Blog Title: Bootstrap Your Business with Vendor Credit | The CEO Creative

Key Takeaways

- Learn how bootstrapping your business with vendor credit allows you to acquire essential supplies today while keeping your cash in the bank for thirty days.

- Understand the mechanics of vendor tradelines and how reporting to bureaus like Equifax and Creditsafe builds a professional paper trail for your EIN.

- Bridge the “Cash Gap” by using Net 30 accounts to fund operations before sales revenue arrives, ensuring your daily cash flow remains stable.

- Follow a structured monthly framework of applying, ordering, and paying to transform routine business expenses into a powerful credit-building tool.

- Discover how a CEO Creative Membership simplifies the growth process by providing high-quality branding tools that report directly to major business bureaus.

What is Bootstrapping with Vendor Credit?

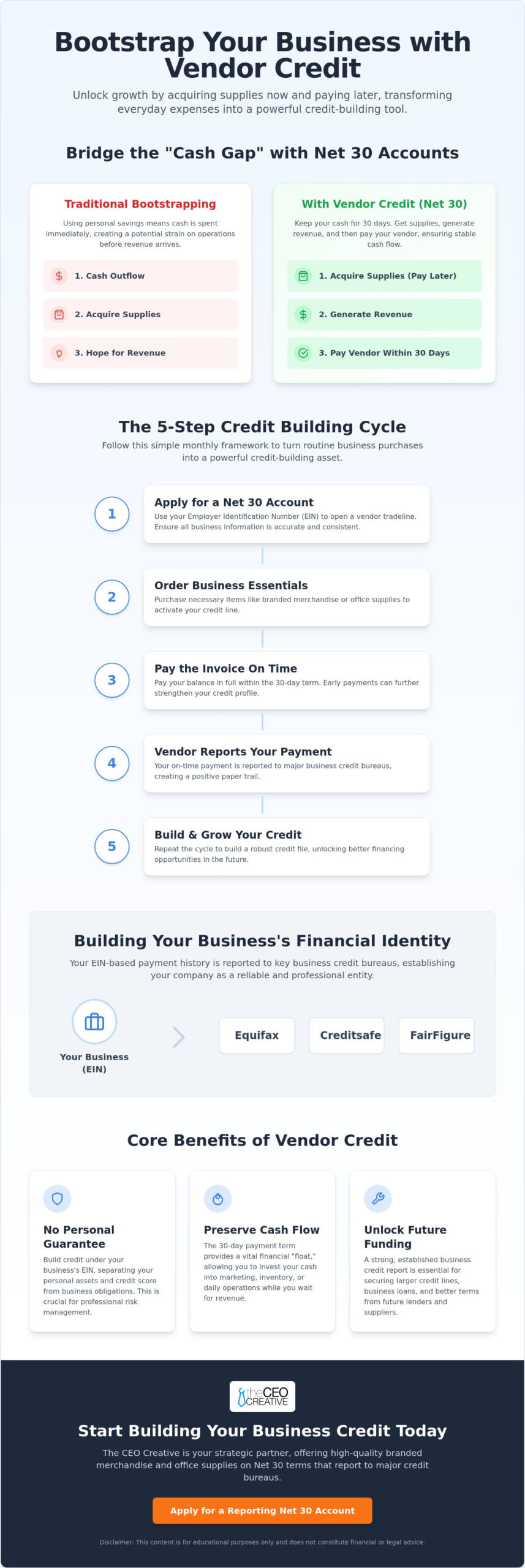

Bootstrapping is the art of building a company from the ground up using personal savings and revenue. It demands high discipline and a keen eye for cash flow. Most entrepreneurs view this as a solo journey; however, strategic founders use Vendor Finance to accelerate their progress. Bootstrapping your business with vendor credit provides a financial “float” that lets you acquire essential supplies today and pay for them later. This approach keeps your personal cash in the bank while your business operations move forward.

Using these terms effectively means you aren’t just saving money. You’re leveraging other people’s capital to establish your brand identity. It’s a foundational move for any new LLC or ecommerce startup. Trust and Compliance Note: This content is for educational purposes and is not financial or legal advice.

To better understand how these strategies help you scale, watch this helpful video:

Defining The CEO Creative as a Reporting Vendor

The CEO Creative acts as a strategic partner for bootstrapped startups by offering a business net 30 account. Many vendors sell products but don’t report your payment history to credit bureaus. These are “dead end” accounts for a growing business. A reporting vendor like The CEO Creative ensures that every time you buy office supplies or branded merchandise, that activity is shared with credit agencies. This visibility is what separates a hobby from a professional entity. Tier 1 vendors are usually the easiest to access for new businesses because they don’t require a long credit history or a personal guarantee.

Key Terms: Net 30, Tradelines, and Bureau Reporting

Understanding the vocabulary of credit is essential for success. A Net 30 term means you have exactly 30 days from the invoice date to pay your balance in full. When you open an account, you create a vendor tradeline. This is a specific record of your credit relationship tied directly to your Employer Identification Number (EIN). Payment reporting is the process where the vendor sends your data to bureaus like Equifax, Creditsafe, and FairFigure. This creates a visible credit file. Without this paper trail, your business remains invisible to traditional banks. Bootstrapping your business with vendor credit turns your routine operational expenses into proof of financial reliability.

The Mechanics of Vendor Tradelines and Payment Reporting

Bootstrapping your business with vendor credit creates a visible history of financial responsibility. When you pay an invoice on Net 30 terms, you’re doing more than settling a bill. You’re adding a “tradeline” to your business credit report. This record acts as a paper trail for future lenders, showing them you can handle debt responsibly without needing a personal guarantee. Every reported transaction strengthens your reputation in the eyes of the financial community.

Your Employer Identification Number (EIN) serves as the anchor for this data. Bureaus like Equifax and Creditsafe collect information from your vendors to build your profile. It’s vital that your business name, address, and phone number are identical across all accounts. Mismatched data is a common reason why tradelines fail to appear on reports. If your vendor has one address and your Secretary of State filing has another, the system might not recognize your business. Consistency is the secret to ensuring your hard work is actually recorded.

Payment timing also matters. While staying on time is the bare minimum, paying early can often boost your internal scores with specific bureaus. As noted in the SBA guide to vendor credit, these early accounts are essential for conserving cash while proving you’re a safe bet for larger credit lines. You can begin establishing this foundation right now by applying for a business net 30 account that reports your activity regularly.

The Reporting Schedule: Equifax, Creditsafe, and FairFigure

Vendors typically report data on a monthly or quarterly cycle. Once you pay your invoice, the vendor sends a batch file to the bureaus. Monitoring this progress is easier with tools like FairFigure, which provides a consolidated view of your standing. Founders should prioritize vendors that report to multiple agencies to ensure their credit file grows across the entire financial ecosystem. This broad reporting helps you build a more comprehensive and reliable corporate identity.

Building Credit Without a Personal Guarantee

One of the biggest hurdles for new founders is the fear of personal liability. By focusing on EIN-based credit, you separate your personal assets from your business obligations. This separation is the core of professional risk management. It protects your personal credit score from business fluctuations. Successfully managing Tier 1 vendor accounts sets the stage for Tier 2 and Tier 3 lines, which offer higher limits and more flexible terms for scaling your operations.

Cash Flow Management: Why Vendor Credit Beats Traditional Bootstrapping

Cash flow is the lifeblood of any organization. While we’ve discussed the mechanics of reporting, the real power of bootstrapping your business with vendor credit lies in your bank account balance. Most founders face the “Cash Gap” where they must pay for operational tools weeks before seeing a return on their investment. Traditional bootstrapping forces you to drain your reserves immediately. By using vendor credit, you effectively extend your runway. You’re using the vendor’s capital to fund your daily needs while your own cash remains available for emergency pivots or marketing surges.

This strategy turns routine expenses into interest-free short-term loans. Instead of a lump-sum payment today, you keep that liquidity for 30 days. It’s a level of agility that cash-only businesses simply don’t have. Whether you’re an ecommerce brand or a service agency, maintaining this “float” is what allows you to survive the lean months and scale during the busy ones. It’s a foundational system for long-term sustainability.

Product-Focused Credit Building

The key is to spend on items that add value to your brand while establishing your file. You can order high-quality mugs for client gifts or apparel for your team on Net 30 terms. These aren’t just perks; they’re branding tools that build your corporate identity. Even engraved merchandise for executive gifts can be acquired through your vendor account. This ensures that every dollar you spend helps professionalize your brand while the payment activity builds your credit score. You’re effectively multitasking with your operational budget.

For those in the sustainable fashion industry, we recommend you visit thrifted apart to see how they leverage authentic Y2K curation to build a strong brand identity.

Avoiding the “No Credit File” Trap

Many founders think staying out of debt is the safest path. However, a “no credit” status is a major liability for an LLC. If you only use cash, you remain invisible to the financial ecosystem we explored in the previous sections. Lenders can’t verify your reliability if there’s no data. Don’t let your business stay in the shadows. It’s crucial to understand how to build business credit without a loan to ensure your company is ready for future expansion. Bootstrapping your business with vendor credit ensures that your growth is documented and verifiable from day one.

Step-by-Step Checklist: Implementing a Vendor Credit Strategy

Transitioning from financial theory to daily practice requires a disciplined routine. Bootstrapping your business with vendor credit isn’t a one-time event; it’s a monthly cycle that builds a reputation of reliability. By following a structured framework, you ensure every dollar spent on operations also works to secure your company’s financial future. This process shifts your focus from “hype” purchases to consistent, professional spending that lenders actually value.

The 5-Step Bootstrap Credit Loop

Success in business credit comes from repetition. Follow these five steps every month to ensure your data reaches the bureaus correctly:

- 1. Apply: Set up your EIN-based Net 30 account. Ensure all your business details match your official formation documents.

- 2. Order: Purchase essential branding or office gear. The CEO Creative acts as a reporting NET 30 vendor that helps build business credit through real business purchases, such as custom merchandise.

- 3. Pay: Settle the invoice on or before the 30-day mark. Early payments are often viewed favorably by internal scoring models.

- 4. Track: Verify that the payment is reported to the bureaus. Use monitoring tools like FairFigure to watch your profile grow.

- 5. Repeat: Maintain regular activity. A single tradeline is a start, but a history of multiple on-time payments creates a robust profile.

Ready to start your first loop? You can apply for a business net 30 account and begin building your corporate foundation today.

8 Common Mistakes in Vendor Credit Bootstrapping

Mistakes can derail your progress and keep your business invisible to lenders. Avoid these common pitfalls to keep your credit-building strategy on track:

- Using inconsistent business addresses or phone numbers across different accounts.

- Missing the payment deadline. Even being late by one day can negatively impact your reporting.

- Over-extending the business beyond its ability to pay within the 30-day window.

- Assuming all vendors report to all bureaus automatically. Always verify reporting status before buying.

- Failing to monitor credit files for reporting errors or missing tradelines.

- Closing accounts too early. A longer credit history generally results in a stronger score.

- Buying unnecessary items just for the sake of credit. Stick to items your business actually needs.

- Neglecting the importance of professional branding. Lenders often look for a cohesive brand identity as a sign of a stable business.

The CEO Creative: Your Strategic Partner in Bootstrapping Success

The journey of a founder often starts with a vision and a limited budget. Bootstrapping your business with vendor credit is the smartest way to scale in 2026 because it aligns your operational needs with your financial growth. The CEO Creative Membership simplifies this path by providing access to high-quality branding tools while building your corporate credit profile. You’re no longer just buying supplies; you’re investing in a system that reports your reliability to major bureaus. This structure allows you to focus on your core business while the credit-building process runs in the background.

Lenders look for signs of stability and professionalism when reviewing applications. A cohesive brand identity, starting with a professional logo design, signals that your business is a serious entity. It moves you away from the “startup” label toward being a corporate partner. By using vendor terms to acquire these services, you preserve your cash for other growth initiatives while simultaneously checking the boxes that future creditors require. It’s a dual-purpose strategy that maximizes the value of every dollar spent.

Establishing Your Corporate Identity

A professional appearance does more than just impress customers. It builds internal culture and external trust. When you use branded apparel and stationery, you create a physical presence for your LLC that banks recognize. Exploring the Best Net 30 Apparel Vendors to Build Business Credit is a great way to start this process. These items aren’t just perks; they’re strategic assets that help you qualify for higher credit tiers down the road. A well-branded business often finds it easier to secure larger contracts and better financing terms because they appear established and reliable.

Recap and Next Steps

Bootstrapping your business with vendor credit extends your cash flow, builds a robust EIN credit profile, and professionalizes your brand. It’s time to transition from a cash-only bootstrap model to a credit-leveraged model that protects your personal assets. Success in the modern market comes from structured systems and reliable reporting partners. Your next move is to apply, order, and pay consistently to turn your daily expenses into a powerful financial foundation. Start by choosing products that reflect the high standards of your organization and watch your corporate profile grow alongside your revenue.

Transform Your Bootstrapping Strategy Today

Bootstrapping your business with vendor credit is the most effective way to separate your personal finances from your corporate growth. By now, you understand that building credit isn’t about taking on unnecessary debt; it’s about creating a documented history of reliability. This strategy allows you to professionalize your brand with custom merchandise while ensuring your EIN is visible to major credit bureaus. You’ve moved beyond simple survival and are now building a sustainable foundation for future scaling.

The CEO Creative is here to serve as your foundational support system. We provide the tools you need to establish a professional presence and the reporting tradelines required to build a robust credit profile. It’s time to stop using personal funds for every operational need and start leveraging the power of Net 30 terms. Your business deserves a credit profile as ambitious as your vision.

Apply for a Net 30 Account with The CEO Creative Today

What happens next?

- Instant Review: Most new LLCs and startups receive an immediate approval decision upon submitting their application.

- Account Activation: Once approved, you’ll gain instant access to our catalog of office supplies, apparel, and branding tools.

- Automated Reporting: Your payment activity is automatically shared with Equifax, Creditsafe, and FairFigure during the next reporting cycle.

By implementing these vendor credit strategies, you’re ensuring your business is ready for whatever opportunities come next, from expanding your operations to hiring new staff through SavannahJobs.com. Keep your cash flow flexible and your credit profile growing.

Trust and Compliance Note: The information provided in this article is for educational purposes only and does not constitute financial or legal advice.

Frequently Asked Questions

Do Net 30 vendors require a personal guarantee?

Most Tier 1 Net 30 vendors don’t require a personal guarantee. This allows founders to protect their personal credit and assets while establishing a corporate history. By focusing on your EIN, you build a separate identity for your business. The CEO Creative offers accounts that don’t require a personal check; making it an ideal choice for new LLCs starting from scratch.

How long does it take for vendor credit to show on my business credit report?

You’ll typically see a new tradeline appear on your report within 30 to 90 days. This timeline depends on the vendor’s specific reporting schedule and the processing speed of the bureaus. Most vendors report in monthly batches. It’s important to keep your account active and pay invoices on time to ensure the data flows correctly to Equifax or Creditsafe.

Can I build business credit if my personal credit is low?

Yes, you can build business credit even with a low personal credit score. Bootstrapping your business with vendor credit is specifically designed to bypass personal financial history. Vendors look at your business revenue and cash flow consistency rather than your individual FICO score. This separation is why many entrepreneurs use Tier 1 accounts to establish their first corporate credit file.

What happens if I pay my Net 30 invoice early?

Paying your Net 30 invoice early is a strategic move that demonstrates high reliability to creditors. Some bureaus reward early payments with higher internal scores. While paying on the due date is sufficient, settling your balance ahead of time creates a stronger profile. This habit proves you have excellent cash flow management and helps you qualify for higher credit limits faster.

Which credit bureaus does The CEO Creative report to?

The CEO Creative reports your payment history to Equifax, Creditsafe, and FairFigure. This broad reporting ensures your activity is visible across multiple major financial databases. By reporting to several bureaus, we help you build a comprehensive corporate profile. This visibility is essential when you’re bootstrapping your business with vendor credit and want to move toward larger credit lines or bank financing.

Is a membership required to start building credit with vendor accounts?

While not all vendors require a membership, The CEO Creative Membership provides a structured way to build credit while accessing branding tools. Membership models often include monthly reporting that keeps your tradelines active even when you aren’t making large purchases. This consistency is vital for maintaining a healthy credit score. It ensures your business stays visible to the bureaus throughout the year.

What kind of products can I buy with a Net 30 account?

You can purchase a wide range of essential business items, including custom office supplies, branded apparel, and professional design services. The CEO Creative provides real business products that help you professionalize your brand identity. Buying items you already need turns routine operational expenses into credit-building opportunities. This allows you to grow your brand and your credit profile simultaneously.

How many Net 30 accounts do I need to see a score increase?

Most industry professionals suggest having at least three to five active Net 30 accounts to establish a solid credit profile. A single tradeline is a great start, but bureaus look for a pattern of reliability across multiple sources. Diversifying your vendors shows that different companies trust your business with credit. This variety builds a more robust score and makes your company more attractive to future lenders.