Title: How to Read a Dun & Bradstreet Report: Complete 2026 Guide

Key Takeaways

- Treat your Business Information Report (BIR) as a professional resume for your EIN to establish credibility with lenders and corporate partners.

- Master how to read a Dun & Bradstreet report by decoding complex metrics like the PAYDEX score and Failure Score to identify specific growth opportunities.

- Resolve the “Thin File” issue by identifying reporting gaps and avoiding common documentation mistakes that often lead to automatic credit denials.

- Implement a structured “Apply, Order, Pay, Track, Repeat” framework to build a robust credit profile using Tier 1 Net 30 vendors.

- Leverage strategic vendor tradelines from The CEO Creative to acquire essential business products while simultaneously strengthening your payment reporting history.

Understanding the Dun & Bradstreet Business Information Report

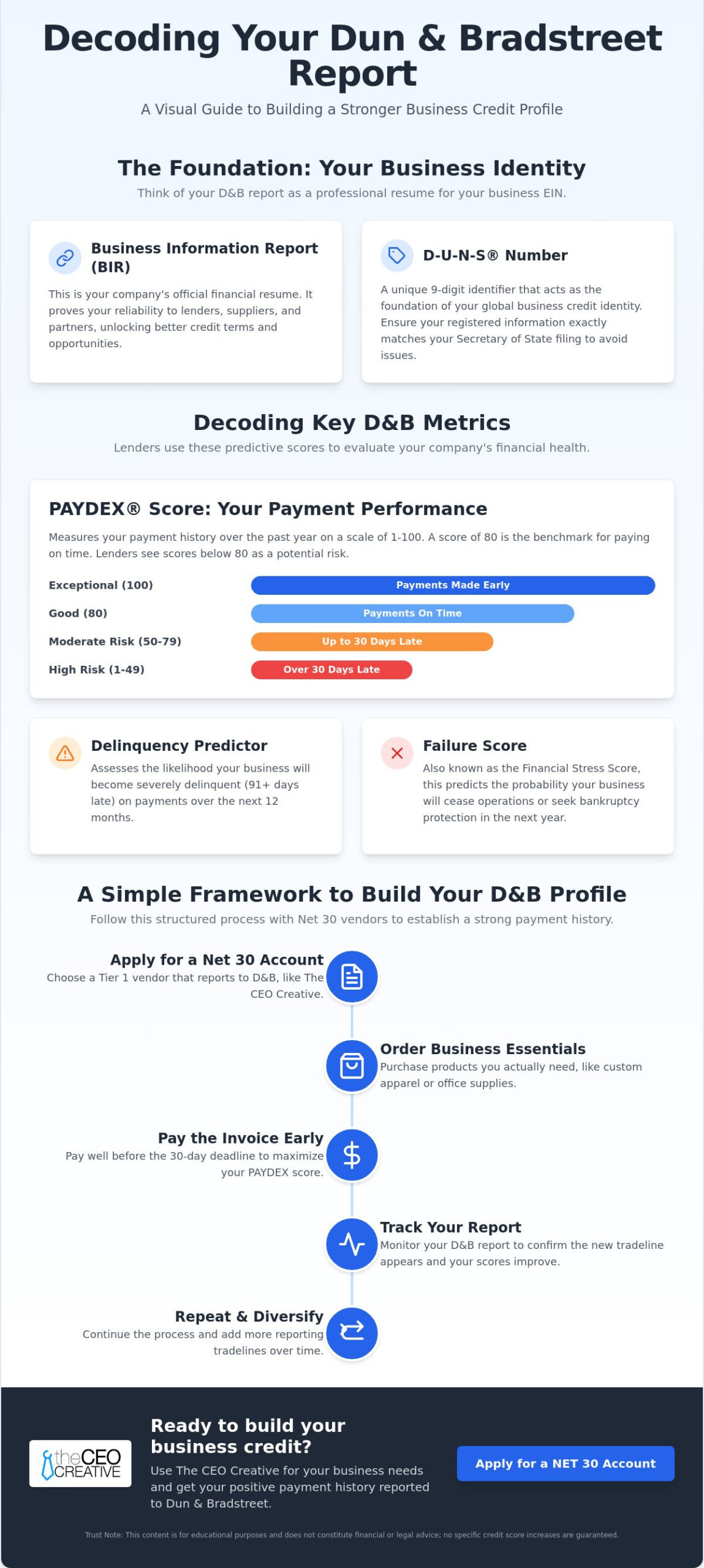

Think of the Business Information Report (BIR) as a professional resume for your business EIN. Just as a resume showcases your qualifications to an employer, the BIR proves your reliability to lenders and corporate partners. Learning how to read a Dun & Bradstreet report is the first step toward unlocking higher credit limits and better terms. By the end of this guide, you’ll know exactly how to interpret your scores and build a profile that lenders trust. Trust Note: This content is for educational purposes and does not constitute financial or legal advice; no specific credit score increases are guaranteed.

Establishing this profile requires consistent data, and that’s where strategic partnerships come in. The CEO Creative acts as a reporting NET 30 vendor, feeding positive payment data into your file to help establish your history. When you make a purchase and pay your invoice, that activity is reported, helping to fill the gaps in your credit story.

To better understand this concept, watch this helpful video:

The Role of the D-U-N-S Number

The foundation of your business credit identity is the Data Universal Numbering System, or D-U-N-S Number. This unique nine-digit identifier is issued by Dun & Bradstreet to track your company’s financial health globally. It’s a free identifier, and every new LLC should register for one before seeking net 30 accounts. It’s critical to ensure your business information matches your Secretary of State filing exactly. Even a minor typo in your legal name or address can delay your profile’s growth or cause confusion with lenders.

Business Identity and Background

The “Business Summary” section provides a snapshot of your ownership, physical location, and daily operations. Accuracy here is vital for your credibility. Using a residential address or a VOIP phone number can sometimes trigger a “high risk” flag. Lenders prefer to see established, commercial physical locations and verified landline numbers. Maintaining consistent business info across all platforms prevents the creation of “split files.” A split file occurs when data is fragmented across different versions of your business name, which can hide your positive credit history from potential creditors.

Key D&B Scores and Ratings: What the Numbers Actually Mean

Understanding how to read a Dun & Bradstreet report requires a deep dive into the predictive scores that lenders use to evaluate risk. In 2026, these scores are more than just historical records; they are real-time indicators of your company’s operational health. To have a score at all, you need vendor tradelines. A vendor tradeline is an account with a supplier that reports your payment history to credit bureaus. This process, known as payment reporting, allows vendors to share your data with major bureaus like Creditsafe, Equifax, and D&B. The CEO Creative acts as a strategic partner in this ecosystem. We report to multiple bureaus to ensure your positive activity gains maximum visibility among potential creditors.

The PAYDEX Score: Your Payment Performance

The PAYDEX score is the metric most business owners recognize first. It ranges from 1 to 100 and measures your payment performance over the past year. According to the Small Business Administration, business credit reports are essential for demonstrating that your firm is a reliable borrower. A score of 80 is the standard benchmark, indicating you pay your bills exactly on time. To reach a perfect 100, you must consistently pay your invoices significantly before the due date. Many startups struggle with a low score not because they pay late, but because they lack reported tradelines entirely. Without data, D&B cannot generate a high score. Conversely, even a single late payment to a Net 30 vendor can disproportionately damage this score, signaling to lenders that your cash flow might be unstable.

Delinquency and Failure Scores

Beyond PAYDEX, your report includes the Delinquency Predictor and the Failure Score. The Delinquency Predictor assesses the likelihood of your business slowing payments or becoming severely delinquent over the next 12 months. The Failure Score, often called the Financial Stress Score, predicts the probability of your LLC ceasing operations or seeking legal relief from creditors. These scores are particularly powerful because they use industry benchmarks. They don’t just look at your business in a vacuum; they compare your performance against similar businesses in your specific sector. This allows lenders to see if you are outperforming or lagging behind your peers.

If you’re ready to start providing the data D&B needs to generate these scores, you can begin by applying for a business net 30 account to establish your first reported tradeline.

Common Mistakes and Red Flags in D&B Reporting

Many entrepreneurs only learn how to read a Dun & Bradstreet report after their first loan denial. One of the most pervasive issues for new LLCs is the “Thin File” problem. This occurs when your business is legally registered, but you have no reported payment history. Without data, D&B can’t generate a score, leaving lenders to view your company as a high-risk unknown. It’s a frustrating hurdle, but it’s often caused by simple administrative oversights rather than poor financial management. Mistakes happen. They shouldn’t be permanent.

Beyond data volume, professional appearance plays a subtle but vital role in how creditors perceive your risk. Investing in logo design increases your perceived credibility, signaling that your company is an established entity rather than a temporary project. According to the SBA guide to business credit reports, maintaining accurate and consistent data is non-negotiable for anyone looking to secure external funding. Small errors in your profile can lead to automatic denials for higher-tier credit lines.

Top 5 Errors to Avoid on Your D&B Profile

- Inconsistent business naming: Using “LLC” on some documents while omitting it on others creates confusion and can lead to split files.

- Personal contact information: Lenders often flag profiles that use personal cell numbers or home addresses as “high risk.”

- Outdated company details: Failing to update your report after a change in location or revenue makes your business look stagnant.

- Insufficient tradelines: You can’t generate a score without enough reporting vendors. You typically need at least three active accounts to see a PAYDEX score.

- Paying exactly on the due date: While not “late,” paying on the deadline only earns you an 80 PAYDEX. You must pay early to reach a perfect 100.

Identifying and Disputing Inaccuracies

D&B provides the “iUpdate” tool, which allows you to correct basic company information and upload financial statements. If you spot a late payment report that you believe is an error, you should initiate a dispute immediately through their portal. Startups should monitor their reports at least once per quarter. Regular checks ensure that your growth is being accurately reflected and that no fraudulent activity is dragging down your scores. By staying proactive, you ensure your business credit resume stays as strong as your actual performance.

Step-by-Step: How to Build Your D&B Profile with Net 30 Vendors

Understanding how to read a Dun & Bradstreet report is the baseline; building that report into a powerful asset is your mission. Many new LLCs get stuck because they believe they need a high-limit business credit card immediately. However, those cards often require a personal guarantee or an established score that a startup simply doesn’t have yet. Tier 1 Net 30 vendors are the true foundation of a professional credit profile. They allow you to build credit using your EIN without the hurdles of traditional lending. To see a full list of reporting partners that can help you get started, consult our Net 30 Vendors 2026 Guide.

The 5-Step Credit Building Checklist

- 1. Apply: Open a business net 30 account with a reporting vendor like The CEO Creative. This is your first official entry into the bureau ecosystem.

- 2. Order: Purchase necessary office supplies or branding items to trigger an invoice. Small, professional purchases keep your overhead low while building a history of activity.

- 3. Pay: Settle the invoice within the 30-day window. If you want a significant PAYDEX boost, aim to pay within 10 days of the invoice date. Early payments signal high liquidity to creditors.

- 4. Track: Monitor your D&B report. It’s rewarding to see that first “tradeline” appear in your history, proving that your business is now a recognized entity in the financial world.

- 5. Repeat: Maintain consistent monthly spending. Lenders want to see stability, not just a one-time transaction. Regular activity proves your business is operational and reliable.

Why Reporting Consistency Matters

One-off purchases don’t build strong scores. Lenders typically look for 3 to 5 consistent tradelines to verify your company’s creditworthiness. Most vendors follow a monthly reporting schedule, which means your score won’t jump overnight. It reflects a pattern of behavior over time. Lenders view credit building as a marathon; if you only buy once, the data point is an outlier. When you repeat the process monthly, you create a trend line that creditors analyze when they see your profile. By shifting your routine spending to reporting vendors for items like customizable products, you build credit without adding new expenses to your budget. Consistency turns a thin file into a robust credit profile that commands respect from banks.

Ready to take the first step toward a stronger profile? Apply for a net 30 account today and start building your business foundation.

Leveraging The CEO Creative to Strengthen Your D&B Report

The CEO Creative is your strategic partner in the journey to corporate creditworthiness. While knowing how to read a Dun & Bradstreet report allows you to identify gaps, our platform gives you the tools to fill them. We provide a dual benefit for growing organizations: access to high-quality net 30 apparel and the creation of a powerful tradeline. Our membership program is designed specifically for structured credit growth, helping you maintain the consistent reporting history that lenders demand.

From Branding to Tradelines

Every purchase you make should serve a larger purpose. When you order custom mugs, stationery, or promotional items, you fulfill an immediate operational need while simultaneously building your financial resume. One of the most significant advantages we offer is an EIN-only approval process. This means you can establish your business credit profile without a personal credit check or a personal guarantee. Professional branding items like uniforms and onboarding kits signal to D&B analysts that your company is a legitimate, established entity. These visual markers of a “real” business often carry weight when your file is being reviewed for higher-tier credit opportunities. Mastering how to read a Dun & Bradstreet report helps you see exactly when these branding efforts begin to influence your scores.

What Happens Next?

Building your profile is a straightforward process when you follow a structured system. Here is the path to strengthening your report:

- Apply for your account: Complete the application to get instant approval using only your EIN.

- Place your first order: Choose from office essentials, custom gear, or apparel to trigger your first invoice.

- Watch your report: Monitor your file as your new tradeline begins reporting to Creditsafe, Equifax, and FairFigure.

Business credit is a marathon, not a sprint. Your D&B report is the scorecard that tracks your progress over time. By using The CEO Creative to handle your routine branding and operational needs, you ensure your scorecard remains strong. Success comes from consistent, deliberate actions that prove your reliability to the financial world. We are here to support your long-term vision with the systems you need to thrive.

Master Your Business Credit Future

Mastering the technical details of your credit profile is a strategic move for any serious entrepreneur. You’ve learned that your scores are not static; they are dynamic reflections of your payment habits and operational consistency. Knowing how to read a Dun & Bradstreet report gives you the clarity to spot errors and the insight to identify where your profile needs more data. Building a robust file doesn’t have to be intimidating when you have the right partners in your corner. Each reported tradeline is a building block for your company’s future financial opportunities.

The CEO Creative provides a seamless path for new LLCs to establish their first vendor tradelines. We offer instant approval with your EIN and require no personal guarantee, allowing you to build credit independently of your personal finances. Your activity with us reports to Equifax, Creditsafe, and FairFigure to ensure maximum visibility across the bureaus. Apply for a CEO Creative Net 30 Account and Start Building Credit Today to take control of your company’s financial narrative. By combining high-quality branding with consistent payment reporting, you set the stage for long-term growth and sustainability. Your journey toward a perfect PAYDEX score starts with a single, deliberate step.

Frequently Asked Questions

Do I need a personal guarantee to get a D&B report?

No, you do not need a personal guarantee to establish or view a Dun & Bradstreet report. D&B tracks your company’s creditworthiness using your Employer Identification Number (EIN) rather than your personal social security number. This structure allows you to build a corporate financial identity that is entirely separate from your personal assets, which is a major advantage for growing startups.

How long does it take for a Net 30 vendor to show up on my D&B report?

Most reporting Net 30 vendors update their records on a monthly cycle. You should generally expect to see a new tradeline appear on your report within 30 to 90 days of your first payment. The exact timing depends on the vendor’s specific reporting schedule and how quickly D&B processes the incoming data files into your business profile.

Can I build a D&B score without any employees?

You can absolutely build a high D&B score as a solo entrepreneur or a company with zero employees. D&B scores are calculated based on your payment history and financial behavior, not the size of your workforce. For those scaling up and hiring internationally, ICSPayroll provides specialized support for managing staff in the Netherlands. As long as you have a registered legal entity and active vendor accounts, you can generate a professional score that attracts lenders.

What is a good PAYDEX score for a new business in 2026?

A PAYDEX score of 80 is the standard benchmark for a healthy business because it indicates you pay all invoices exactly on time. In 2026, lenders look for this score as a baseline for reliability. Learning how to read a Dun & Bradstreet report helps you monitor this number so you can aim for scores above 80, which require paying invoices early.

Does paying a Net 30 invoice early actually help my D&B report?

Paying early is the most effective way to maximize your PAYDEX score. While paying on the due date earns you an 80, paying 10 to 20 days early can push your score toward a perfect 100. These early payments signal high liquidity and excellent cash flow management, making your business much more attractive to banks and high-tier creditors.

Why is my D&B report empty even though I have a DUNS number?

A DUNS number is simply a digital identifier; it does not automatically pull in credit data. Your report will remain empty until you establish accounts with vendors that participate in payment reporting. To see data in your file, you must actively use your Net 30 terms and ensure those vendors report your on-time payments to the bureau.

Does D&B report to the personal credit bureaus like Experian?

Dun & Bradstreet is a commercial credit bureau and does not report business activity to personal bureaus like Experian, Equifax, or TransUnion. This separation protects your personal credit score from being affected by your business expenses. However, keep in mind that some lenders may still require a personal credit check during the initial application for high-limit financing.

Can I fix a low business credit score by closing accounts?

Closing accounts is rarely a good strategy for fixing a low business credit score. It can shorten your credit history and reduce the number of active tradelines on your report, which may actually cause your score to drop. A better approach is to maintain your accounts and focus on consistent, early payments to demonstrate long-term financial stability.

Ready to strengthen your business credit profile with a partner that understands your growth needs? The CEO Creative offers instant approval for new LLCs with no personal guarantee required. Our accounts report to Equifax, Creditsafe, and FairFigure to ensure your hard work is reflected across the bureaus.

Apply for a CEO Creative Net 30 Account and Start Building Credit Today

What happens next:

- Submit your application with your EIN for instant approval.

- Place your first order for professional office essentials or custom gear.

- Pay your invoice early to trigger positive payment reporting to the bureaus.

Building a robust business credit profile is a strategic process that requires the right tools and consistent behavior. By purchasing routine operational items like professional apparel, customized mugs, or engraved items, you can fulfill your branding needs while establishing a solid financial foundation. Start your credit building journey today and turn your business report into a powerful asset for future funding.