Corporate credit has been a cornerstone of business operations for decades. Over the years, the way businesses manage their finances has gone through significant changes. Initially, companies relied heavily on Net 30 credit terms, a system where businesses were required to pay their invoices within 30 days. Though it worked well for a time, this method came with certain limitations. Businesses naturally started searching for something more flexible and accessible, leading to the development of revolving credit lines. Today, these lines provide businesses with a more dynamic way to handle their financial needs and empower them to grow at their own pace.

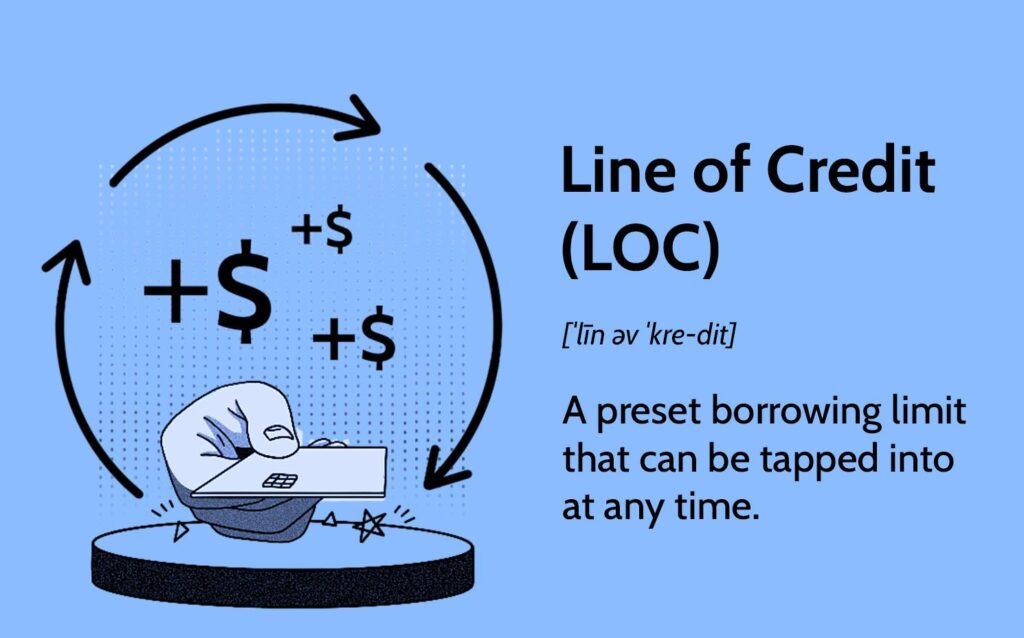

Transformation to Revolving Lines of Credit

Remember when business owners had to juggle stacks of invoices and payments on a strict 30-day schedule? Those Net 30 credit terms were once the bread and butter of many businesses. But as businesses evolved, so did their financial needs, leading to the emergence of revolving lines of credit. This transformation has been a game-changer in the world of corporate finance.

Key Features of Revolving Credit

Revolving credit is like having a financial safety net that you can dip into when needed, without the constraints of short-term repayment deadlines. Here are some of its standout features:

– Flexibility: Unlike fixed-term loans, revolving credit allows you to borrow, repay, and borrow again up to a certain limit without reapplying. This makes it incredibly adaptable to changing business needs.

– Variable Interest Rates: Many revolving credit lines come with interest rates that can fluctuate based on market conditions. This can be beneficial in a stable market but might require extra caution during volatile times.

– Credit Limit: Businesses are approved for a maximum borrowing limit, which they can utilize partially or fully. This limit is determined by the lender based on the business’s creditworthiness.

– No Fixed Payment Structure: Payments are usually based on the amount of credit used, which can make cash flow management more predictable for businesses that experience seasonal or unexpected fluxes in revenue.

Benefits for Modern Businesses

Revolving lines of credit offer a suite of benefits tailored for the dynamic needs of today’s enterprises:

– Enhanced Cash Flow Management: Businesses can maintain liquidity even during low revenue periods. This smooths out cash flow irregularities and helps manage daily operational costs more effectively.

– Quick Access to Funds: When a business deals with unexpected expenses or opportunities, having immediate access to funds can be invaluable.

– Simplified Financial Planning: By having an open line of credit, businesses can better plan their finances as they don’t have to worry about applying for a new loan each time they need capital.

– Capital for Growth: Whether it’s for expanding operations or taking advantage of a new business opportunity, revolving credit provides the financial muscle businesses need for growth without delay.

Challenges and Considerations

Despite its advantages, revolving credit comes with its own set of challenges. Here are some critical points business owners should consider:

– Variable Costs: With interest rates that can change, businesses might face increased costs if the rates rise suddenly.

– Risk of Overspending: Easy access to credit can sometimes lead businesses into a debt spiral if they don’t manage their spending responsibly.

– Stringent Qualification: Establishing a revolving line of credit might require a strong credit history and solid financial standing, which could be a hurdle for new businesses.

– Potential for High Fees: Some credit lines come with high annual fees or penalties for certain activities, such as withdrawing more than a stipulated amount.

Impact on Business Credit History

One of the critical aspects of transitioning from Net 30 terms to revolving lines of credit is the impact on a business’s credit history. The way businesses handle their revolving credit significantly influences their creditworthiness and financial strategies.

Building and Maintaining Creditworthiness

Revolving credit lines play a crucial role in building and maintaining a strong business credit history. Here’s how:

– Positive Payment History: Regular and timely repayment of revolving credit can enhance a business’s credit score. This is crucial because lenders often view timely repayments as a sign of reliability.

– Utilization Rate: Keeping the credit utilization ratio—a measure of how much is borrowed versus the credit limit—low can positively impact the business’s credit score. Businesses that manage this aspect well are often seen as financially disciplined.

– Diverse Credit Portfolio: Having a mix of credit types, including revolving credit, can strengthen a business’s credit profile. This diversity shows potential lenders that the business can manage different kinds of credit.

Influence on Financial Strategies

The switch to revolving lines of credit from traditional Net 30 terms has also transformed how businesses plan financially. Here’s how:

– Strategic Flexibility: Businesses can make strategic investments without needing to wait for long approval processes, enabling them to capitalize swiftly on market opportunities.

– Leverage for Negotiations: Strong credit history due to effective use of revolving credit can position businesses better when negotiating with suppliers or potential investors.

– Risk Management: Revolving credit provides a buffer against economic downturns, helping businesses sustain operations and workforce even in trying periods.

Changes in Business Credit Scoring

The evolution of corporate credit has brought about significant changes in how business credit scoring is approached:

– Comprehensive Assessment: Credit scoring now takes a more comprehensive view, considering not just payment history but also credit utilization, debt levels, and credit diversity.

– Predictive Analytics: Advanced data analytics are used to predict credit behavior, providing a more accurate picture of a business’s financial health and risk profile.

– Focus on Real-Time Data: Credit reporting agencies are increasingly focusing on real-time data to provide up-to-date insights into a business’s credit performance, which can greatly affect scoring.

In conclusion, the transition from Net 30 terms to revolving lines of credit marks a significant shift in corporate finance. While it provides flexibility and numerous financial tools for growth and stability, it also requires businesses to be vigilant about managing credit responsibly to maintain their creditworthiness and financial health. By understanding and leveraging the nuances of revolving credit, businesses can navigate the modern financial landscape with greater confidence and agility.

Conclusion

As corporate credit continues to evolve, businesses stand at an exciting crossroads. Transitioning from net 30 credit terms to more flexible revolving credit lines offers companies the opportunity to manage their cash flow with greater ease and agility. This shift not only helps improve business credit history but also allows companies to seize new opportunities as they arise. Here are some key takeaways:

– Flexibility: Revolving credit lines offer more adaptable payment schedules.

– Growth: Easier access to funds means businesses can invest in growth sooner.

– Opportunities: Companies can capitalize on market opportunities without delay.

The evolution of corporate credit is a journey toward more dynamic financial solutions, paving the way for businesses to thrive in today’s fast-paced economy. As we embrace these changes, businesses are better equipped to navigate the financial landscape and achieve their goals.