What if your personal credit score didn’t have to carry the weight of your entire company’s growth? It’s exhausting to watch your personal debt-to-income ratio climb every time you need to stock up on inventory or buy new office supplies. You likely already know that separating your personal and business liabilities is the ultimate goal for any serious LLC or startup. However, your partner might be skeptical about membership fees or confused about how reporting actually works.

This guide will help you master the art of explaining the value of tradelines to a business partner so you can stop relying on personal guarantees and start building a powerful, independent corporate credit profile. We’ll break down the mechanics of Net 30 vendor reporting, address common skepticism about costs, and provide a clear roadmap for securing buy-in using an EIN-based credit strategy that protects your personal assets. By the end of this article, you’ll have the exact talking points needed to turn a skeptical partner into a strategic ally in your credit-building journey.

Key Takeaways

- Learn how to shift the narrative from membership fees to strategic assets. This helps your company move away from risky personal guarantees.

- Understand the mechanics of Net 30 accounts. These accounts serve as both a cash flow tool and a credit-building engine for your LLC.

- Gain confidence in explaining the value of tradelines to a business partner. Focus on protecting personal assets and creating an independent EIN profile.

- Identify key reporting bureaus like Equifax and Creditsafe. This ensures your monthly spending translates into a high-visibility credit resume.

- Follow a structured framework to build corporate credibility. Use essential business expenditures to establish your brand’s financial reputation.

The Strategic Necessity: Why Your Partner Needs to Understand Tradelines

Trust Note: This content is for educational purposes only and does not constitute financial, legal, or tax advice. We make no guarantees regarding specific credit score increases or financing approvals.

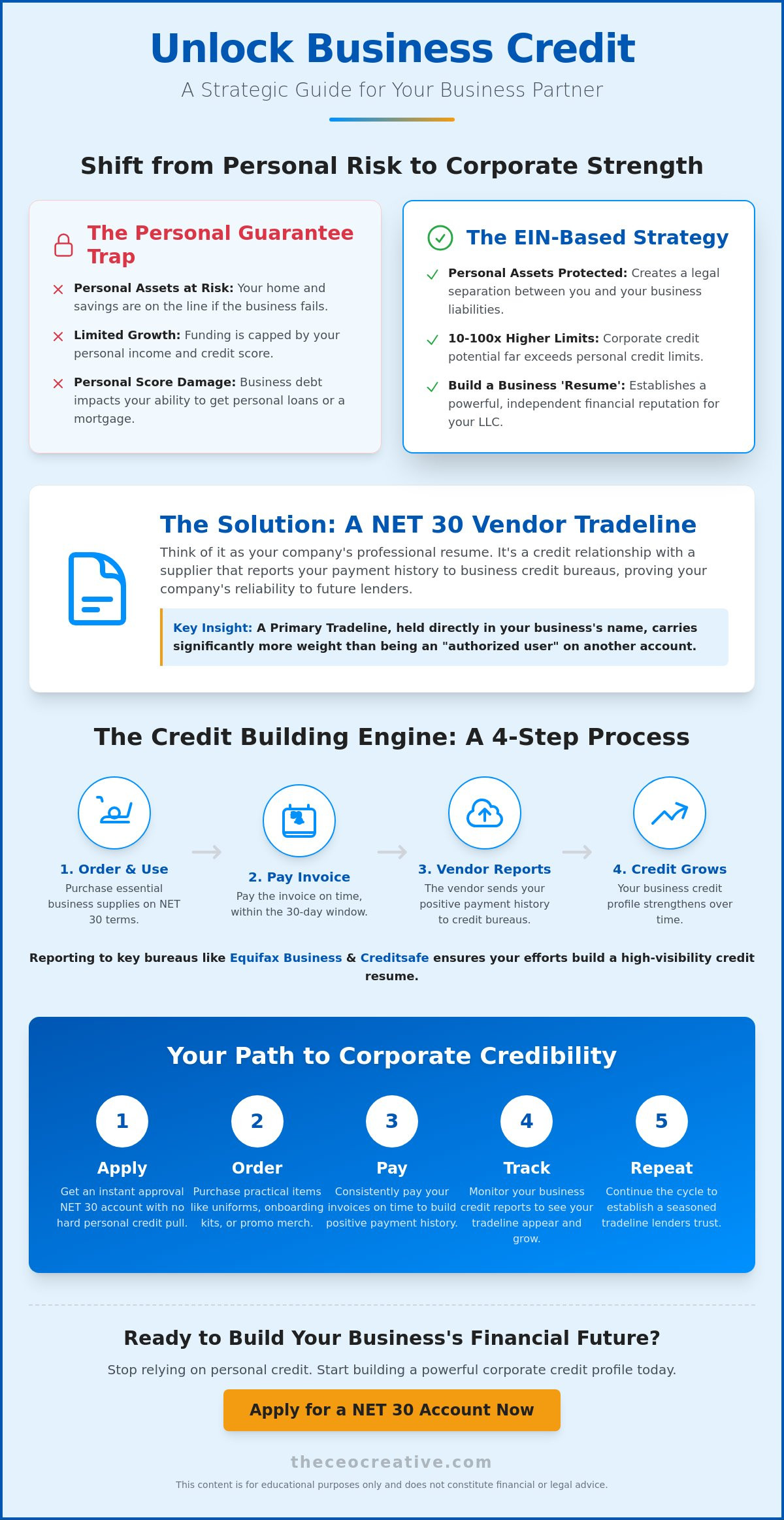

Building a company with a partner is an exercise in shared risk. However, many entrepreneurs unknowingly trap themselves in a cycle where their personal assets are permanently tethered to the business’s survival. Learning how to identify and explain the “Personal Guarantee Trap” is the first step toward financial freedom. By introducing a reporting vendor like The CEO Creative into your workflow, you can begin the process of establishing an independent credit profile that stands on its own merit. When you’re explaining the value of tradelines to a business partner, focus on how this strategy shifts the burden of proof from your personal bank account to the company’s EIN.

To better understand this concept, watch this helpful video:

The Personal Guarantee Trap

Using personal credit cards for business expenses creates a “liability bridge” that puts both partners at risk. If the business faces a downturn, your personal credit score takes the hit, making it harder to buy a home or secure a personal loan. Personal credit also has strict limits based on your individual income. In contrast, corporate credit potential is often ten to one hundred times higher than personal limits. Your ultimate goal is a “No Personal Guarantee” (No PG) future. Achieving this requires a business net 30 account that reports your payment history. This separation protects your family’s future while giving the business room to breathe and grow without individual constraints.

Tradelines as a Business Resume

Think of tradelines as the professional resume for your LLC. Just as a hiring manager looks for a solid work history, lenders look for a history of on-time payments with vendors. In 2026, a “thin file” or a lack of credit history remains the top reason for small business loan rejections. Lenders don’t just want to see that you have money; they want to see a seasoned tradeline that proves you’ve managed credit responsibly over several months or years. Starting early is critical. By explaining the value of tradelines to a business partner as a long-term asset, you can show them that every invoice paid today is an investment in the company’s future borrowing power. It’s about building a reputation before you actually need to use it.

Defining the Value: Tradelines and NET 30 Mechanics

A vendor tradeline is a credit relationship between your business and a supplier where your payment history is reported to major business credit bureaus. This is the bedrock of your company’s financial reputation. When you’re explaining the value of tradelines to a business partner, clarify the difference between a Primary Tradeline and an authorized user. A Primary Tradeline is an account held directly in your business’s name. It carries far more weight with lenders than simply being an authorized user on someone else’s account. This distinction is crucial because primary accounts demonstrate your LLC’s direct ability to handle debt and manage its own obligations.

Starting with the right partners is essential for long-term success. Instant approval vendors like The CEO Creative provide the perfect entry point because they remove the friction of high-barrier applications. This allows you to begin building history immediately without the stress of a hard credit pull on your personal file. It’s a low-risk, high-reward strategy that appeals to partners who might be cautious about taking on new financial commitments.

How NET 30 Accounts Manage Cash Flow

Net 30 terms act as a strategic “Buy Now, Pay Later” tool for your daily operations. This 30-day payment window allows your business to acquire necessary supplies or services and put them to work before the bill is due. For example, if you purchase custom uniforms or office essentials, you have an entire month to use those items to facilitate business growth before the cash leaves your account. You can essentially generate revenue from your purchases to pay off the invoice later. It’s a powerful way to keep cash in your bank account longer. To help your partner understand the full scope of these terms, you might share more on the Net 30 meaning and how it impacts your monthly bottom line.

The Power of Vendor Tradelines

A frequent error among new entrepreneurs is thinking they need a $50,000 bank loan to start building credit. That’s simply not true. Smaller, consistent vendor tradelines build the necessary depth that lenders look for during the underwriting process. These accounts are much easier to obtain than traditional loans, especially for startups or ecommerce brands. Consistent reporting of small invoices proves your reliability to the bureaus. If you’re ready to start, you can apply for a business net 30 account to begin documenting your payment history today. This approach creates a solid foundation to establish business credit without the hurdles of traditional banking. By focusing on practical, recurring spend, you demonstrate that your business is a stable and trustworthy entity.

The Mechanics of Growth: How Reporting to Equifax, Creditsafe, and FairFigure Works

Every purchase your business makes with a reporting vendor is more than just a transaction. It’s a data point that builds your company’s financial reputation. Explaining the value of tradelines to a business partner requires a clear breakdown of where that data goes and how it influences your future borrowing power. When you pay an invoice, that activity travels through a digital pipeline to reach specific bureaus that specialize in commercial data. This process transforms routine operational spending into a verifiable track record that lenders use to assess your risk level.

Tracking your progress is essential for maintaining partner buy-in. When they see the score moving, the strategy becomes tangible. Monitoring these updates allows you to verify that your efforts are yielding results. Reporting typically happens every 30 to 60 days. This cycle means your consistency today creates the “Score” your partner will see next month.

The Big Three of Vendor Reporting

In 2026, three specific entities dominate the landscape for small business credit evaluation. Equifax Business remains a heavyweight in lending decisions, often serving as the primary source for traditional banks and credit card issuers. Creditsafe has become a vital indicator for both global and domestic vendors. They use this data to determine what kind of terms and credit limits they should offer your LLC. Finally, FairFigure provides a modern platform for monitoring this multi-bureau data. It offers a centralized way to see how your payment history is being interpreted across the board. Using a business net 30 account that feeds these specific bureaus ensures your efforts aren’t wasted on invisible activity.

Consistency is Credibility

Your business information must be identical across every account you open. This includes your legal name, physical address, and phone number. A mismatched suite number or a different phone format can cause a tradeline to “ghost,” which means the bureau cannot match the data to your file. Your EIN acts as the anchor for your credit profile, but the bureaus use your contact details to verify the match. Following the SBA guide to establishing business credit highlights the importance of this professional foundation. Without consistency, even the most diligent payment history might fail to show up on your report. Make sure your partner understands that “administrative hygiene” is just as important as the payments themselves.

Implementation Strategy: Building Credit Through Essential Business Spend

Partners often view tradeline fees or membership costs as an extra expense. You need to flip that narrative. Explaining the value of tradelines to a business partner is much easier when you focus on “Practical Spend.” Instead of buying random retail items from vendors that don’t report, use your Net 30 accounts for things the company already needs. This makes the credit-building process feel like a natural part of operations rather than an added financial burden. It’s about making your existing budget work twice as hard for you.

A highly effective strategy is the “Onboarding Kit.” When you hire a new team member or launch a new project, you inevitably need uniforms and office gear. By purchasing customizable products through a reporting vendor, you fulfill a legitimate business need while simultaneously building your credit history. This approach ensures that every dollar spent is an investment in both your operations and your company’s future borrowing power. It’s intentional, professional, and easy for a partner to support.

Branding and Credit: A Dual Investment

Investing in your brand’s image is never a waste of capital. Using custom apparel helps build a professional identity for your team while your payments are reported to bureaus like Creditsafe and Equifax. Similarly, purchasing office supplies through these channels ensures your daily administrative needs contribute to your EIN’s reputation. Even a professional logo design can serve as a tradeline, signaling to future lenders that you are a serious, established entity. This dual-purpose spending is the cornerstone of a smart credit-building strategy.

Common Mistakes to Avoid (Partner Edition)

To maintain partner buy-in, you must avoid specific pitfalls that can jeopardize your progress. Skepticism often grows when systems break down, so keeping your credit-building activities organized is vital for long-term success. Avoid these common errors:

- Overspending just for the sake of credit. Keep your purchases professional and necessary to stay within budget.

- Late payments. This is the fastest way to destroy partner trust and your business credit scores.

- Failing to track the reporting schedule. You need to know when your data hits the bureaus to verify progress.

- Neglecting to update business info after a move. Consistency is key for reporting accuracy.

- Using personal funds to pay business vendor invoices. Always use your business bank account to keep liabilities separate.

If you’re ready to start building your business resume through practical spending, apply for a business net 30 account today. This simple move sets the stage for a more professional and financially independent future for your LLC.

The CEO Creative Framework: A Step-by-Step Path to Corporate Credibility

Building corporate credibility requires more than just one-off purchases. It demands a repeatable system that lenders can verify. The CEO Creative Membership streamlines this process by providing a consistent reporting environment. This structure helps remove the guesswork and administrative friction. When you’re explaining the value of tradelines to a business partner, having a concrete roadmap makes the process feel professional rather than experimental. It shows that you have a plan to move from basic vendor accounts to high-level corporate financing.

The 5-Step Credit Building Checklist

- Apply: Set up your Net 30 account using your EIN. Ensure your business details match your Secretary of State filings exactly to avoid reporting errors.

- Order: Purchase essential business items. Focus on things you already use, such as stationery, branded mugs, or team apparel.

- Pay: Clear the invoice before the 30-day mark. Paying early is better. It demonstrates superior cash flow management to the bureaus.

- Track: Monitor your report on platforms like FairFigure or Creditsafe. Seeing the data hit your file validates your strategy and keeps your partner engaged.

- Repeat: Maintain consistent monthly activity. This “seasons” the account and shows long-term reliability to future lenders.

Scaling Beyond Tier 1

Eventually, this path leads to corporate credit cards that don’t require a personal guarantee. This fully decouples your personal life from business liabilities, which is the ultimate win for any partnership. It also provides the financial flexibility to invest in high-end operations, such as booking a luxury chauffeur service dubai for your next board meeting or executive retreat.

What Happens Next

Once you activate your membership and place your first order, the reporting cycle begins. Here is what you can expect in the coming weeks:

- Account Activation: Your business information is verified to ensure it’s ready for accurate bureau reporting.

- First Reporting Cycle: Your initial activity is batched and sent to Equifax Business, Creditsafe, and FairFigure, typically within 30 to 60 days.

- Profile Maturation: As you repeat the cycle, your credit depth increases. This makes your LLC more attractive to traditional banking institutions.

Building an independent credit profile is a marathon, not a sprint. By following this structured framework, you protect your personal assets and create a valuable financial asset for the company. This strategic move ensures your partnership is built on a foundation of professional reliability and long-term financial strength. For B2C founders who want to complement their financial strategy with expert leadership guidance, check out Founder Freedom to learn from experienced CEOs.

Securing Your Company’s Financial Independence

Building a business credit profile is the most effective way to decouple your personal liabilities from your professional growth. By focusing on practical spending for branding and office essentials, you transform routine costs into a strategic resume for future lenders. You’ve learned how consistent reporting to Equifax Business, Creditsafe, and FairFigure creates the visibility needed to scale into higher credit tiers. Now that you’ve mastered explaining the value of tradelines to a business partner, it’s time to take the final step toward corporate credibility.

The CEO Creative provides a streamlined path for new LLCs and startups to build history without a personal guarantee. Our accounts offer instant approval and reporting to the major business bureaus, ensuring your on-time payments are always working for you. Don’t let a thin credit file limit your company’s potential. Apply for a CEO Creative Business Net 30 Account Today and start building the independent financial foundation your business deserves. Your future self and your business partner will thank you for making this strategic move today.

Frequently Asked Questions

Do I need a personal guarantee (PG) for a Net 30 account?

No, you don’t need a personal guarantee for many Tier 1 vendor accounts. Providers like The CEO Creative allow you to apply using only your EIN, which protects your personal credit score from being affected by business debt. This is a vital point when explaining the value of tradelines to a business partner because it limits individual liability while the company grows. It ensures that your personal assets remain safe even if the business faces challenges.

How long does it take for a tradeline to show up on my business credit report?

Reporting typically takes between 30 and 60 days to appear on your business credit file. Vendors usually batch their data and send it to bureaus once a month, so the exact timing depends on when your purchase was made relative to that cycle. If you make a purchase today, it might not show up until the next reporting window is completed. Consistency is vital so that your report shows steady activity every month.

Does paying early help my business credit score?

Paying early is one of the most effective ways to boost your business credit score. Many commercial scoring models reward companies that clear their invoices before the actual due date. For instance, a Dun & Bradstreet Paydex score of 80 indicates on-time payments, but reaching a score of 90 or 100 requires paying early. This behavior demonstrates excellent cash flow management and lower risk to any future lenders or suppliers.

Which credit bureaus does The CEO Creative report to?

The CEO Creative reports your payment data to Equifax Business, Creditsafe, and FairFigure. These bureaus are critical indicators for small business lending and vendor credit decisions in 2026. By reporting to these specific entities, your payment history becomes visible to a wide range of financial institutions. This visibility is essential for moving your business toward higher credit tiers and securing much better terms for future financing needs.

Can I build business credit with a brand new LLC?

Yes, you can start building business credit the same day you receive your EIN from the IRS. New LLCs often have “thin files,” which means they have no established history at all. Opening Tier 1 vendor accounts is the standard first step to establish a professional reputation. This is a powerful argument when explaining the value of tradelines to a business partner who may think the company is too young to qualify for credit.

What is the difference between a business tradeline and a personal tradeline?

A business tradeline is linked to your company’s EIN, while a personal tradeline is linked to your Social Security Number. Business accounts generally don’t appear on your personal credit report, so they don’t impact your personal debt-to-income ratio. This separation is the primary goal of corporate credit building. It ensures the business stands as its own legal and financial entity, protecting your personal borrowing power for things like home loans.

How many tradelines do I need to get a high-limit business loan?

Most lenders look for at least 3 to 5 seasoned tradelines before considering a business for high-limit financing or corporate cards. These accounts should show at least six to twelve months of consistent, on-time payment history. Building a “deep” file with multiple reporting vendors proves you can handle different types of credit. This foundation is necessary to qualify for Tier 2 and Tier 3 credit without personal guarantees.

What happens if I miss a payment on a Net 30 account?

Missing a payment will likely result in a negative report to the business credit bureaus. Late payments can significantly lower your business credit score and may stay on your report for several years. This makes it much harder to secure future credit or favorable terms from other suppliers. Always communicate with your vendor if you anticipate a delay to protect your company’s reputation and maintain the trust of your business partner.