending consistent and professional:

- Branded mugs for the office or client gifts.

- High-quality engraved items to celebrate team milestones.

- Custom uniforms that ensure your staff looks cohesive.

- Onboarding kits to welcome new hires with professional flair.

If you’re looking to expand your vendor list further, you can check out the best Net 30 apparel vendors in 2026 to see how other companies integrate merchandise into their credit strategies. This holistic approach ensures you aren’t just spending money; you’re building a foundation.

Strategic growth requires a balance between operational needs and financial documentation. By choosing net 30 accounts vs business credit cards for startups, you protect your personal assets while building a professional brand. The synergy between high-quality merchandise and consistent bureau reporting ensures your company is ready for its next stage of funding. Your business credit file should be a reflection of your brand’s excellence and reliability.

Secure Your Brand’s Financial Future Today

Choosing the right path for your company’s financial growth doesn’t have to be a gamble. When you evaluate net 30 accounts vs business credit cards for startups, it’s clear that vendor tradelines provide the safest entry point for new LLCs. You’ve learned how to protect your personal credit score while building a professional brand identity through strategic purchases. By focusing on consistent payments and accurate reporting, you set the stage for Tier 2 and Tier 3 funding opportunities.

The CEO Creative offers a streamlined solution with no personal guarantee required and instant approval options available for new businesses. We ensure your positive payment history reaches Equifax, Creditsafe, and FairFigure to maximize your impact. Take the first step toward corporate independence and financial authority. Apply for a CEO Creative Business Net 30 Account Today to start building the credit your business deserves. Your brand’s potential is limitless when you have the right systems in place. We’re proud to be your partner and foundational support system as you scale.

Frequently Asked Questions

Do Net 30 accounts require a personal guarantee?

Most Net 30 accounts don’t require a personal guarantee. This is a significant advantage for new founders who want to protect their personal assets while growing their company. By using your EIN to secure terms, you establish a clear boundary between your personal and business financial lives. This structure ensures that your business liabilities remain with the entity rather than affecting your personal credit score or borrowing power.

Which credit bureaus does The CEO Creative report to?

The CEO Creative reports your payment activity to Equifax Business, Creditsafe, and FairFigure. Reporting to these specific bureaus helps you build a multi-dimensional credit profile that modern lenders value. Because we share your data with multiple agencies, you aren’t just building one score; you’re creating a comprehensive financial reputation. Consistent reporting across these platforms is vital for moving from Tier 1 to higher levels of corporate credit.

How long does it take for a Net 30 account to show up on my credit report?

You can typically expect your account to appear on your credit report within 30 to 45 days. This timeline depends on the vendor’s specific reporting cycle and when you settle your invoice. Most vendors report data once a month in batches. If you pay your invoice just after a reporting period ends, it might take a full cycle before the bureaus update your file with the new information.

Can I build business credit with an EIN only?

Yes, you can absolutely build a robust credit profile using only your EIN. By working with reporting vendors that don’t require a personal social security number, you document your company’s reliability independently. This process allows you to establish a Paydex score and qualify for larger lines of credit. It’s the most effective way to ensure your startup stands on its own financial feet without relying on your personal history.

Does paying a Net 30 invoice early help my credit score?

Paying early is one of the best ways to boost your business credit score. While on-time payments are expected, business scoring models like the Paydex system specifically reward early settlement. Settling your invoice 10 days before the due date can result in a higher score than paying on the actual deadline. This proactive approach signals to future lenders that your business manages its cash flow with extreme precision and care.

What is the difference between a Net 30 and a Net 60 account?

The primary difference is the length of time you have to settle your invoice. A Net 30 account requires full payment within 30 days of the purchase or invoice date. A Net 60 account extends that window to 60 days. While Net 60 terms offer more cash flow flexibility, Net 30 accounts are more common for startups. They provide more frequent reporting opportunities, which helps you build your credit profile much faster.

Is a business credit card better than a Net 30 account for a new LLC?

Net 30 accounts are usually the better starting point for a new LLC because they rarely require a personal guarantee. When comparing net 30 accounts vs business credit cards for startups, vendor accounts offer a lower barrier to entry and protect your personal credit score. Credit cards are useful for daily flexibility, but they often come with high interest rates and personal liability risks that can hinder a young company’s growth.

What happens if I miss a payment on a Net 30 account?

Missing a payment can lead to late fees and negative reporting to the credit bureaus. Just one late payment can significantly damage your business credit score and make it harder to qualify for Tier 2 or Tier 3 credit. Most vendors will also suspend your credit terms until the balance is settled. It’s crucial to communicate with your vendor immediately if you anticipate a cash flow issue to protect your reputation.

Do I need a high personal credit score to get a Net 30 account?

You don’t need a high personal credit score to qualify for most Net 30 accounts. Because many vendors focus on your business registration and EIN, they often skip the personal credit check entirely. This makes vendor tradelines an ideal tool for entrepreneurs who are still working on their personal finances. It allows you to build a successful business reputation regardless of your past personal credit challenges or high utilization.

Can I use Net 30 accounts to buy office supplies and apparel?

Yes, you can use Net 30 accounts to purchase essential office supplies, custom apparel, and branding materials. Buying these items through a reporting vendor allows you to meet your operational needs while simultaneously building credit. Whether you’re ordering team uniforms or onboarding kits for new hires, these routine business expenses become valuable tradelines. This strategy ensures that every dollar you spend on your brand also works to strengthen your financial future.