Did you know that 93% of new businesses in early 2026 launched as sole proprietorships? Even though this is the most popular way to start, many owners still feel trapped by the fear of personal liability and the struggle to secure traditional bank loans. You might think that lacking a formal LLC means you’re stuck using your personal credit for every business expense. This is why learning how sole proprietors can build business credit is essential for protecting your personal assets and scaling your operations. We understand that you want a clear path to financial independence without the corporate jargon.

In this guide, you’ll learn the exact framework for establishing a robust business credit profile using Net 30 vendor accounts and strategic reporting. We’ll show you how to build an independent score with major bureaus like Equifax and Creditsafe using your EIN. We’ll also define how The CEO Creative serves as a reporting Net 30 vendor to help you secure tradelines. This article previews the step-by-step checklist you need to move from a zero credit file to a professional, credit-ready organization.

Key Takeaways

- Secure an Employer Identification Number (EIN) to separate your personal identity from your professional operations and ensure your data remains consistent across all credit bureaus.

- Utilize Net 30 vendor accounts to manage cash flow while establishing a track record of on-time payments that report to major business credit agencies.

- Follow a proven 5-step framework for how sole proprietors can build business credit by turning routine business expenses into strategic tradelines.

- Leverage a membership model to access instant approval for credit lines, allowing you to invest in high-quality branding materials without immediate out-of-pocket costs.

- Build independent business credit scores with bureaus like Equifax and Creditsafe to reduce your reliance on personal guarantees for future financing.

Understanding Net 30 and The CEO Creative’s Role in Your Growth

Trust Note: This content is for educational purposes only and is not financial or legal advice; no specific credit score increases are guaranteed. Discover how to transform your routine business spending into a powerful credit-building engine while learning how sole proprietors can build business credit using a proven 5-step framework. The CEO Creative is a reporting Net 30 vendor that helps businesses establish credit through essential branding and office supplies. By leveraging these accounts, you turn necessary operational costs into strategic financial assets.

A Net 30 account allows you to purchase goods today and pay the full invoice balance within 30 days. These accounts create vendor tradelines, which act as the foundation for Business credit reports. When you use payment reporting, your vendor sends your transaction history to major bureaus like Equifax, Creditsafe, and FairFigure. This process proves to future lenders that your business is reliable and capable of managing debt independently.

To better understand this concept, watch this helpful video:

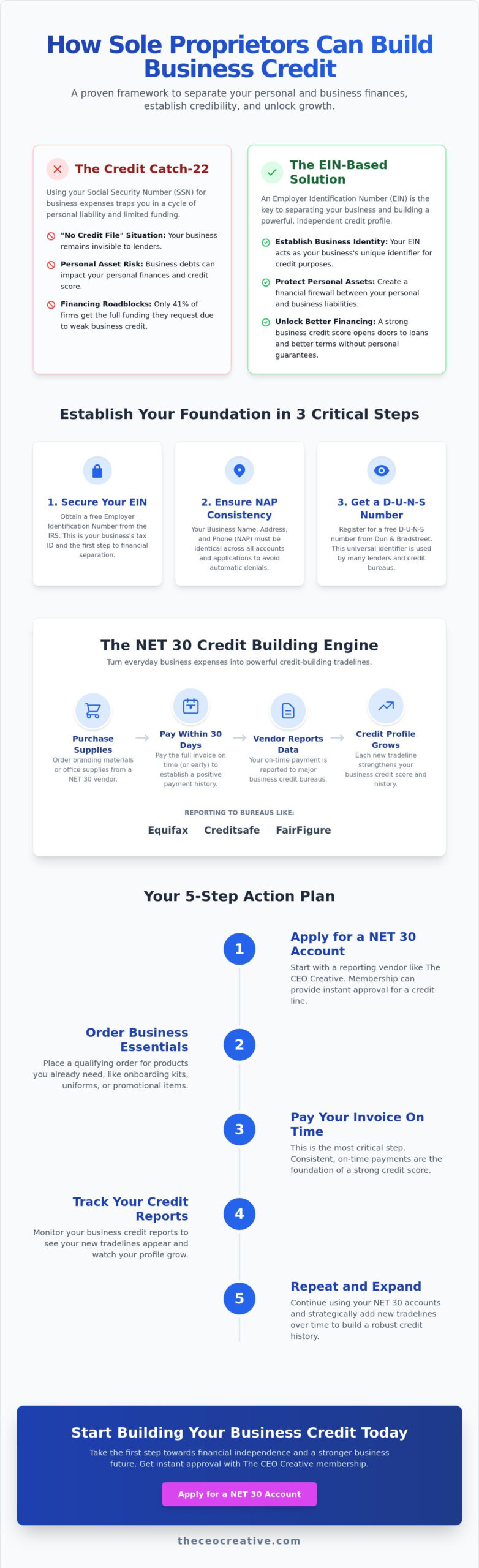

The Problem: The Credit Catch-22 for Sole Proprietors

Most solo owners fall into a common trap. They use their Social Security Number for every business expense. This creates a “no credit file” situation for the business itself. Without a history, you can’t get better terms or scale effectively. In 2024, only 41% of firms received the full amount of financing they requested. This limitation often stems from a lack of corporate credibility. Vendor tradelines bridge this gap. They provide a path to professional standing without requiring a high personal credit score or massive cash reserves.

The Solution: Separating Identity from the Start

The core of how sole proprietors can build business credit involves separating your personal identity from your business entity. You must move from an SSN-only mindset to an EIN-based credit profile. Securing The CEO Creative Membership is a strategic first step in this journey. It allows you to establish your first tradelines through purchases you already need for your brand. This guide provides a roadmap for your growth:

- Establishing Your Business Identity: The necessity of an EIN and data consistency.

- Mechanics of Tradelines: How reporting cycles work with major bureaus.

- The 5-Step Action Plan: A checklist to apply, order, and track your progress.

- Scaling Your Brand: Using membership to streamline your corporate credibility.

Establishing Your Business Identity as a Sole Proprietor

Setting a firm foundation is the most critical phase of your journey. You can’t build a house on sand; similarly, you can’t build professional credit on a personal Social Security Number alone. Understanding how sole proprietors can build business credit starts with obtaining an Employer Identification Number (EIN). While the IRS allows you to operate under your SSN, doing so keeps your business and personal finances permanently tangled. An EIN is free to obtain and acts as your business’s tax ID. It’s the first step to establish business credit because it allows you to apply for accounts without immediately alerting personal credit bureaus.

Consistency is your next priority. Lenders use automated systems to verify your data. If your business name is “John’s Consulting” on your bank account but “John Doe Consulting” on a credit application, you’ll face automatic denials. Ensure your name, address, and phone number (NAP) match exactly across all records. You also need a D-U-N-S Number from Dun & Bradstreet. This nine-digit identifier is free, and standard processing takes about 30 business days. Without it, you essentially don’t exist in the eyes of many commercial lenders. Finally, opening a dedicated business bank account is non-negotiable. It provides the clean financial data lenders require to verify your revenue and stability.

EIN vs. SSN: Which One Builds Your Future?

Using an EIN protects your personal credit score from the fluctuations of business spending. Lenders view EIN-only applications as a sign of a mature, organized business. When you rely solely on your SSN, you’re often required to provide a personal guarantee, making you personally liable for every cent of debt. By shifting to an EIN-based profile, you begin building a separate history that eventually allows for better terms and higher limits. This is a core strategy for anyone looking to build business credit without a loan. To start this process, you can apply for a business Net 30 account to generate your first reporting activity.

Setting Up a Professional Footprint

Credibility isn’t just about numbers; it’s about professional perception. Lenders and bureaus verify your business through public records and digital footprints. A generic Gmail address or a missing website can trigger red flags during the manual review process. You need a professional business email and a dedicated website to signal that you’re an established entity. A dedicated business phone line is also essential for bureau verification. You can streamline this process by investing in web packages that build your digital presence and your credit history at the same time. This professional footprint ensures that when bureaus look for your business, they find a consistent, reliable brand.

The Mechanics of Vendor Tradelines and Bureau Reporting

A vendor tradeline is more than just a payment arrangement. It’s a formal credit account between your business and a supplier that allows you to buy essential items today and pay the balance in full within a 30-day window. This short-term credit is the most effective way to build business credit without taking on high-interest debt. When you use a Net 30 account, you aren’t just buying office supplies or branding materials. You’re generating data. This data travels from the vendor to business credit bureaus, creating a history of financial responsibility that other lenders can verify.

Understanding the reporting cycle is vital for your strategy. Vendors typically batch their data and report it once a month. If you make a purchase on the 5th but the vendor reports on the 30th, your activity won’t show up until the following month’s update. This is why knowing how sole proprietors can build business credit involves patience and consistent activity across multiple reporting cycles. By maintaining active accounts, you ensure a steady stream of positive data points flows to your profile.

Why Net 30 Accounts Are Tier 1 Credit Builders

Tier 1 vendors are often the first to approve new businesses because they don’t always require a long track record or a high personal credit score. For a sole proprietor, this is a massive advantage. These accounts offer a low barrier to entry, allowing you to establish a footprint with just an EIN. As you maintain a history of on-time payments, many vendors will increase your internal credit limits. You can find a curated list of these opportunities in The Ultimate Guide to Net 30 Vendors.

What Reports and When? The Reporting Schedule

Data reporting isn’t just about paying on time. It’s about paying early. Business credit scores often rely on “Days Beyond Terms” (DBT). If you pay on day 20 of a 30-day term, you’re 10 days early. This results in a higher score than if you pay exactly on day 30. Your activity is reported to specific bureaus, including:

- Equifax Business: Tracks financial and trade data to assess risk.

- Creditsafe: Provides international and domestic credit ratings.

- FairFigure: Offers monitoring tools to track your progress in real-time.

This visibility allows you to track how sole proprietors can build business credit by watching your score rise as you diversify your tradelines and maintain clean reporting habits.

Your Step–by-Step Credit Building Checklist and Pitfalls

Success in building commercial credit requires a disciplined approach. You’ve already established your identity and learned the mechanics of reporting. Now, you need a repeatable system to generate positive data. This is how sole proprietors can build business credit effectively without getting overwhelmed by complex financial structures. By following a structured action plan, you’ll see how sole proprietors can build business credit while scaling their brand identity simultaneously.

- Apply: Secure instant approval for a Business Net 30 Account. Use the consistent business information you verified in previous steps to ensure a smooth verification process.

- Order: Select practical items that support your daily operations. Focus on essential Office Supplies or professional Custom Apparel for your team.

- Pay: Never wait until the due date. Pay your invoice 5 to 10 days early to maximize your score through positive Days Beyond Terms (DBT) reporting.

- Track: Monitor your reports with Equifax and Creditsafe. Verify that your tradelines appear correctly and reflect your early payment habits.

- Repeat: Consistency is the engine of credit growth. Make at least one purchase every month to keep your file active and current.

Common Mistakes to Avoid

Even small errors can stall your progress. Avoid these frequent pitfalls to keep your momentum:

- Using a personal email address like @gmail.com instead of a professional domain.

- Paying exactly on the 30th day, which lenders may view as a neutral rather than positive signal.

- Inconsistent business information across different vendor accounts, causing split files at the bureaus.

- Applying for Tier 2 or Tier 3 accounts before you have at least three solid Tier 1 tradelines.

- Neglecting to check your credit file for errors or missing tradelines that should’ve reported.

- Ordering items you don’t need; stick to onboarding kits or uniforms to keep spending professional.

The Importance of Consistency

A single purchase won’t build a sustainable score. Credit bureaus look for patterns of behavior over time. If you stop ordering, your file can become “thin” or inactive, causing your score to drop. Use branding products like Customizable Mugs and Apparel to keep your brand visible while maintaining your credit activity. Business Information Consistency is the alignment of name, address, and phone across all legal and financial documents. Maintaining this alignment is vital for ensuring your data reports correctly every time. Ready to start your first tradeline? Apply for a business Net 30 account today and begin your journey.

Scaling Your Brand and Credit with The CEO Creative Membership

The CEO Creative Membership acts as a foundational support system for your long-term success. It simplifies the logistical hurdles of management by bundling credit access with essential brand-building tools. Instead of managing multiple disjointed vendors, you have a single partner for your operational needs. This unified approach is a key part of how sole proprietors can build business credit while maintaining a high-level professional aesthetic. By treating basic essentials as strategic moves, you elevate your business from a solo venture into a credible corporate entity, much like how a specialized business like The Roast Haus Coffee Co. must establish its own professional identity to grow.

Turning Operational Costs into Assets

Buying items like office supplies and apparel through a Net 30 account is a strategic move for any growing brand. When you use a personal debit card, that money is gone instantly and leaves no footprint on your business credit reports. By using credit terms, you keep cash in your bank account to manage daily cash flow while building a history of reliability. High-quality branding increases your perceived creditworthiness to future lenders and partners. When a bank sees a consistent brand and a year of on-time tradeline reporting, they’re more likely to approve larger Tier 2 credit lines or traditional loans. You aren’t just spending money on routine items; you’re investing in your business’s future financial profile. This remains the most efficient framework for how sole proprietors can build business credit without relying on personal guarantees.

Final Summary and Next Steps

Building business credit as a sole proprietor starts with an EIN and a reporting vendor like The CEO Creative. By following the Apply-Order-Pay-Track-Repeat cycle, you can establish a professional identity that scales with your business. This framework ensures you’re no longer invisible to major bureaus and lenders. Sole proprietors can and should build credit to ensure long-term sustainability and financial independence.

Apply for your Net 30 account today and start building your brand and credit simultaneously.

What Happens Next:

- Your account is reviewed for instant approval based on your business information.

- You browse our extensive catalog for branding essentials and office supplies.

- Your on-time payments are reported to business credit bureaus to build your score.

Elevate Your Professional Credibility Today

Establishing a separate financial identity is the most strategic move a solo entrepreneur can make. You’ve learned how sole proprietors can build business credit by moving beyond an SSN and embracing an EIN-based profile. By integrating Net 30 vendor tradelines into your routine operations, you transform necessary spending into a powerful reporting engine. Consistency remains the key; paying your invoices early and maintaining monthly activity ensures your file stays active and attractive to future lenders.

The CEO Creative is ready to act as your foundational support system. Our membership accounts offer instant approval for new businesses and sole proprietors with no personal guarantee required. We ensure your positive payment history reaches the right eyes by reporting to Equifax Business, Creditsafe, and FairFigure. This visibility allows you to scale your brand while building the corporate credibility needed for long-term sustainability.

Stop relying on personal credit for business growth. Apply for a CEO Creative Net 30 Account today and take the first step toward a robust, independent business credit profile. Your journey from a solo venture to an established brand starts with one strategic purchase.

Frequently Asked Questions

Can I build business credit as a sole proprietor without an LLC?

Yes, you don’t need an LLC to establish a commercial credit profile. You can establish a separate credit profile by using an Employer Identification Number instead of your Social Security Number. This allows you to open vendor accounts that report to commercial bureaus. It’s a strategic move for solo entrepreneurs who want to protect their personal assets while growing their brand. Most major bureaus track sole proprietorships just as they do formal corporations.

Do Net 30 vendors require a personal guarantee for sole proprietors?

Not always, as many Tier 1 Net 30 vendors allow you to open accounts based solely on your business’s EIN. This means you aren’t personally liable for the debt, and the account doesn’t appear on your personal credit report. By using your EIN to apply, you build history for the business entity itself. This structure is ideal for startups and solo owners who want to establish credibility without risking their personal credit scores or assets.

How long does it take for The CEO Creative to report my payments to the bureaus?

Reporting typically occurs every 30 to 60 days. Once you pay your invoice in full, we batch your transaction data with other account holders and send it to the credit bureaus. The exact timing depends on the bureau’s processing schedule and the vendor’s reporting window. To ensure consistent reporting, make it a habit to order and pay early every single month. This creates a steady stream of positive data for your profile.

Does paying a Net 30 bill early help my business credit score more than paying on time?

Yes, paying early provides a significant advantage for your score. Business credit scoring models heavily weight how many days before the due date an invoice is settled. This is known as “Days Beyond Terms” or DBT. If you pay 10 days before the deadline, you signal to lenders that your cash flow is strong. This proactive habit often leads to faster score increases and higher credit limits than paying exactly on the due date.

What business credit bureaus does The CEO Creative report to?

We report your payment activity to Equifax Business, Creditsafe, and FairFigure. Reporting to multiple bureaus is important because different lenders use different data sources to evaluate your risk. By having your history visible on three major platforms, you ensure that your reliability is well-documented. This broad visibility makes it easier for your business to qualify for better terms and larger financing options as you scale your operations and brand identity.

Is an EIN required for a sole proprietor to build business credit?

An EIN is absolutely necessary for this process. It serves as the primary identifier for your business, similar to how a Social Security Number identifies you personally. Using an EIN is the most effective way to track how sole proprietors can build business credit independently. It allows bureaus to create a separate file for your professional activity. This separation is the first step toward building a business that stands on its own without personal liability.

What happens if I miss a payment on my Net 30 account?

Missing a payment will likely result in negative reporting to the bureaus. Just as on-time payments build your score, late payments will lower it. You may also face late fees or have your account terms revoked. If you anticipate a delay, contact your vendor immediately to discuss the situation. Maintaining a clean record is vital for your long-term credibility and your ability to secure Tier 2 or Tier 3 credit lines in the future.

Can I use my personal credit card to pay my Net 30 invoice?

You can use a personal card, but we recommend using a business bank account or business debit card. Keeping your finances separate makes tax season easier and provides a clean audit trail for lenders. You can learn more about EmLedger to see how professional accounting software streamlines this documentation for sole proprietors. When you apply for larger loans, banks will review your business bank statements to verify your revenue. Paying your Net 30 invoices from a business account proves that your company is a self-sustaining entity with its own cash flow.

How many tradelines do I need to see a business credit score?

You generally need at least three reporting tradelines to generate a business credit score. Having a single account isn’t enough for bureaus to assess your overall creditworthiness. Consistently adding new vendors is a core part of how sole proprietors can build business credit over time. Each new tradeline adds depth to your file. Aim to have five to ten active reporting accounts to demonstrate a high level of financial maturity to future lenders.

What is the difference between a vendor tradeline and a credit card?

A vendor tradeline is a direct line of credit from a supplier for specific goods, while a credit card is a revolving line from a bank. Vendor accounts usually have a fixed payment term, like Net 30, and are often easier for new businesses to secure. Credit cards offer more flexibility in where you can spend but often require a personal guarantee or a higher credit score. Both are useful tools for building a robust commercial credit profile.