![Business Financing Options [A Guide to Securing Capital]](https://theceocreative.com/wp-content/uploads/2025/01/Securing-Capital-A-Guide-to-Business-Financing-Options.jpg)

Starting or growing a business can be as exciting as a rollercoaster ride, but just like any ride, it needs a strong base. That’s where getting money comes in! Having enough funds is crucial to take advantage of growth chances or simply keep your business running.

Luckily, there are many ways to get financing. Whether you’re just starting out or have been in business for a while, knowing these options can help you turn your business ideas into reality. So, get ready as we dive into the world of business financing!

Understanding Your Business Financing Needs

Choosing the right way to get money for your business can feel like standing at a fork in the road, unsure which way to go. But don’t stress! By doing some research and gaining a clear idea of what you need, you can figure out the best business financing option.

Assessing Capital Requirements

Before you start looking for money, take a moment to think, “How much money do I really need?” Whether you’re just starting out or have been running a business for a while, knowing exactly how much money you need is very important. Begin by making a detailed plan for your budget. This plan should include:

– Startup Costs: These are one-time expenses like buying equipment, getting licenses, and your first batch of products.

– Operational Costs: These are regular expenses such as rent, electricity, and paying your employees.

– Emergency Funds: It’s always smart to have some extra money saved for unexpected problems.

Think about what you need right now and what you might need in the future. Having a clear idea of how much money you need will help you talk to people who might lend or invest in your business.

Evaluating Risk and Return

Every way to get money for your business has its own mix of risks and possible rewards. It’s important to think about these things carefully to make good decisions. Ask yourself:

– What could go wrong? Are you okay with making regular interest payments, or does the idea of giving up part of your business worry you more?

– What do you hope to gain? Think about how the money will help your business make more income.

By balancing the risks and rewards, you can choose a way to get money that works well and helps your business grow in a healthy way.

Aligning Financing with Business Goals

Lastly, make sure your funding decisions match your long-term business plans. Are you aiming for quick growth, or do you prefer slow and steady progress? Different types of funding are suited for different needs. For example, a short-term loan can help with seasonal costs, while selling shares in your business might be necessary for expanding your operations.

By matching your funding approach to your business goals, you can grow not just quickly, but wisely too!

Traditional Funding Methods

Once you know how much money you need, it’s time to explore the usual ways to get funding and learn how to build business credit. These methods are well-known, reliable, and have helped many businesses get the financial support they need.

Bank Loans: Pros, Cons, and Qualifications

Bank loans are a common and dependable way to finance a business—they’re like the basic, go-to option for many. Here’s a simple breakdown:

Advantages:

– Steady and clear: Fixed interest rates and set repayment schedules mean you know exactly what to expect from the beginning.

– Keep full control: Unlike selling shares, you don’t have to give up any ownership of your business.

Disadvantages:

– Strict credit checks: Banks usually require a good credit score, which can be hard for new businesses to achieve.

– Need for collateral: Most loans require you to offer assets (like property or equipment) as security, which adds some risk.

What you need to get a bank loan:

To get a loan from a bank, you usually need:

– A clear and strong business plan

– A good credit history for both you and your business

– Clear and detailed financial records and future money plans

Knowing these things will help you decide if a bank loan is the best choice for your business.

SBA Loans: Government-Backed Support for Small Businesses

Sometimes, you need a bit of support from the government. That’s where SBA loans can help. These loans are supported by the Small Business Administration and are a great option for small businesses that want to expand.

Advantages:

– Lower interest rates and longer repayment periods: Because the government backs these loans, they often have better terms.

– Versatility: You can use them for different purposes, like covering daily expenses or buying property.

Disadvantages:

– Long application process: Be ready to fill out a lot of forms and wait a while for approval.

– Personal guarantee: Most SBA loans need you to promise to pay back the loan personally, which means your own belongings could be at risk if the business doesn’t succeed.

Requirements:

To get an SBA loan:

– Your business must be small (usually fewer than 500 employees).

– You need good personal and business credit.

– Your business must be legal and make a profit.

When deciding, think about what your business needs and how an SBA loan can help meet those needs.

Once you know your financing needs and have looked at traditional funding options, you’re closer to getting the money your business needs to grow. Next, we’ll talk about newer ways to get funding. Keep reading!

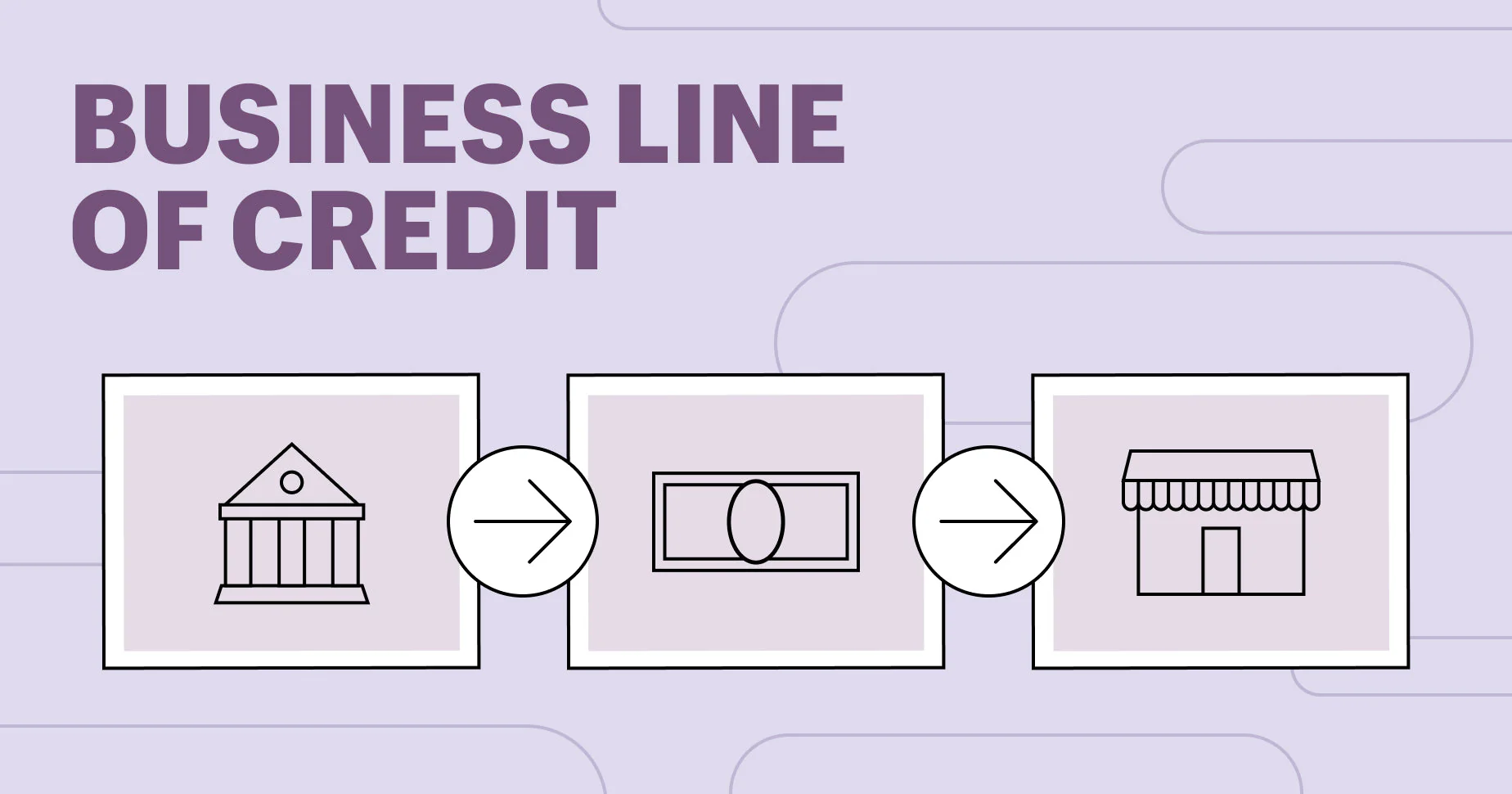

Lines of Credit: Flexibility for Business Needs

In the world of business funding, lines of credit are a flexible and adaptable choice. Unlike loans, which give you a large amount of money all at once, lines of credit work more like a financial backup plan. They let businesses take out money when they need it. This can be especially helpful for businesses that have ups and downs in their cash flow or those that run into surprise costs. But how do these lines of credit actually work, and are they a good fit for your business? Let’s take a closer look.

How Business Lines of Credit Work

A business line of credit works a lot like a credit card. You get approved for a certain amount of money, but you don’t have to use it all at once. You can take out money whenever you need it, up to your approved limit, and you only pay interest on the amount you actually use. This makes lines of credit a great option for businesses that need extra cash for everyday needs, like paying employees during slow times or buying inventory.

Here’s how you can use a line of credit:

– Handle Cash Flow: Use the money to cover expenses when your cash is running low.

– Grab Opportunities: Quickly get funds to take advantage of new business opportunities.

– Seasonal Support: Use it to keep your business running smoothly during slower seasons.

The best part is that once you pay back what you borrowed, the credit becomes available again, and you can use it up to your limit whenever you need it. This makes it a flexible and reusable source of money.

Secured vs. Unsecured: Understanding the Difference

When looking into a line of credit, you’ll come across two main types: “secured” and “unsecured.” Here’s what they mean:

– Secured Line of Credit: This type of credit is tied to an asset you own, like property or inventory. By offering something as collateral, it’s usually easier to get a larger credit limit with lower interest rates. However, if you can’t make payments, you risk losing the asset you used as collateral.

– Unsecured Line of Credit: This type doesn’t require any collateral. Instead, it’s based on how trustworthy your business is financially. Because there’s no asset backing it, interest rates are often higher, as lenders take on more risk.

Deciding between a secured and unsecured line of credit depends on your business needs. If you have valuable assets and want lower interest rates, a secured line could be the better option. But if you prefer less paperwork and can handle higher interest rates, an unsecured line might work better for you.

Alternative Business Financing Solutions

Not every business fits the usual way of getting money, and that’s totally fine! There are many other ways to get funding that can work for your specific business needs. Whether you’re just starting out or already running a business and need money fast, here are some options to think about:

Invoice Financing: Unlocking Cash Flow from Invoices

Invoice financing is a way for businesses to get money by using unpaid invoices as a guarantee. This can be very helpful for companies that have trouble with cash flow because their customers take a long time to pay. Instead of waiting 30, 60, or even 90 days for payment, businesses can get most of the money from the invoice right away through invoice financing.

Main advantages include:

– Better Cash Flow: Quickly access money to pay workers, buy supplies, or grow the business.

– Fast Approval: The financing decision often depends on your customer’s credit, not yours.

– Flexibility: You usually don’t have to finance all your invoices, so you can pick which ones to use.

This financing option can be a big help for businesses that have to wait a long time to get paid, allowing them to keep running smoothly without needing to take on regular loans.

Merchant Cash Advances: Fast Funding, Higher Costs

Need money quickly? A Merchant Cash Advance (MCA) could be an option for you. With an MCA, you get a lump sum of cash upfront, and in return, you agree to give a portion of your future credit card sales. This option is often easier to get than a regular loan, which makes it appealing for businesses that need fast cash.

But be careful:

– Higher Costs: MCAs usually have much higher fees compared to traditional loans.

– Frequent Payments: Payments are often taken daily or weekly from your credit card sales, which can put pressure on your cash flow.

– Risky Dependence: Since repayments depend on future sales, you’ll need steady credit card transactions to keep up with payments.

While MCAs are tempting because they’re quick and easy to get, they’re best used as a short-term fix. The high costs and frequent payments can create problems for your business if you’re not careful.

Crowdfunding: Harnessing the Power of the Crowd

In today’s internet era, raising money has become more collaborative than ever. Crowdfunding websites like Kickstarter and Indiegogo let businesses share their ideas with the public. In return, supporters often get early access to products, special rewards, or even a small share in the company.

Why think about crowdfunding?

– Connect with People: Talk directly to potential customers and get them excited about your product or service.

– Test Your Idea: See if people are interested before fully launching and get helpful feedback from supporters.

– No Loans Needed: Money raised through rewards-based crowdfunding doesn’t have to be paid back.

But running a successful crowdfunding campaign takes effort. You need a good marketing plan and to stay in touch with your backers. It’s not just about asking for money; it’s about sharing a great story and creating a group of people who believe in your brand.

Looking into different ways to get funding can help businesses that need more support than what regular banks can give. Whether you’re getting money from unpaid invoices or gathering funds from a group of people through crowdfunding, each choice has its own benefits and difficulties. The important thing is to pick the right funding option that fits your business goals and abilities, so you can get the money you need in a smart and lasting way.

Choosing the Right Financing for Your Business

Choosing the right way to fund your business is like finding the perfect pair of shoes — it needs to feel right and match the situation. Every business is different, so there’s no single solution that works for everyone when it comes to financing. Let’s go over some key points to help you figure out what’s best for you.

Aligning Financing with Business Goals and Needs

First, think about where you want your business to go. Do you want to grow, create a new product, or make your operations better? Knowing your business goals will help you choose the right way to get money. For example:

– Growth or Expansion: If you want to grow, you might look into a business loan or venture capital. These can give you a lot of money for big projects.

– Creating a New Product: If you need money over time for research or slowly developing a product, a line of credit could work well.

– Improving Operations: If you want to buy new technology or machines, equipment financing might be the best option.

By matching the way you get money with your goals, you can make sure the funds you get help you reach the targets you’ve set.

Comparing Interest Rates, Terms, and Fees

Once you’ve figured out your goals, it’s time to focus on the financial details. A low-interest rate might not always be the best option if other conditions aren’t good. Here’s what to pay attention to:

– Interest Rates: Compare different lenders to get the best rate for your business. A lower rate can save you a lot of money over time.

– Loan Length: Think about how long you’ll have to repay the loan and if it matches your cash flow plans. Short-term loans might mean higher monthly payments, but you’ll pay less interest in total.

– Fees: Be careful of hidden costs like setup fees, penalties for paying early, and other charges. Make sure you understand all the costs before choosing a loan.

Making smart choices in these areas can help you avoid money problems later and make sure the loan is the right fit for your business.

Factors to Consider When Choosing a Business Financing Option

Just like you carefully think about all the details before making a big choice, such as buying a house or a car, it’s important to look at all the important factors when getting money for your business. Let’s go over what you should think about.

Your Business’s Financial Situation and Creditworthiness

Your financial situation and credit history are like a report card for your business — lenders use these to decide if they can trust you to repay a loan.

– Business Finances: Make sure your financial records are clear and organized. Lenders will usually check your cash flow, income, and how much profit you’re making.

– Credit Score: A strong credit score can help you get better loan terms and lower interest rates. Check your credit report and fix any mistakes or issues.

– Debt-to-Income Ratio: Lenders like businesses that handle their debts well. A lower ratio shows that you can easily pay off your debts with the money you earn.

If your finances are clear and your credit is good, you’ll have a better chance of getting the funding you need.

The Amount of Funding Needed and Repayment Terms

The next step is figuring out how much money you actually need and making sure you can pay it back as part of your business plan.

– Assess Your Needs: Before asking for a loan, figure out exactly how much money your project or business needs, including any unexpected expenses that might come up.

– Plan for Repayment: Think about different ways you can pay back the loan. Can your business handle the payments even if sales slow down for a while? It’s important to be ambitious but also careful.

– Match Loan Terms to Your Needs: Make sure the time you have to repay the loan fits with what you’re using the money for. For example, use short-term loans for quick needs and long-term loans for bigger investments.

By knowing how much money you need and how you’ll pay it back, you can avoid borrowing too much or agreeing to payments you can’t afford.

The Type of Asset or Project Being Financed

Finally, take a close look at what the money will be used for. The type of asset or project you’re working on can greatly affect the kind of financing you should pick.

– Physical Items: Loans for things like equipment or property can help you buy these items, and the loan terms can match how long the item is expected to last.

– Non-Physical Projects: If you’re paying for something like a marketing plan or software creation, think about whether a line of credit or a term loan would work better.

– Risky Projects: For new businesses working on unique but untested ideas, venture capital or angel investors might be a good choice. They can offer not just money but also advice and guidance.

By figuring out exactly what you need the money for and choosing the right financing option, you can make sure the funds help you achieve your goals.

In short, picking the right way to fund your business can help it succeed. By matching your funding options with your business goals, knowing how it will affect your finances, and thinking about the kind of project you’re working on, you’ll be on track to get the money your business needs to grow.

Conclusion

Getting business financing might feel overwhelming, but understanding your choices and developing strong cash flow management strategies can make it easier. Whether you go for a regular business loan, try crowdfunding, or look for angel investors, each option has its own benefits. The important thing is to figure out what you need, do your homework, and pick the option that fits your business goals best. With the right funding and smart cash flow management, your business can grow and reach its full potential. Don’t hesitate to take that next step!