Your EIN is more than just a tax ID; it’s a strategic financial tool that can function like a secondary bank account. You might be wondering how to buy what your business needs now without draining your bank account immediately. Understanding how vendor credit improves business cash flow is the key to turning everyday operational costs into a growth engine. It’s frustrating to watch your capital vanish the moment you buy office supplies or inventory, especially when traditional banks are tightening their lending requirements. With SBA loan minimum scores rising to 165 in 2026, finding alternative ways to keep your cash liquid is no longer optional; it’s a necessity for survival.

We know you want to keep your cash in the bank longer to handle inconsistent revenue cycles. This article will show you exactly how to leverage Net 30 vendor accounts, like those offered by The CEO Creative, to bridge those gaps while building a strong credit profile that doesn’t rely on your personal assets. We’ll walk through the mechanics of reporting tradelines, the steps to establish a profile from scratch, and how to use your “billing float” to scale your business sustainably.

Key Takeaways

- Master the concept of the “billing float” to keep your working capital in the bank for an extra 30 days while you fulfill orders.

- Learn exactly how vendor credit improves business cash flow by bridging the gap between operational expenses and incoming revenue.

- Understand how reporting vendor tradelines to bureaus like Equifax and Creditsafe builds a robust business credit profile without personal risk.

- Discover the strategic 5-step checklist to apply for Net 30 accounts and scale your credit limits through consistent, professional purchasing.

- Identify common pitfalls, such as inconsistent business information or overextending credit, to ensure your business remains fundable and credible.

What is Vendor Credit and the Cash Flow Gap?

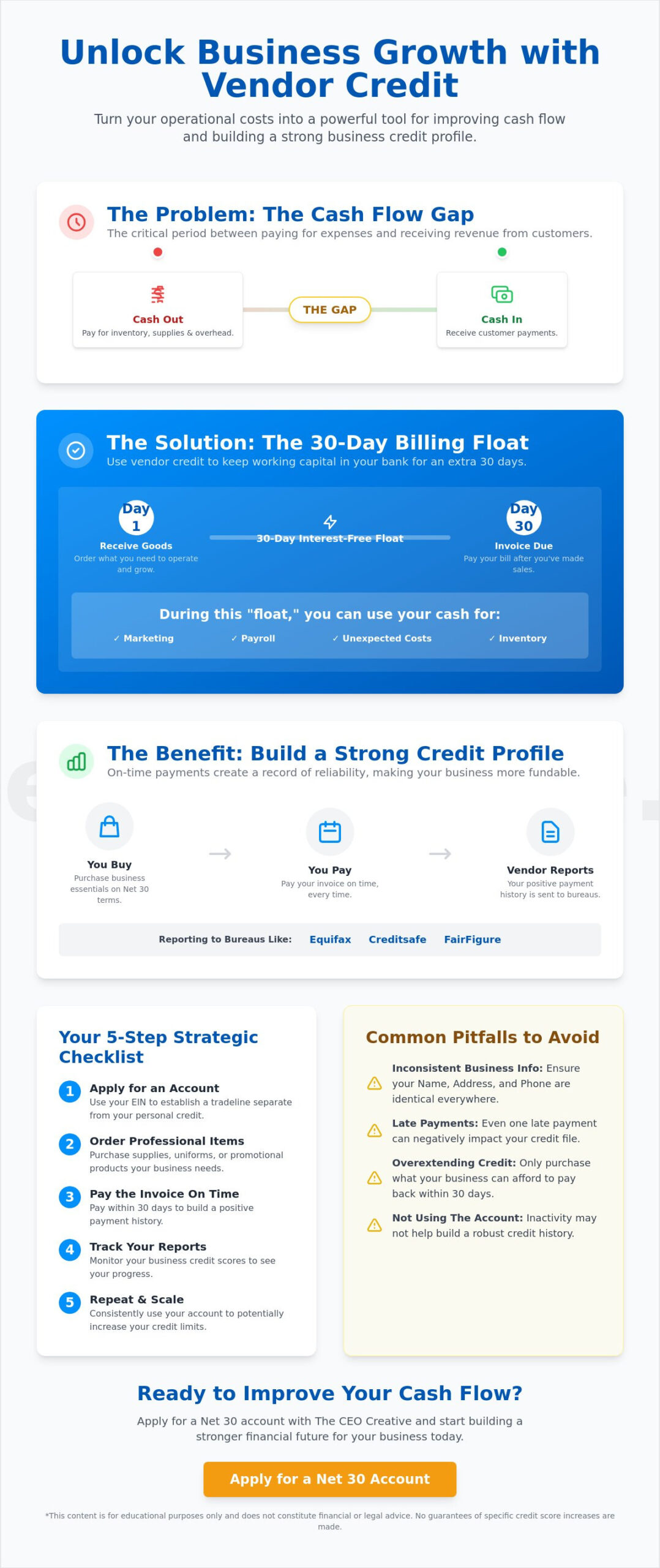

For many entrepreneurs, the biggest hurdle to growth isn’t a lack of customers; it’s a lack of liquid capital. What is Vendor Credit? Simply put, it’s a short-term financing arrangement where a supplier allows you to purchase goods or services upfront and pay the invoice at a later date. This delay in payment is a strategic advantage that addresses the “Cash Flow Gap.” This gap represents the stressful period between paying for your overhead, inventory, or marketing and actually receiving revenue from your customers.

The “Cash Flow Gap” is especially dangerous for new businesses that haven’t established a deep cash reserve. If you’re an ecommerce brand, you might pay for inventory today but not see a profit for weeks. Vendor credit bridges this gap by allowing you to sell the product or use the supplies before you’ve even paid the supplier, while using an omni-channel payment processor like Strictly ensures you capture those sales efficiently. This is exactly how vendor credit improves business cash flow for growing firms. It turns your accounts payable into a flexible tool for expansion.

To better understand this concept, watch this helpful video:

Most new LLCs and startups find Net 30 terms to be the most accessible entry point into business financing. Unlike traditional bank loans that require years of tax returns, Net 30 accounts are often approved based on your business credentials. This allows you to keep cash in your operational account for other emergencies while still acquiring the essentials your business needs to function.

Trust Note: This content is for educational purposes and does not constitute financial or legal advice. We make no guarantees regarding specific credit score increases.

Defining the Net 30 Vendor Account

A Net 30 account means you have 30 days from the invoice date to pay the balance in full. These are known as “vendor tradelines” and they differ significantly from traditional bank loans. While a bank loan involves interest rates and strict repayment schedules, vendor credit is typically interest-free if paid on time. By using your Employer Identification Number (EIN), you can establish these accounts as a separate entity from your personal finances. This is a critical step in protecting your personal assets from business risks while building a professional credit profile.

The Hook and Promise of Vendor Credit

Securing a $1,000 credit limit can happen quickly when you apply for a business net 30 account. This creates a strategic shift in your financial management from a “pay-as-you-go” model to a “grow-as-you-go” strategy. When you work with reporting vendors, your payment history is shared with bureaus like Equifax, Creditsafe, and FairFigure. This creates a permanent record of your reliability, making it easier to access larger loans and higher credit limits as your business matures.

The Mechanics of Net 30: Leveraging the Billing Float

The “Billing Float” is the engine behind your operational flexibility. It refers to the interest-free window between the moment you receive your goods and the moment the invoice is due. By utilizing this 30-day buffer, you keep your working capital accessible for other critical needs. This is a fundamental strategy for building business credit while maintaining a healthy bank balance. Understanding how vendor credit improves business cash flow allows you to treat your accounts payable like a revolving credit line that you control.

Reinvesting that floated cash into immediate revenue-generating activities is how startups scale. Instead of your money sitting in a vendor’s pocket, it stays in yours. This is a primary example of how vendor credit improves business cash flow during the lean months of a new venture. This strategy also provides a psychological benefit. It reduces the “cash-out anxiety” many founders feel when they see their balance drop. While the full 30 days are yours to use, occasionally paying by day 10 or 15 can strengthen your relationship with suppliers, often leading to higher credit limits and better terms in the future.

Just as you manage the psychological stress of business growth, maintaining your physical health is essential; specialized resources like Upper Cervical Care can help you find expert chiropractic support to keep you performing at your peak.

Calculating Your Cash Flow Benefit

Consider a scenario where you purchase $500 in custom apparel to fulfill a specific client contract. If you pay upfront, that $500 is gone before you even start the work. With a Net 30 account, you order the items today and deliver the finished product to your client in 20 days. If your client pays you upon delivery, you have the cash in hand to pay the vendor by day 30. You successfully completed a project without using a single dollar of your own reserves. This simple timing shift eliminates the need for expensive, high-interest bridge loans or credit card debt.

Strategic Inventory and Supply Management

Effective management means never letting your operations stall due to a lack of supplies. You can use vendor credit for recurring essentials like office supplies or branded merchandise. This is particularly useful when preparing for trade shows or marketing events. You can stock up on promotional items weeks in advance without depleting your payroll funds. By adjusting your order timing relative to your invoice due dates, you can navigate seasonal fluctuations with ease. If you’re ready to start managing your capital more effectively, consider opening a business net 30 account to secure your first reporting tradeline.

Strategic Credit Building: Tradelines and Bureau Reporting

A vendor tradeline is essentially a credit reference. It’s the documented history of your transactions with a supplier, which is then reported to commercial credit agencies. For businesses that have no history, these entries are vital. They prove that your LLC can handle debt and honor its agreements. Consistent reporting directly influences your credit scores, including the Paydex score, which operates on a scale from 1 to 100. Understanding how vendor credit improves business cash flow is the first step, but ensuring those payments are reported is what builds long-term fundability.

Success starts with business info consistency. Your business name, address, and phone number must be exactly the same on every account. If you use “Street” on one and “St.” on another, the bureaus might fail to link the data to your file. This attention to detail ensures you capture every bit of benefit from how vendor credit improves business cash flow. It turns routine spending into a strategic asset for your company’s future.

The Reporting Ecosystem: Beyond Equifax

In 2026, a “thick” credit file requires more than just one or two entries. While Equifax is a major player, visibility on Creditsafe is equally important for modern brands. Creditsafe provides global visibility, which is a major advantage if you ever seek international partnerships. FairFigure has also emerged as a key platform for monitoring and building business credit. When your payments are reported to multiple bureaus, you build a more resilient profile. This multi-layered reporting schedule creates the transparency lenders need to offer you better terms and higher limits.

Building Credibility with Tradelines

You don’t have to wait for large inventory orders to start this process. Essential services like logo design and brand development can function as reporting tradelines. This allows you to invest in your company’s visual identity while simultaneously strengthening your EIN-based credit. This is the first step in moving from Tier 1 vendors to Tier 2 opportunities, such as fuel cards or specialized retail accounts. Businesses that remain “unrated” often face higher barriers, including larger security deposits for leases and increased insurance premiums. By establishing these tradelines now, you position your brand as a reliable executive entity rather than a risky startup.

Implementation Guide: Maximizing Vendor Credit Safely

Implementation is where your financial strategy meets reality. Disciplined management is the only way to ensure you see how vendor credit improves business cash flow without creating unnecessary risks. You should treat your vendor accounts with the same level of seriousness as a high-stakes bank loan. Reliability is the primary currency of the business credit world; building it requires a repeatable system. Small, consistent purchases are far more effective for your score than one-off large orders. A pattern of five smaller orders over five months tells a much better story to bureaus than one massive order followed by months of inactivity.

Consistency proves you have recurring operational needs and the ongoing ability to meet your obligations. To get started, follow the 5-step vendor credit checklist: Apply, Order, Pay, Track, and Repeat. This cycle creates the “thick” credit file mentioned earlier. If you are ready to take the first step, you can apply for a business Net 30 account today to establish your foundation.

Your Step-by-Step Action Plan

- Step 1: Apply for a business Net 30 account using your EIN. Ensure your business name and address match your Secretary of State filings exactly.

- Step 2: Place an order for essential business items like custom apparel or office stationery. Keep the initial order manageable to ensure you can pay it back comfortably.

- Step 3: Pay the invoice in full before the 30-day deadline. Aim for day 20 or 25 to account for any processing delays.

Common Pitfalls to Avoid

Even small errors can stall your progress. Avoid these common mistakes to keep your credit building on track:

- Missing the payment deadline by even 24 hours. Late payments are the fastest way to damage a burgeoning credit score.

- Using a personal home address for applications when your business is registered at a commercial location or virtual office.

- Failing to track which specific bureaus each vendor reports to; don’t assume every vendor reports to all of them.

- Overextending your credit limit too quickly. Just because you have a $2,000 limit doesn’t mean you should use it all at once.

- Inconsistent business information. Using “The CEO Creative LLC” on one form and “CEO Creative” on another can fragment your credit file.

- Failing to monitor your reports. Check your Equifax or Creditsafe files regularly to ensure the vendor is reporting your payments accurately.

By following this structured approach, you ensure that how vendor credit improves business cash flow remains a benefit rather than a burden. Once you’ve mastered these first three steps, focus on tracking your reporting and repeating the process monthly to scale your limits.

The CEO Creative serves as a foundational partner for entrepreneurs who need to scale without exhausting their cash reserves. Unlike traditional retail, we provide a reporting Net 30 structure designed specifically for the needs of modern LLCs and startups. By using our services for your daily operational needs, you turn routine expenses into powerful financial assets. This is exactly how vendor credit improves business cash flow while simultaneously professionalizing your brand identity. Whether you need onboarding kits for new hires or branded apparel for your field team, every purchase contributes to a verifiable credit history.

The CEO Creative Membership offers more than just access to products; it provides a roadmap for growth. Members gain access to tools and tradelines that are often out of reach for new organizations. Instead of waiting months for a bank’s approval, you can begin building your EIN-based credit profile immediately. Routine expenses become assets. It’s a strategic shift that allows you to reinvest your liquid cash into marketing or product development while your credit profile matures in the background.

The CEO Creative Membership Advantage

New businesses often face high rejection rates from traditional institutions, especially with the 2026 SBA rule changes requiring higher credit scores. Our membership creates instant approval pathways, allowing you to secure Net 30 apparel and other essentials without a personal guarantee. We report your payment history to Equifax, Creditsafe, and FairFigure every month. This consistent visibility is the key to unlocking higher credit limits and better financing terms as your company matures. You get the items you need to run your business today while the bureaus record your reliability for tomorrow.

Recap and Strategic Move

You’ve now seen how vendor credit improves business cash flow by bridging the gap between your expenses and your revenue. By leveraging the 30-day billing float, you keep your capital liquid for emergencies or expansion efforts. The long-term vision is clear: use these Tier 1 vendor tradelines today to prove your reliability, so you can secure traditional bank loans tomorrow. Stay consistent with your reporting schedule and keep your business information accurate. Start small with items like customizable products or stationery, and pay your invoices early to maximize your score.

Frequently Asked Questions

Does The CEO Creative report to credit bureaus?

Yes, we report payment history to Equifax Business, Creditsafe, and FairFigure to help you build a robust business credit profile.

How long does it take for vendor credit to show on my report?

Most bureaus update their records every 30 to 60 days. Consistent monthly activity ensures your file stays current.

Do I need a personal guarantee for a Net 30 account?

No, our Net 30 accounts are established using your business EIN, allowing you to build credit without risking your personal assets.

What is the minimum order to trigger reporting?

We recommend consistent, manageable purchases of at least $100 to ensure there is meaningful data for the bureaus to record.

Does paying early help my business credit score?

Yes, paying early often results in a higher Paydex score, as it demonstrates exceptional financial responsibility to future lenders.

Can I get a Net 30 account as a new LLC?

Absolutely. Net 30 vendor accounts are the primary way new LLCs and startups establish credit when they have no prior history.

Is there a membership fee?

The CEO Creative offers a membership model that provides access to reporting tradelines and a wide range of business products and services.

Which bureaus are most important for my business?

Equifax and Creditsafe are critical for domestic and international visibility, while FairFigure provides modern monitoring tools for 2026.

Ready to professionalize your brand and build your business credit? Apply for The CEO Creative Membership today.

What happens next:

- Submit your application for a reporting Net 30 account using your EIN.

- Browse our catalog for essential office supplies or branding services.

- Pay your invoices on time to trigger reporting to major credit bureaus and build your profile.

Building a sustainable business requires both creative vision and structured financial systems. By utilizing vendor credit for items like Net 30 apparel and customizable products, you strengthen your company’s foundation. Stay focused on your reporting consistency to ensure long-term success.

Take Control of Your Financial Future Today

Mastering your cash flow is the difference between a struggling startup and a sustainable enterprise. You now understand how vendor credit improves business cash flow by providing a 30-day window to reinvest your working capital where it matters most. By leveraging the interest-free billing float and ensuring your payments are reported to Equifax, Creditsafe, and FairFigure, you’re building a foundation that makes your LLC truly fundable.

Don’t let a lack of credit history hold your brand back. You can access high-quality custom branding products and professional supplies while simultaneously growing your EIN-based credit profile. Most business memberships qualify for instant approval, making it easier than ever to start your journey. It’s time to stop worrying about bank rejection and start building. Apply for a CEO Creative Net 30 Account Today to secure your first tradeline and professionalize your operations. Your future growth depends on the strategic moves you make today.

Frequently Asked Questions

Do I need a personal guarantee for a Net 30 vendor account?

No, most Tier 1 Net 30 accounts do not require a personal guarantee. This is a primary benefit for business owners who want to separate their personal credit from their company’s liabilities. By using your EIN, you establish credit for the business entity itself. This structure protects your personal assets and allows the business to stand on its own financial feet.

How long does it take for vendor credit to show up on my business credit report?

You can expect your payment activity to appear on your business credit report within 30 to 60 days. Vendors typically report to bureaus on a monthly schedule; however, the time it takes for the bureau to process and display that data can vary. It’s important to maintain consistent activity over several months to ensure your file remains active and reflects a positive payment history.

Does paying a Net 30 invoice early help my credit score more?

Paying early is one of the most effective ways to boost your business credit score, specifically your Dun & Bradstreet Paydex score. While paying on time earns you a good score, paying 10 to 20 days before the due date can result in a perfect rating. This proactive approach demonstrates exceptional reliability; it shows future lenders that you manage your cash flow with precision.

What happens if I miss a payment on a Net 30 account?

Missing a payment can lead to late fees and negative reporting to business credit bureaus. Even a single late payment can significantly drop your business credit score and damage your reputation with suppliers. If you find yourself in a tight spot, contact the vendor immediately to discuss a payment plan. Maintaining open communication is better than allowing a delinquency to hit your permanent credit file.

Can I build business credit with vendor accounts if I have a new LLC?

Yes, vendor accounts are the most common starting point for new LLCs to establish a credit profile. Since many vendors offer Net 30 terms without requiring years in business, they act as the gateway to higher tier financing. This is exactly how vendor credit improves business cash flow for startups by allowing them to acquire supplies while building their first reporting tradelines.

Which credit bureaus does The CEO Creative report to?

The CEO Creative reports your payment history to Equifax Business, Creditsafe, and FairFigure. Reporting to multiple bureaus is essential for creating a “thick” credit file that different types of lenders can see. This broad visibility ensures that your positive payment behavior is recognized across the modern business credit landscape, making it easier to secure larger lines of credit later.

Is there a minimum purchase requirement to trigger credit reporting?

While reporting policies vary by vendor, we recommend a minimum purchase of $100 to ensure the data is meaningful for the bureaus. Very small purchases might not provide enough weight to significantly impact your score. Consistently ordering essential items like office supplies or custom apparel helps maintain a healthy reporting cycle and shows that your business has ongoing operational needs.

Can I use my EIN only to apply for vendor credit?

Yes, you can use your Employer Identification Number (EIN) to apply for many vendor credit accounts without providing a Social Security Number. This is a critical step in understanding how vendor credit improves business cash flow while keeping your personal finances separate. Using your EIN only ensures that the credit history belongs strictly to the business entity, which is vital for long-term corporate credit building.